PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072582

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072582

Manufacturing Operations Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

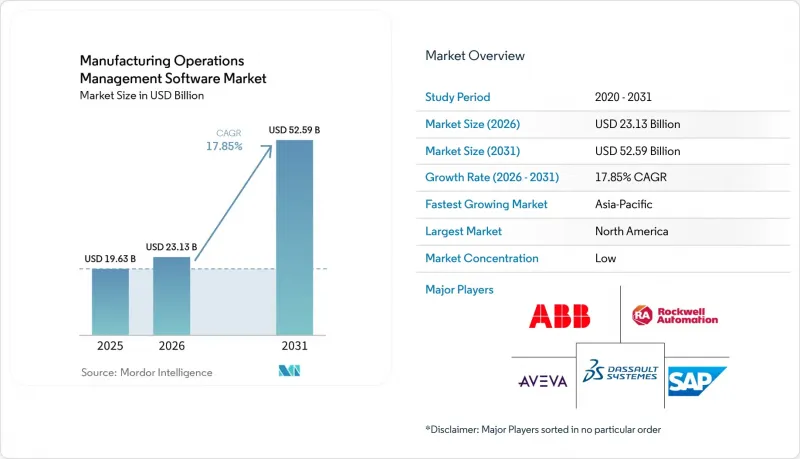

According to Mordor Intelligence, the manufacturing operations management software market size is projected to expand from USD 19.63 billion in 2025 and USD 23.13 billion in 2026 to USD 52.59 billion by 2031, registering a CAGR of 17.85% between 2026 and 2031.

This report is Segmented by Deployment Mode (On-Premises, Cloud, and Hybrid), Component (Software, and Services), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Function Type (Manufacturing Execution System, Planning and Scheduling, and More), End-User Industry (Aerospace, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Manufacturing Operations Management Software Market Trends and Insights

AI-Driven Real-Time Production Optimization Is Redefining Throughput Economics

AI has moved beyond maintenance alerts and is becoming a practical tool for real-time throughput control in the manufacturing operations management software market. Production scheduling systems are increasingly combining telemetry, demand changes, and machine-state data in near real time, enabling plants to resequence work faster than static dispatch logic can manage. Schneider Electric and Microsoft showed this direction at Hannover Messe 2026, where their industrial copilot reduced control configuration and documentation time by up to 50% in live demonstrations. Emerson pushed the same theme further with AspenTech AVA in May 2026, combining first-principles industrial models with large language models so operators can act on recommendations inside operational workflows. This matters because manufacturers that place AI inside the execution layer can reduce the time between deviation detection and corrective action, which compounds into stronger OEE performance over repeated production cycles.

Industry 4.0 And Smart Factory Expansion Drive Sustained Platform Investment

Industry 4.0 programs are now tied to plant roadmaps rather than isolated pilot projects, which is expanding the role of the manufacturing operations management software market across core production environments. Digital twins, connected equipment, and real-time analytics are being deployed as operating infrastructure, not optional experiments. India is becoming important in this shift because Rockwell Automation's 2026 findings showed that 97% of Indian manufacturers considered digital transformation essential, while high-spend respondents allocated materially more operating budget to industrial technology than their global peers. Large multi-site rollouts are also becoming more common, as shown by Siemens Energy's use of SAP Digital Manufacturing to standardize execution across more than 70 plants. This pattern supports a longer investment cycle because smart factory programs now depend on persistent platform layers that can connect execution, quality, and analytics across a full network of facilities.

Brownfield Integration And Data Model Complexity Remain The Primary Adoption Brake

Brownfield complexity remains the largest operating constraint on the manufacturing operations management software market because most installed industrial assets were not designed for modern bidirectional data exchange. Plants still run a mix of PLCs, SCADA systems, legacy fieldbuses, and proprietary machine protocols, which require staged connections before unified execution systems can function reliably. A 2026 paper in The International Journal of Advanced Manufacturing Technology showed that even when modern interfaces are missing, legacy integration can still be achieved through a multi-step architecture using Modbus TCP, MQTT middleware, buffering, and phased synchronization. That kind of sequence extends deployment timelines and increases the amount of edge normalization, data cleansing, and mapping required before the value is visible to the plant. It also explains why full-platform ROI can be delayed by 18 to 36 months in sites with extensive legacy, customized infrastructure.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native And Hybrid MOM Adoption Accelerates Across Enterprise Tiers

- Tighter Quality And Traceability Mandates Structurally Expand MOM Scope

- OT-IT Skills Shortage And Change Management Friction Slow Platform ROI

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployment accounted for 45.23% of the manufacturing operations management software market share in 2025, reflecting the weight of regulated sites that still prefer validated local control over remote application hosting. In pharmaceutical, aerospace, semiconductor, and other tightly controlled environments, core execution systems remained on site due to data sovereignty, cybersecurity policies, and validation routines, slowing migration. This installed base explains why the manufacturing operations management software market still carried substantial legacy infrastructure in 2025, even as new investment priorities changed. Siemens positioned Opcenter X as a cloud-native SaaS offering for smaller discrete manufacturers seeking a more modular, lower-friction path to digital execution.

Cloud deployment is forecast to grow at a 17.97% CAGR, making it the fastest-growing segment of the manufacturing operations management software market during 2026-2031. This shift is being supported by subscription economics, faster template rollout across sites, and easier benchmarking between plants using shared process models. Siemens Energy standardized processes across more than 70 plants using SAP Digital Manufacturing, underscoring why cloud delivery is attractive for manufacturers that need network-level visibility rather than plant-by-plant isolation. Hybrid deployment is also gaining ground because it balances deterministic shop-floor execution with the scale of reporting and analytics that cloud infrastructure can deliver.

Software accounted for 67.34% of the component mix in 2025, reflecting the scale of licensing and subscription revenue already established across installed manufacturing platforms. That share kept the manufacturing operations management software market centered on platform ownership and recurring application value rather than pure project revenue. Even so, services expanded faster because brownfield integration, data harmonization, user adoption, and site-by-site rollout all require hands-on support. Buhler's SAP Digital Manufacturing rollout at its Uzwil site showed how implementation services were the main unlock for later expansion across China, Germany, and the United Kingdom.

Services are forecast to grow at a 18.14% CAGR, making it one of the fastest-expanding segments of the manufacturing operations management software market during 2026-2031. Managed services are now extending the vendor relationship beyond go-live through connector monitoring, update administration, and uptime commitments in regulated environments. IGZ and United Manufacturing Hub demonstrated that combining SAP Digital Manufacturing with a data platform supporting more than 150 IT and OT protocols can materially reduce integration complexity and shorten machine onboarding timelines. This model, which combines a software supplier, an implementation partner, and a managed-service layer, is becoming the standard commercial structure for large enterprise rollouts.

Complete Report Scope:

- By Deployment Mode

- On-Premises

- Cloud

- Hybrid

- By Component

- Software

- Services

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Function Type

- Manufacturing Execution System (MES)

- Planning and Scheduling

- Quality Process Management

- Inventory Management

- Other Function Types (Labor Management, Analytics)

- By End-user Industry

- Aerospace

- Automotive

- Pharmaceuticals

- Medical Equipment

- Chemicals

- Food and Beverages

- Consumer Goods

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 33.52% of the manufacturing operations management software market share in 2025, giving the region the largest revenue share. The United States supported that lead through dense pharmaceutical, aerospace, semiconductor, and defense production bases that require strict control over electronic records and plant-level traceability. Reshoring and near-shoring programs are also increasing the need to standardize execution systems across new and upgraded facilities. Canada and Mexico add demand through automotive and industrial corridors that align with the United States on common supply chain standards. The region also benefits from a mature integrator and managed-services ecosystem that can shorten deployment cycles relative to markets where OT-IT talent remains more limited.

Asia-Pacific is projected to grow at a 17.88% CAGR, making it the fastest-expanding regional block and the strongest source of future gains in the manufacturing operations management software market during 2026-2031. China and India are widening the addressable base for cloud and hybrid platforms as factories scale digital production models across automotive, electronics, and industrial equipment. Rockwell Automation's 2026 India findings showed that 97% of Indian manufacturers viewed digital transformation as essential, and high-spend respondents devoted materially more operating budget to industrial technology than global peers. This matters because greenfield and fast-scaling facilities in Asia-Pacific can implement newer execution models without the same degree of legacy harmonization required in older industrial estates. Japan and South Korea remain high-value markets where semiconductor and automotive precision keep demand centered on reliable execution control and strong cybersecurity discipline.

Europe remained a high-compliance regional cluster in the manufacturing operations management software market, led by Germany and supported by the United Kingdom, France, and Italy. The EU Cyber Resilience Act is adding stronger documentation and reporting expectations that will influence vendor selection and system architecture across industrial sites selling into Europe. The Middle East is benefiting from greenfield diversification programs in Saudi Arabia and the United Arab Emirates, while Africa is still in an earlier stage, led by South Africa and Egypt. South America is seeing demand concentrate in Brazilian automotive and food processing clusters, where traceability needs align well with pre-configured cloud deployment models.

- ABB Ltd.

- Rockwell Automation, Inc.

- AVEVA Group plc

- Dassault Systems SE

- SAP SE

- Emerson Electric Co.

- Siemens Digital Industries Software

- GE Vernova

- Schneider Electric SE

- Plex Systems, Inc.

- Parsec Automation Corp.

- Accevo Systems (ANT Solutions)

- SYSPRO Inc.

- Aegis Software Inc.

- SedApta S.r.l.

- Infor Inc.

- MPDV Mikrolab GmbH

- ITAC Software Inc.

- ATS Global

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-Driven Real-Time Production Optimization

- 4.2.2 Industry 4.0 and Smart Factory Expansion

- 4.2.3 Cloud-Native and Hybrid MOM Adoption

- 4.2.4 Tighter Quality and Traceability Mandates

- 4.2.5 Digital Product Passport Readiness

- 4.2.6 Execution-Layer AI Copilots for Frontline Decisions

- 4.3 Market Restraints

- 4.3.1 Brownfield Integration and Data Model Complexity

- 4.3.2 OT-IT Skills Shortage and Change Management Friction

- 4.3.3 Cyber Resilience Act and SBOM Compliance Burden

- 4.3.4 Inspection-Ready Digital Record Architecture Costs

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premises

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Function Type

- 5.4.1 Manufacturing Execution System (MES)

- 5.4.2 Planning and Scheduling

- 5.4.3 Quality Process Management

- 5.4.4 Inventory Management

- 5.4.5 Other Function Types (Labor Management, Analytics)

- 5.5 By End-user Industry

- 5.5.1 Aerospace

- 5.5.2 Automotive

- 5.5.3 Pharmaceuticals

- 5.5.4 Medical Equipment

- 5.5.5 Chemicals

- 5.5.6 Food and Beverages

- 5.5.7 Consumer Goods

- 5.5.8 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Rockwell Automation, Inc.

- 6.4.3 AVEVA Group plc

- 6.4.4 Dassault Systems SE

- 6.4.5 SAP SE

- 6.4.6 Emerson Electric Co.

- 6.4.7 Siemens Digital Industries Software

- 6.4.8 GE Vernova

- 6.4.9 Schneider Electric SE

- 6.4.10 Plex Systems, Inc.

- 6.4.11 Parsec Automation Corp.

- 6.4.12 Accevo Systems (ANT Solutions)

- 6.4.13 SYSPRO Inc.

- 6.4.14 Aegis Software Inc.

- 6.4.15 SedApta S.r.l.

- 6.4.16 Infor Inc.

- 6.4.17 MPDV Mikrolab GmbH

- 6.4.18 iTAC Software Inc.

- 6.4.19 ATS Global

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment