PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072587

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072587

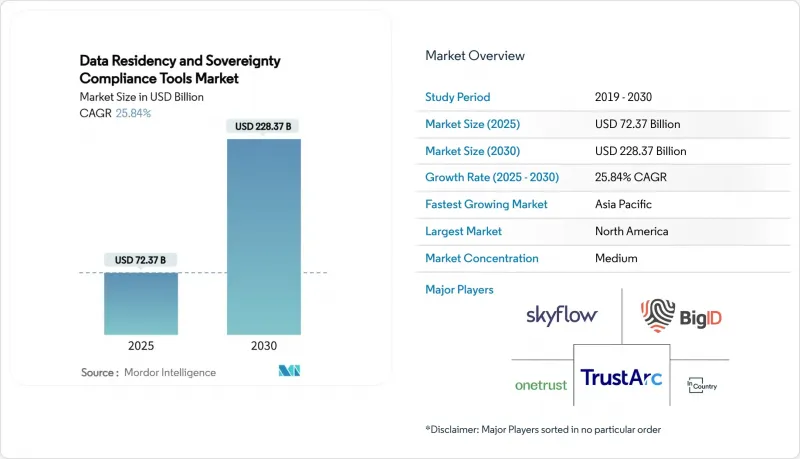

Data Residency and Sovereignty Compliance Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

According to Mordor Intelligence, data residency and Sovereignty Compliance Tools market size reached USD 72.37 billion in 2025 and is forecast to rise to USD 228.37 billion by 2030, implying a compounding CAGR of 25.84%.

This report is Segmented by Deployment Model (On-Premises, Public Cloud, and Hybrid), Tool Type (Data Residency-As-A-Service Platforms, and More), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (BFSI, Healthcare and Life Sciences, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Global Data Residency and Sovereignty Compliance Tools Market Trends and Insights

Proliferation of Strict Data-Localization Laws and Penalties

GDPR enforcement peaked during 2024 with EUR 1.2 billion in fines, while daily breach notifications averaged 363 incidents. China's Network Data Security Management regulations, which took effect in January 2025, layer tiered obligations on firms processing large personal data volumes. India's Digital Personal Data Protection Act introduces extraterritorial reach and penalties up to INR 250 crore (USD 30 million). Similar moves in Indonesia and Malaysia signal Asia-Pacific harmonisation. Collectively, these statutes boost the compliance premium and position the data residency solutions market as a foundational requirement for cross-border operations.

Hyperscaler Sovereign-Cloud Roll-outs

AWS earmarked EUR 7.8 billion (USD 8.8 billion) for European sovereign-cloud infrastructure to be fully operational by end-2025, including EU-resident personnel. Microsoft's Cloud for Sovereignty enables encrypted policy-controlled workloads and continues to add regional key-management options. Oracle and other hyperscalers mirror the blueprint across Asia-Pacific, encouraging enterprises to mix cloud services with jurisdictional controls. These investments enlarge the data residency solutions market by creating plug-in points for independence-certified tooling and advisory overlays.

High Implementation and Orchestration Costs

Deployment often combines infrastructure change, legal consultancy, and ongoing audit management, sending total ownership beyond initial budgets. SMEs feel the pinch most acutely, even though cloud-native residency-as-a-service models help to flatten capital outlays. Vendors that bundle advisory support with automated monitoring find traction, yet macro-economic caution keeps some organisations in pilot phases rather than full roll-outs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Cost of Non-Compliance and Cyber-Breach Litigation

- AI-Model Localization Demands Compliant Data Pipes

- Regulatory Patchwork and Volatility Across Jurisdictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid environments deliver the flexibility to hold sensitive data within sovereign space while leveraging public-cloud cost benefits for non-sensitive workloads. The segment's 30.2% CAGR underscores its role as the agility lever for multinational firms. Public cloud maintains a commanding share due to hyperscaler investment in sovereign zones, whereas on-premises systems remain essential for ultra-regulated workloads such as defense. CIO plans to repatriate selected workloads to further energise demand for configurable placement engines. Vendors able to orchestrate data rules across object stores, private clouds, and colocation footprints are carving a competitive advantage.

The data residency solutions market size attributed to public-cloud deployments is expected to keep expanding as AWS, Microsoft, and Oracle certify additional sovereign regions. At the same time, hybrid solutions increasingly include carbon-aware placement features that shift low-risk data toward facilities powered by renewable energy, fulfilling both compliance and sustainability mandates. As geopolitical tensions rise, many boards consider hybrid policy engines not merely technical tooling but strategic insurance against forced decoupling scenarios.

Data-privacy management suites integrate discovery, classification, and policy enforcement in one console and therefore lead to 2024 revenue. Demand now tilts toward residency-as-a-service offerings that wrap predefined controls, in-country vaults, and automated transfer impact assessments behind subscription pricing. Skyflow's privacy vault supports 150+ jurisdictions, illustrating market appetite for turnkey coverage. Tokenisation and vaulting tools gain particular velocity as zero-trust frameworks become standard for AI workloads.

Spending on governance, risk, and compliance platforms that incorporate residency modules remains steady among highly regulated enterprises that want single-pane consolidation. Meanwhile, sovereign-cloud enablement toolkits optimise Kubernetes clusters to run inside hyperscaler sovereign regions, lowering integration friction. Funding into BigID and similar vendors signals that investors view AI-aligned data hygiene as the next catalyst for the data residency solutions market.

Complete Report Scope:

- By Deployment Model

- On-Premises

- Public Cloud

- Hybrid

- By Tool Type

- Data Residency-as-a-Service Platforms

- Data-Privacy Management Suites

- GRC Platforms with Residency Modules

- Sovereign-Cloud Enablement Tools

- Tokenisation and Data-Vault Solutions

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-Use Industry

- BFSI

- Healthcare and Life Sciences

- Government and Public Sector

- IT and Telecom

- Retail and eCommerce

- Manufacturing and Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held a 38.2% share in 2024, anchored by the US CLOUD Act, Canada's PIPEDA, and expansive hyperscaler footprints. The region serves as a compliance testbed; multinationals refine architectures that reconcile federal, state, and sectoral statutes before rolling them out globally. Recent US policy papers on AI export controls add another jurisdictional layer that platform vendors must encode. Canada's adoption of public cloud up to Protected B classification shows how policy clarity can accelerate rollout while maintaining sovereignty controls.

Asia-Pacific is forecast to register a 28.1% CAGR, the fastest among all regions. India's Digital Personal Data Protection Act, China's Network Data Security Management regulations, and Indonesia's Personal Data Protection Law together form a harmonising backbone that simplifies regional scaling for solution providers. Massive data-centre expansion, driven by AI workloads, provides the physical substrate for residency vaults and sovereign clouds. Multinationals now treat Asia-Pacific localisation budgets as core project lines rather than contingency items, cementing the region's importance within the data residency solutions market.

Europe capitalises on GDPR maturity and hyperscaler sovereign-cloud capital expenditure. AWS's EUR 7.8 billion (USD 8.8 billion) programme includes dedicated EU-resident staff and air-gapped networks. Rising enforcement, evidenced by 2024's fine tally, keeps compliance budgets resilient. The EU AI Act extends governance to algorithmic outputs, intensifying the need for fine-grained audit trails that residency tooling can supply. In the Middle East and Africa, governments are drafting comprehensive privacy frameworks and subsidising cloud campuses to attract foreign investment, opening a greenfield for residency specialists.

- OneTrust, LLC

- TrustArc Inc.

- BigID, Inc.

- InCountry, Inc.

- Skyflow, Inc.

- Riscosity, Inc.

- Odaseva SAS

- Protegrity USA, Inc.

- Privacera, Inc.

- SecuPi Ltd.

- Immuta, Inc.

- Securiti, Inc.

- DataGrail, Inc.

- DataGuard GmbH

- Ketch, Inc.

- Delphix Corporation

- Anonos Inc.

- Data Sentinel Inc.

- Egnyte, Inc.

- Atakama Inc.

- Virtru, Inc.

- Enveil, Inc.

- Evervault Ltd.

- CryptoMove, Inc.

- StrongSalt, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of strict data-localization laws and penalties

- 4.2.2 Hyperscalers' sovereign-cloud roll-outs

- 4.2.3 Rising cost of non-compliance and cyber-breach litigation

- 4.2.4 Residency-as-a-Service platforms reach 70+ nations

- 4.2.5 AI-model localisation demands compliant data pipes

- 4.2.6 Digital-trade pacts embed sovereignty clauses

- 4.3 Market Restraints

- 4.3.1 High implementation and orchestration costs

- 4.3.2 Regulatory patchwork/ volatility across jurisdictions

- 4.3.3 Sustainability-driven data-centre repatriation risk

- 4.3.4 Trade-barrier headwinds for cross-border SaaS

- 4.4 Impact of Macroeconomic Factors

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premises

- 5.1.2 Public Cloud

- 5.1.3 Hybrid

- 5.2 By Tool Type

- 5.2.1 Data Residency-as-a-Service Platforms

- 5.2.2 Data-Privacy Management Suites

- 5.2.3 GRC Platforms with Residency Modules

- 5.2.4 Sovereign-Cloud Enablement Tools

- 5.2.5 Tokenisation and Data-Vault Solutions

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-Use Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Public Sector

- 5.4.4 IT and Telecom

- 5.4.5 Retail and eCommerce

- 5.4.6 Manufacturing and Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 OneTrust, LLC

- 6.4.2 TrustArc Inc.

- 6.4.3 BigID, Inc.

- 6.4.4 InCountry, Inc.

- 6.4.5 Skyflow, Inc.

- 6.4.6 Riscosity, Inc.

- 6.4.7 Odaseva SAS

- 6.4.8 Protegrity USA, Inc.

- 6.4.9 Privacera, Inc.

- 6.4.10 SecuPi Ltd.

- 6.4.11 Immuta, Inc.

- 6.4.12 Securiti, Inc.

- 6.4.13 DataGrail, Inc.

- 6.4.14 DataGuard GmbH

- 6.4.15 Ketch, Inc.

- 6.4.16 Delphix Corporation

- 6.4.17 Anonos Inc.

- 6.4.18 Data Sentinel Inc.

- 6.4.19 Egnyte, Inc.

- 6.4.20 Atakama Inc.

- 6.4.21 Virtru, Inc.

- 6.4.22 Enveil, Inc.

- 6.4.23 Evervault Ltd.

- 6.4.24 CryptoMove, Inc.

- 6.4.25 StrongSalt, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment