PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072619

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072619

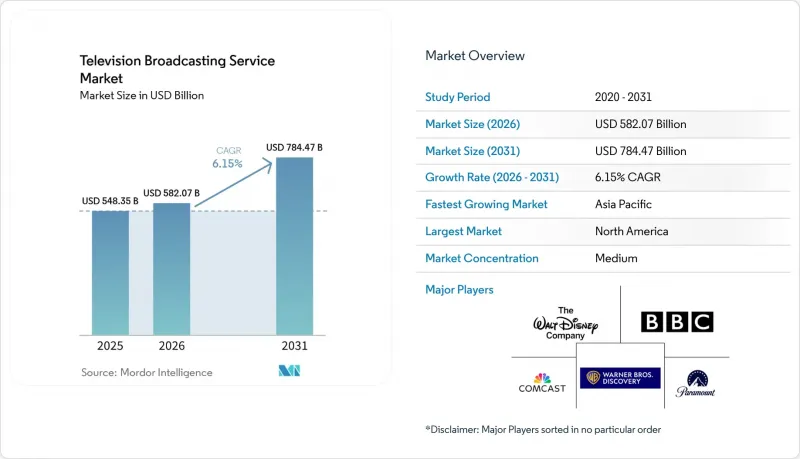

Television Broadcasting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the television broadcasting service market size was valued at USD 548.35 billion in 2025 and estimated to grow from USD 582.07 billion in 2026 to reach USD 784.47 billion by 2031, at a CAGR of 6.15% during the forecast period (2026-2031).

This report is Segmented by Delivery Platform (Terrestrial Broadcast TV, Cable TV, IPTV, OTT/Internet TV, and More), Service Type (Subscription-Based, Advertising-Supported, and More), Broadcaster Type (Public Service, Commercial, and More), Content Genre (Entertainment and Drama, Sports, News and Current Affairs, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Global Television Broadcasting Service Market Trends and Insights

Cord-Cutting Pushes Adoption of OTT and Streaming TV

Streaming's share of total television usage reached 47% in January 2026, a 5.4-point jump in 12 months. Households keep high-speed broadband but cancel multichannel bundles, funneling spending toward a-la-carte apps that bundle on-demand libraries with live linear channels. Comcast lost 10% of domestic linear pay-TV subscribers year-over-year in Q4 2025, yet Peacock added 12% more paid subscribers over the same period. Free ad-supported services accelerate churn from cable because zero subscription cost slashes switching friction; Tubi and The Roku Channel each posted mid-single-digit viewing-share gains by January 2026. Broadcasters therefore prioritize seamless app experiences and robust libraries over carriage negotiations, shifting capital toward direct-to-consumer technology.

Growing Advertiser Demand for Live-Sports Inventory

Sports rights appreciated 113% in value between 2014 and 2024, dwarfing overall advertising growth because brands prize real-time reach and high engagement. Netflix's World Baseball Classic stream in Japan drew 31.4 million viewers, illustrating that even subscription-first platforms will pay premiums for exclusive live events. On FAST services, sports channels enjoyed 105% advertising-revenue growth and 71% higher ad recall than short-form video. Deep-pocketed streamers and national broadcasters thus lock up marquee properties, forcing regional networks to pivot toward niche sports or shoulder programming.

SVOD Platforms Cannibalizing Linear Viewership

Warner Bros Discovery's linear-networks revenue fell 12% year-over-year in Q4 2025 even as streaming subscribers rose to 131.6 million. Linear advertising inventory shrinks alongside audience migration, and per-viewer revenue on SVOD is lower than on scheduled broadcasts. Comcast lost 10% of domestic pay-TV households in Q4 2025, reinforcing a decade-long cord-cutting trend. Broadcasters must therefore fund duplicative infrastructure to run direct-to-consumer apps while still maintaining legacy networks, compressing margins during transition.

Other drivers and restraints analyzed in the detailed report include:

- Broadband and Smart-TV Penetration in Emerging Markets

- Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- Escalating Premium-Rights Acquisition Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OTT and internet TV captured 36.45% of 2025 revenue in the television broadcasting service market and will rise at a 6.57% CAGR to 2031. The surge reflects smart-TV operating systems that foreground streaming apps and mobile networks that zero-rate video traffic. Cable and satellite still anchor rural and maritime distribution, yet subscriber erosion continues as low-earth-orbit broadband promises viable alternatives within three years. Terrestrial broadcast TV benefits from ATSC 3.0 interactivity, but spectrum refarming limits expansion. IPTV's share remains confined to carrier bundles in fiber-rich geographies.

Broadcasters now deploy converged technology stacks so that one asset manifests as a linear channel, an on-demand episode, and a FAST feed with dynamic ad insertion. Paramount unified its Paramount+ and Pluto TV workflows in Q4 2025, cutting per-stream cost by 15%. This model safeguards scale economics while surfing audience preference shifts, ensuring that the television broadcasting service market size for OTT platforms grows without wholly cannibalizing legacy formats.

Advertising-supported offerings controlled 55.78% of 2025 revenue and are projected to expand at a 6.88% CAGR, exceeding subscription growth as households manage budget fatigue. Netflix's ad tier achieved 190 million monthly active users in Q1 2026, materially boosting quarterly revenue of USD 12.25 billion. Roku's USD 1.22 billion Q4 2025 platform revenue validates FAST economics, where higher completion rates and granular targeting lift CPMs.

Subscription services still underpin blockbuster originals but face churn spikes when catalogs stagnate. Hybrid models now dominate: a free, ad-supported on-ramp funnels users toward premium tiers, capturing willingness-to-pay across the income curve. The television broadcasting service market share mix therefore tilts back toward advertising, yet margins improve because programmatic systems automate inventory sales.

Complete Report Scope:

- By Delivery Platform

- Terrestrial Broadcast TV

- Satellite Broadcast TV

- Cable TV

- IPTV

- OTT / Internet TV

- By Service Type

- Subscription-Based Services

- Advertising-Supported Services

- Pay-Per-View / Transactional

- By Broadcaster Type

- Public Service Broadcasters

- Commercial Broadcasters

- Community / Educational Broadcasters

- By Content Genre

- Entertainment and Drama

- Sports

- News and Current Affairs

- Kids and Family

- Other Content Genre

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

Asia-Pacific generated 32.87% of 2025 revenue, buoyed by India's OTT leapfrog and China's state-funded 5G broadcast infrastructure. Zee5's EBITDA-positive milestone at INR 564 million (USD 6.8 million) confirms unit-economics viability for regional-language platforms. South Korea's TVING integration with Wavve boosted advertising 74.7%, and Fuji Television's exclusive Formula 1 rights bet on premium sports loyalty.

Linear platforms in North America and Europe are witnessing a managed decline, which is being offset by the growth of streaming services. By Q1 2026, Peacock achieved a 12% increase in paid subscribers, reaching 46 million, while Comcast's linear base saw a 10% contraction. The FCC's proposed ATSC 1.0 sunset is expediting the transition to IP-centric distribution models. Meanwhile, European quotas and ownership caps are adding complexity to consolidation efforts in the region.

The Middle East is forecast to post the highest 7.98% CAGR, underwritten by sovereign wealth-fund backing of local studios and fiber-to-the-home builds that enable 4K HDR linear channels. South America pivots around Brazil's Globoplay, exceeding 100 million downloads, leveraging Portuguese-language football rights to fend off global entrants. Africa remains nascent because broadband affordability limits mass adoption, but mobile-first models promise catch-up growth in the outer forecast years.

- British Broadcasting Corporation (BBC)

- Comcast Corporation

- Paramount Global

- The Walt Disney Company

- Warner Bros. Discovery, Inc.

- RTL Group S.A.

- Nippon Television Holdings, Inc.

- Fuji Media Holdings, Inc.

- Sky Group Limited

- Mediaset S.p.A.

- Eutelsat Communications S.A.

- Sinclair Broadcast Group, Inc.

- Nexstar Media Group, Inc.

- Seven West Media Limited

- ITV plc

- ProSiebenSat.1 Media SE

- Grupo Globo Comunicacao e Participacoes S.A.

- China Central Television (CCTV)

- Zee Entertainment Enterprises Limited

- CJ ENM Co., Ltd.

- Television Broadcasts Limited (TVB)

- Roku, Inc.

- Amazon.com, Inc. (Freevee)

- Pluto TV LLC

- DAZN Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cord-Cutting Pushes Adoption of OTT and Streaming TV

- 4.2.2 Growing Advertiser Demand for Live-Sports Inventory

- 4.2.3 Broadband and Smart-TV Penetration in Emerging Markets

- 4.2.4 Roll-Out of ATSC 3.0 Enabling Interactive Broadcasts

- 4.2.5 OEM-Backed FAST Channel Ecosystems Gain Traction

- 4.2.6 Cloud-Based Playout Lowers Entry Barriers for Niche Nets

- 4.3 Market Restraints

- 4.3.1 SVOD Platforms Cannibalizing Linear Viewership

- 4.3.2 Local Content and Foreign-Ownership Regulation Caps

- 4.3.3 Escalating Premium-Rights Acquisition Costs

- 4.3.4 Spectrum Refarming for 5G Reduces Terrestrial Capacity

- 4.3.5 Impact of Macroeconomic Factors on the Market

- 4.3.6 Industry Value / Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.7 Threat of New Entrants

- 4.8 Bargaining Power of Suppliers

- 4.9 Bargaining Power of Buyers

- 4.10 Threat of Substitutes

- 4.11 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Delivery Platform

- 5.1.1 Terrestrial Broadcast TV

- 5.1.2 Satellite Broadcast TV

- 5.1.3 Cable TV

- 5.1.4 IPTV

- 5.1.5 OTT / Internet TV

- 5.2 By Service Type

- 5.2.1 Subscription-Based Services

- 5.2.2 Advertising-Supported Services

- 5.2.3 Pay-Per-View / Transactional

- 5.3 By Broadcaster Type

- 5.3.1 Public Service Broadcasters

- 5.3.2 Commercial Broadcasters

- 5.3.3 Community / Educational Broadcasters

- 5.4 By Content Genre

- 5.4.1 Entertainment and Drama

- 5.4.2 Sports

- 5.4.3 News and Current Affairs

- 5.4.4 Kids and Family

- 5.4.5 Other Content Genre

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 British Broadcasting Corporation (BBC)

- 6.4.2 Comcast Corporation

- 6.4.3 Paramount Global

- 6.4.4 The Walt Disney Company

- 6.4.5 Warner Bros. Discovery, Inc.

- 6.4.6 RTL Group S.A.

- 6.4.7 Nippon Television Holdings, Inc.

- 6.4.8 Fuji Media Holdings, Inc.

- 6.4.9 Sky Group Limited

- 6.4.10 Mediaset S.p.A.

- 6.4.11 Eutelsat Communications S.A.

- 6.4.12 Sinclair Broadcast Group, Inc.

- 6.4.13 Nexstar Media Group, Inc.

- 6.4.14 Seven West Media Limited

- 6.4.15 ITV plc

- 6.4.16 ProSiebenSat.1 Media SE

- 6.4.17 Grupo Globo Comunicacao e Participacoes S.A.

- 6.4.18 China Central Television (CCTV)

- 6.4.19 Zee Entertainment Enterprises Limited

- 6.4.20 CJ ENM Co., Ltd.

- 6.4.21 Television Broadcasts Limited (TVB)

- 6.4.22 Roku, Inc.

- 6.4.23 Amazon.com, Inc. (Freevee)

- 6.4.24 Pluto TV LLC

- 6.4.25 DAZN Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment