PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072661

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072661

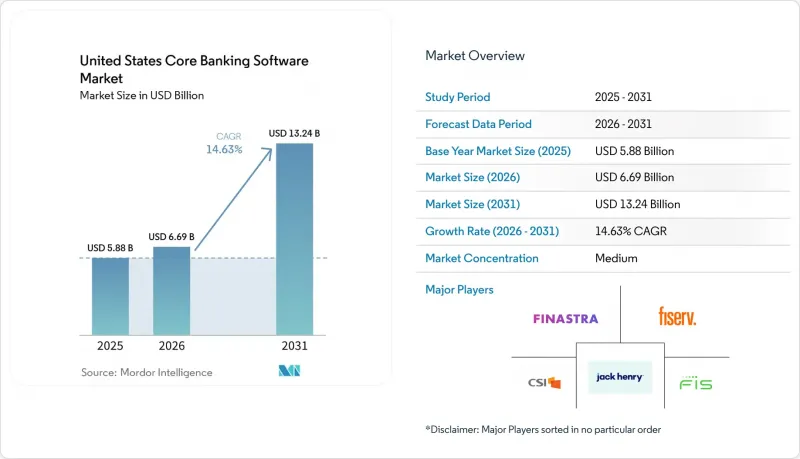

United States Core Banking Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states core banking software market size was valued at USD 5.88 billion in 2025 and estimated to grow from USD 6.69 billion in 2026 to reach USD 13.24 billion by 2031, at a CAGR of 14.63% during the forecast period 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), and End-User (Banks, Non-Bank Financial Institutions, and More (FinTechs and Payment Institutions)). The Market Forecasts are Provided in Terms of Value (USD).

United States Core Banking Software Market Trends and Insights

Cloud-Native Migration Lowering Cost And Release Cycles

Cloud-native architectures are reducing release cycles from quarters to weeks, and that speed gap is turning into a commercial disadvantage for banks still running monolithic cores. U.S. Bank expanded its collaboration with AWS in May 2026 across payment processing, wealth management, and commercial banking applications that support approximately 1.4 million businesses, showing that modernization now spans mission-critical workloads rather than side systems. PeoplesBank completed its move to a modern cloud-native core in September 2025, finished a day ahead of schedule, and re-enrolled more than 19,000 customers in online banking within 24 hours, which gave community institutions a live example of low-disruption conversion execution. These cases show that cloud migration is no longer limited to pilot programs, because both national and community institutions are using it to reset operating models and delivery timelines. Consumption-based infrastructure also changes the cost equation by reducing the fixed overprovisioning that sat inside long-lived mainframe environments. In the United States core banking software market, that combination of faster releases and cleaner cost visibility is making migration timing part of competitive planning rather than a back-office technology decision.

FedNow And RTP Adoption Driving Real-Time Core Upgrades

Real-time payment growth is moving faster than many replacement budgets expected, and the gap between receiving transactions and sending them in real time is exposing weaknesses in batch-oriented core designs. FedNow processed more than USD 850 billion in 2025 and the network had reached around 1,700 financial institutions by April 2026, which shows how quickly the operating baseline has shifted for banks of different sizes. The RTP network also raised its transaction cap from USD 1 million to USD 10 million in February 2025, widening commercial and treasury use cases that require immediate ledger visibility and faster reconciliation. Metropolitan Commercial Bank completed the retirement of its legacy ACH mainframe in February 2026 and moved to Finzly's cloud-native, API-first payment platform, which showed that full decommission is possible and that hybrid workarounds are not the only path. As instant payment throughput rises, banks that still rely on batch-ledger updates face rising operating strain in payments, exception handling, and customer-facing service response. In the US core banking software market, the market keeps real-time readiness tied closely to core replacement timing rather than to standalone payments upgrades.

Conversion Risk And Legacy Integration Complexity At Regional Banks

Conversion risk is most acute at regional institutions in the USD 1 billion to USD 50 billion asset range, where operating complexity is high but IT scale is still limited. A 2025 industry survey found that 35% of banks were dissatisfied with their core processor and 19% were likely to convert at the next renewal date, which shows that demand to switch exists even when execution remains difficult. The challenge usually sits beyond the core itself, because banks often have to remap 30 to 50 or more ancillary systems across payments, treasury, compliance, cards, and digital channels before a cutover can happen. Legacy environments also carry years of undocumented data transformations, and those issues often appear late in validation when timelines are already tight. Longer parallel runs can reduce operational risk, but they also increase program cost, control overhead, and internal fatigue during migration. In the United States core banking software market, that keeps many regional banks cautious even when the long-term case for modernization is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Agentic AI Programs Requiring Event-Driven Core Data

- Mainframe Talent Attrition Accelerating Core Renewal

- Vendor Lock-In And Long Renewal Cycles Slowing Switching

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 61.89% of the United States core banking software market share in 2025, which kept software subscriptions and platform licenses as the largest revenue base for vendors and buyers. Within the US core banking software market size outlook, services are projected to expand at a 14.98% CAGR through 2026-2031, which makes delivery work the faster-growing revenue stream. This mix shows that banks still commit large budgets to the platform itself, but they increasingly need outside help to execute conversion, integration, testing, and control design safely. The demand pressure does not come from one workstream alone, because API exposure, data mapping, payments integration, and compliance preparation often run together during the same replacement program. As a result, implementation capacity has become a constraint that shapes deal timing, vendor selection, and migration sequencing across the US core banking software market.

The services layer is also becoming more recurring as vendors and partners add managed migration, cloud operations, and AI workflow support around the core. That shift improves the economics of service delivery because the relationship continues after go-live instead of ending once the platform is installed. It also changes how buyers assess vendor quality, since delivery depth now affects not only speed but also operating stability and examination readiness. In the United States core banking software industry, certified platform expertise is becoming more valuable because institutions want fewer handoffs across separate advisory, integration, and operations teams. This leaves services positioned as the segment that absorbs the execution demands created by modernization, even while solutions remain the larger base of spending.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By End-User

- Banks

- Non-Bank Financial Institutions

- Other End-users (FinTechs, Payment Institutions)

List of Companies Covered in this Report:

- Fiserv, Inc.

- Jack Henry & Associates, Inc.

- Fidelity National Information Services, Inc.

- Finastra Group Holdings Limited

- Oracle Corporation

- Temenos AG

- Computer Services, Inc.

- Tata Consultancy Services Limited

- EdgeVerve Systems Limited

- Intellect Design Arena Limited

- Nymbus, Inc.

- Corelation, Inc.

- Q2 Holdings, Inc.

- nCino, Inc.

- Mambu GmbH

- Thought Machine Group Limited

- Corelation, Inc.

- ACI Worldwide, Inc.

- Finzly, Inc.

- Finxact, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 FedNow and RTP Adoption Driving Real-Time Core Upgrades

- 4.2.2 Cloud-Native Migration Lowering Cost and Release Cycles

- 4.2.3 Mainframe Talent Attrition Accelerating Core Renewal

- 4.2.4 Open Banking and API Ecosystem Expansion

- 4.2.5 Sponsor-Bank Program Controls Pulling Payments Closer to the Core

- 4.2.6 Agentic AI Programs Requiring Event-Driven Core Data

- 4.3 Market Restraints

- 4.3.1 Conversion Risk and Legacy Integration Complexity at Regional Banks

- 4.3.2 Vendor Lock-In and Long Renewal Cycles Slowing Switching

- 4.3.3 Third-Party and Fourth-Party Scrutiny Raising Due-Diligence Burden

- 4.3.4 Cyber-Resilience and Severe-Outage Recovery Requirements Increasing Migration Scope

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End-User

- 5.3.1 Banks

- 5.3.2 Non-Bank Financial Institutions

- 5.3.3 Other End-users (FinTechs, Payment Institutions)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Fiserv, Inc.

- 6.4.2 Jack Henry & Associates, Inc.

- 6.4.3 Fidelity National Information Services, Inc.

- 6.4.4 Finastra Group Holdings Limited

- 6.4.5 Oracle Corporation

- 6.4.6 Temenos AG

- 6.4.7 Computer Services, Inc.

- 6.4.8 Tata Consultancy Services Limited

- 6.4.9 EdgeVerve Systems Limited

- 6.4.10 Intellect Design Arena Limited

- 6.4.11 Nymbus, Inc.

- 6.4.12 Corelation, Inc.

- 6.4.13 Q2 Holdings, Inc.

- 6.4.14 nCino, Inc.

- 6.4.15 Mambu GmbH

- 6.4.16 Thought Machine Group Limited

- 6.4.17 Corelation, Inc.

- 6.4.18 ACI Worldwide, Inc.

- 6.4.19 Finzly, Inc.

- 6.4.20 Finxact, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment