PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072675

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072675

U.S. Non-PVC IV Bags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

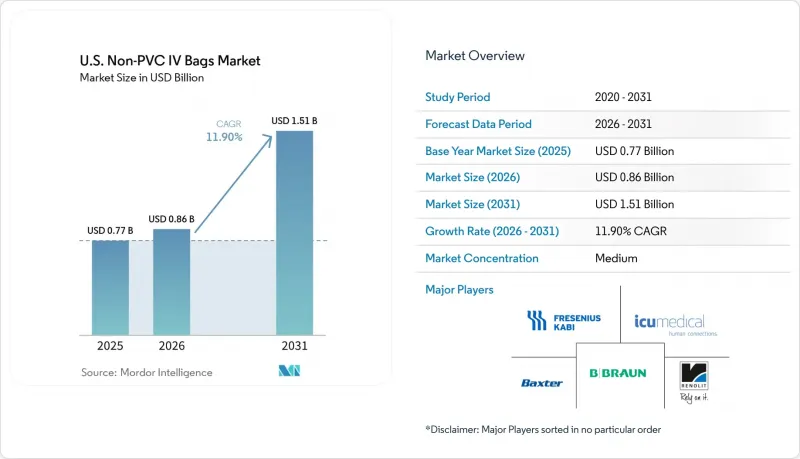

According to Mordor Intelligence, the u.S. non-PVC iV bags market size is projected to be USD 0.77 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.51 billion by 2031, growing at a CAGR of 11.90% from 2026 to 2031.

This report is Segmented by Material (Polypropylene, Polyolefin Blends, EVA, Copolyester Ether, Others), Chamber Configuration (Single-Chamber, Multi-Chamber), Capacity (Below 100 ML, 100-250 ML, 251-500 ML, 501-1, 000 ML, Above 1, 000 ML), Content Type (Liquid, Frozen Mixtures), and End User (Hospitals, Specialty Clinics, Ascs, Others). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Non-PVC IV Bags Market Trends and Insights

DEHP/PVC Phase-Out in High-Risk Patient Cohorts Drives Specification Rewrites

State laws are driving the United States non-PVC IV bags market by setting clear standards for hospitals and suppliers. California's AB 2300, enacted in September 2024, bans DEHP in IV solution containers from 2030 and prohibits substitution with other ortho-phthalates. Pennsylvania's Senate Bill 804, passed in March 2026, follows a similar approach. These regulations are critical in neonatal care, oncology infusion, and long-term parenteral nutrition, where plasticizer migration risks are significant. Hospitals revising specifications for these patient groups often extend changes across broader formularies for easier standardization, accelerating the market's shift to system-wide adoption.

Oncology and Hazardous-Drug Compatibility Needs Redefine Container Selection Standards

In oncology, stricter container selection criteria emphasize compatibility with hazardous drugs, increasing the demand for non-PVC materials. Updated USP standards have shifted focus from cost to container interaction with formulations. Non-PVC options like polypropylene multilayer systems are preferred for their chemical stability and safety. Suppliers such as ICU Medical and Fresenius Kabi are positioning non-PVC formats for critical applications, embedding these specifications into routine practices and stabilizing market demand.

Higher Non-PVC Resin and Conversion Economics Constrain Adoption Rate

The primary barrier to faster adoption is cost, as advanced non-PVC films are priced higher than standard PVC materials. Bag manufacturers face increased expenses due to costly inputs like polypropylene and advanced EVA structures, along with additional investments in equipment. Hospitals and Ambulatory Surgical Centers (ASCs), particularly smaller facilities with fixed-price contracts, struggle to absorb these higher costs. The broader economic benefits of premix use, such as reduced labor and handling, are often overlooked in budget evaluations, slowing the transition despite strong clinical and compliance arguments. Growth in the United States non-PVC IV bags market remains steady, but the pace depends on balancing material safety with cost pressures.

Other drivers and restraints analyzed in the detailed report include:

- Ready-to-Administer and Premix Infusion Adoption Reshapes Compounding Economics

- Domestic Supply-Resilience Sourcing Accelerates Nearshoring Investment

- Drug-Container Compatibility and Validation Burden Slows Formulary Transitions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, EVA accounted for 47.65% of revenue, making it the leading material in the United States non-PVC IV bags market. Its dominance stems from broad drug compatibility, clear visibility for inspections, and stable freeze-thaw performance, making it ideal for frozen antibiotics, electrolyte solutions, and blood-compatible formulations. EVA's versatility supports standardized bag formats, reinforcing its position as the market's foundation.

Polypropylene, growing at a 13.20% CAGR through 2031, is gaining traction in specialized applications like oncology and multi-chamber parenteral nutrition systems. Its advantages include hazardous-drug compatibility and suitability for advanced multi-layer construction. Innovations like Fresenius Kabi's patent for multilayer infusion bags highlight the material's expanding role in premium clinical applications.

Single-chamber bags held 65.55% of revenue in 2025, maintaining their lead in the United States non-PVC IV bags market. Their straightforward use in fluid replacement and routine infusions, coupled with ease of manufacturing and alignment with nursing workflows, ensures their continued dominance.

Multi-chamber bags, projected to grow at a 12.10% CAGR through 2031, address the demand for ready-to-mix products in parenteral nutrition and antibiotic combinations. These bags simplify sterile preparation, reduce compounding errors, and align with standardized workflows, driving their growth in the market.

Complete Report Scope:

- By Material

- Polypropylene

- Polyolefin blends

- Ethylene Vinyl Acetate (EVA)

- Copolyester / Copolyester Ether

- Ethylene-Propylene Copolymer and Other Multilayer Films

- By Chamber Configuration

- Single-chamber bags

- Multi-chamber bags

- By Capacity

- Below 100 mL

- 100 mL to 250 mL

- 251 mL to 500 mL

- 501 mL to 1,000 mL

- Above 1,000 mL

- By Content Type

- Liquid Mixtures

- Frozen Mixtures

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

List of Companies Covered in this Report:

- Amcor plc

- B. Braun

- Baxter

- Central Admixture Pharmacy Services, Inc. (CAPS)

- Eastman Chemical Company

- Epic Medical Pte. Ltd.

- Fagron Sterile Services US

- Fresenius

- Hospira, Inc.

- ICU Medical

- Kraton

- Laboratorios Grifols, S.A.

- Otsuka Pharmaceutical Factory, Inc.

- Pfizer

- PolyCine GmbH

- RENOLIT

- Sealed Air Corporation

- Technoflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DEHP/PVC Phase-Out in High-Risk Patient Cohorts

- 4.2.2 Oncology and Hazardous-Drug Compatibility Needs

- 4.2.3 Ready-To-Administer and Premix Infusion Adoption

- 4.2.4 Domestic Supply-Resilience Sourcing After IV Fluid Disruptions

- 4.2.5 USP <797>-Driven Container Validation in Sterile Compounding

- 4.2.6 State-Level Non-DEHP Compliance and Sustainability-Led Purchasing

- 4.3 Market Restraints

- 4.3.1 Higher Non-PVC Resin and Conversion Economics

- 4.3.2 Drug-Container Compatibility and Validation Burden

- 4.3.3 Installed-Base PVC Workflow Lock-in

- 4.3.4 Non-DEHP Versus Non-PVC Labeling Ambiguity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Polypropylene

- 5.1.2 Polyolefin blends

- 5.1.3 Ethylene Vinyl Acetate (EVA)

- 5.1.4 Copolyester / Copolyester Ether

- 5.1.5 Ethylene-Propylene Copolymer and Other Multilayer Films

- 5.2 By Chamber Configuration

- 5.2.1 Single-chamber bags

- 5.2.2 Multi-chamber bags

- 5.3 By Capacity

- 5.3.1 Below 100 mL

- 5.3.2 100 mL to 250 mL

- 5.3.3 251 mL to 500 mL

- 5.3.4 501 mL to 1,000 mL

- 5.3.5 Above 1,000 mL

- 5.4 By Content Type

- 5.4.1 Liquid Mixtures

- 5.4.2 Frozen Mixtures

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty Clinics

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amcor plc

- 6.3.2 B. Braun Medical Inc.

- 6.3.3 Baxter International Inc.

- 6.3.4 Central Admixture Pharmacy Services, Inc. (CAPS)

- 6.3.5 Eastman Chemical Company

- 6.3.6 Epic Medical Pte. Ltd.

- 6.3.7 Fagron Sterile Services US

- 6.3.8 Fresenius Kabi AG

- 6.3.9 Hospira, Inc.

- 6.3.10 ICU Medical, Inc.

- 6.3.11 Kraton Corporation

- 6.3.12 Laboratorios Grifols, S.A.

- 6.3.13 Otsuka Pharmaceutical Factory, Inc.

- 6.3.14 Pfizer Inc.

- 6.3.15 PolyCine GmbH

- 6.3.16 RENOLIT SE

- 6.3.17 Sealed Air Corporation

- 6.3.18 Technoflex

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment