PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072694

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072694

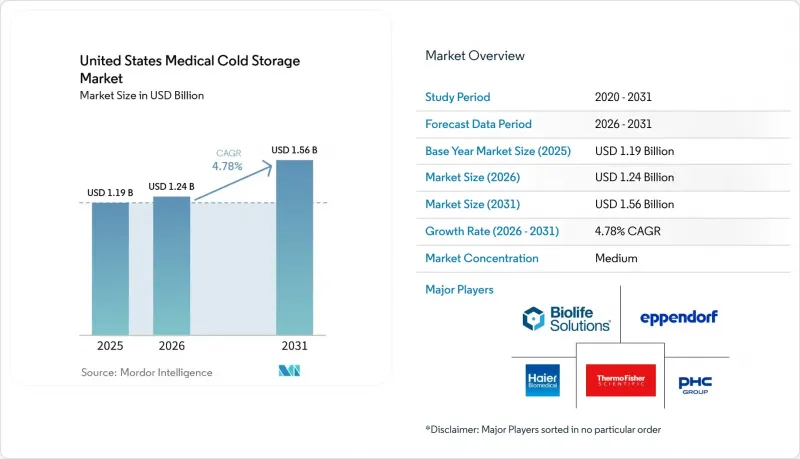

United States Medical Cold Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states medical cold storage market size is expected to grow from USD 1.19 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.56 billion by 2031 at 4.78% CAGR over 2026-2031.

This report is Segmented by Product Type (Refrigerators, Freezers, Cryogenic Storage, Walk-Ins, Monitoring Systems), Temperature Range (CRT, Refrigerated, Frozen, Ultra-Low, Cryogenic), Application (Vaccines, Blood Components, Biologics, Cell/Gene Therapies, Lab Specimens, Organs/Tissues), and End User (Hospitals, Pharmacies, Blood Banks, Labs, Pharma/Biotech, CROs/CMOs). Forecasts in Value (USD).

United States Medical Cold Storage Market Trends and Insights

Expanding Biologics and Specialty-Drug Cold Storage Demand

The United States medical cold storage market is gaining durable support from the growing number of biologics that need validated handling across manufacturing, distribution, and care delivery sites. Biocon Biologics received FDA approval in 2025 for Kirsty, an interchangeable rapid-acting insulin aspart, which widened cold chain requirements across pharmacies, hospital outpatient departments, and specialty care settings. Each new biologic launch adds storage needs beyond the manufacturer because the same product must move through distribution nodes, hospital pharmacies, and monitored clinical inventories before administration. That pattern matters for the United States medical cold storage market because it creates repeat replacement demand across the full chain instead of tying equipment sales to a single launch event. Storage validation standards also keep procurement tied to compliance, which makes purpose-built refrigeration and freezer capacity harder to postpone than general equipment purchases. As biologics portfolios widen, the United States medical cold storage market continues to shift toward regulated assets that must meet documentation, temperature uniformity, and monitoring expectations in daily operations.

Cell and Gene Therapy Scale-Up Requiring Cryogenic Capacity

The United States medical cold storage market is also being lifted by the expansion of commercial cell and gene therapy programs that depend on cryogenic handling. Cryoport stated in its first quarter 2026 results that it supports 21 commercially approved CGTs and 766 active clinical trials globally, with 569 in the Americas, which shows the scale of programs requiring specialized storage and logistics. BioLife Solutions reported in May 2026 that its biopreservation media were embedded in 17 approved CGT products, with 9 additional approvals or expansions anticipated within 12 months, which points to continuing demand for validated cryogenic workflows. Unlike vaccine inventories, autologous therapies need a dedicated labeled cryogenic position for each patient lot, so storage demand rises with every treatment slot rather than only with bulk batch volumes. That patient-specific model gives the United States medical cold storage market a strong growth layer in cryogenic systems, especially at outsourced manufacturing and processing sites where chain-of-custody controls are most intensive. It also keeps procurement concentrated among vendors that can pair physical storage with validation support, remote diagnostics, and documented audit trails.

High Capital and Lifecycle Energy Costs of ULT Assets

The United States medical cold storage market still faces a real cost barrier from ultra-low temperature equipment, especially in settings with tight capital approval cycles. Purchase prices remain high for compliance-grade -80°C systems, and the cost burden rises further when facilities add calibration, service contracts, backup power integration, and future refrigerant-related adjustments. The University of California, Santa Barbara, estimated a 6 to 13 year payback period for ENERGY STAR ULT replacements, even with strong energy savings, which shows why many facilities delay upgrades despite clear operating benefits. This slows parts of the United States medical cold storage market because smaller hospitals, independent laboratories, and rural health systems often cannot replace aging units on the same timetable as large academic centers. Even when energy-efficient alternatives are available, procurement teams must weigh upfront premiums against long replacement cycles and site-specific budget limits. The result is a market where replacement intent is present, but actual conversion can move slowly outside well-funded institutions.

Other drivers and restraints analyzed in the detailed report include:

- Tighter FDA, CDC, and Accreditation Compliance Requirements

- Rising Vaccine Inventory Complexity Across Care Settings

- Refrigerant-Transition Procurement Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical-grade freezers accounted for 52.43% of the United States medical cold storage market size in 2025, which made them the largest product category by revenue. Their lead came from wide use across blood components, specialty biologics, and research sample preservation, where -20°C to -90°C performance is routine. The United States medical cold storage market continues to rely on this category because freezers serve the broadest mix of healthcare, research, and biopharma applications. Procurement activity within the category is centered on units that can combine temperature stability, alarm systems, and documented compliance features in one platform. The VA Long Beach 2025 solicitation for TSX Universal Series -80°C freezers showed how buyers are now specifying dual-cascade refrigerants and extended warranty expectations, which favors established suppliers with validated product lines.

Medical-grade refrigerators remain the installed volume base for pharmacy, vaccine, blood bank, and laboratory use, but the demand pattern is more mature, and replacement-led rather than expansion-led. These units still matter because broad ambulatory and hospital use gives them a large installed footprint across the United States medical cold storage market. Walk-in cold rooms and cryogenic systems serve narrower but higher-intensity use cases, especially where GMP biorepository functions or advanced therapy handling are involved. Monitoring systems and accessories are forecast to grow at a 6.36% CAGR through 2031, which makes them the fastest-growing product grouping as digital compliance shifts from optional to expected. That growth reflects a practical change in buying behavior, because facilities increasingly need traceable logs, automated alerts, and audit-ready dashboards rather than manual temperature records alone.

Cryogenic storage is still smaller in current revenue terms, but it represents the highest-intensity capital deployment area inside this product mix. The main reason is that cell and gene therapy workflows require purpose-built storage conditions and documented chain-of-custody controls that cannot be served by standard freezer platforms. Cryoport's MVE Biological Solutions introduced the Fusion 800 Series self-sustaining cryogenic freezer in the first quarter of 2026, which addressed one of the main operational limits of cryogenic adoption by reducing dependence on continuous liquid nitrogen supply. That type of product development shows how the US medical cold storage industry is responding to operational pain points, not just temperature targets. It also means product competition is moving toward integrated system design, where safety, remote oversight, and cryogenic workflow fit matter as much as pure cabinet performance.

The monitoring category is gaining from the same compliance shift, but with a different value proposition. Buyers increasingly want storage assets that can produce documentation without relying on manual intervention, which supports remote diagnostics and easier survey preparation. PHC's TwinGuard ECO 703VXH launch in January 2026 reflected this shift by pairing ultra-low performance with remote diagnostics and optional identity-based access control. In the United States medical cold storage market, that combination turns monitoring from an accessory purchase into a core part of product qualification. Over time, this is likely to widen the gap between vendors selling compliant platforms and vendors competing mainly on cabinet hardware.

Ultra-low storage represented 43.21% of the United States medical cold storage market size in 2025, which made it the largest temperature band by value. This range remains central because many biologics, research samples, and advanced therapy materials are stabilized at very low temperatures under validated handling protocols. The United States medical cold storage market depends heavily on ultra-low systems because they sit at the intersection of research, blood-related applications, specialty therapeutics, and outsourced biomanufacturing. Demand here is not only broad but also specification-heavy because buyers increasingly want energy efficiency, redundancy, and audit support in the same unit. That is why product launches in this band carry outsized weight in competitive positioning.

PHC Corporation of North America launched the TwinGuard ECO 703VXH in January 2026 with 7.3 kWh per day consumption at a -80°C setpoint, natural refrigerants, and inverter-controlled dual compressor redundancy. The launch matters because it addressed three purchase criteria at once, which were energy costs, backup protection, and low-GWP transition readiness. In the United States medical cold storage market, vendors that solve all three issues together are better placed than those that treat them as separate procurement decisions. Refrigerated storage at 2°C to 8°C remains a stable and large installed base because vaccines, medications, and blood-related applications continue to need it every day. Frozen storage at -20°C to -40°C also stays relevant for plasma products, vaccine variants, and specimen archiving, but it does not face the same degree of capital intensity as the ultra-low tier.

Cryogenic storage at or below -150°C is projected to grow at a 5.87% CAGR through 2031, which is the fastest rate across temperature sub-segments. That pace reflects the spread of advanced therapy workflows that need vapor-phase liquid nitrogen conditions and tighter chain-of-custody requirements. The United States medical cold storage market is therefore being reshaped by a two-speed temperature structure where ultra-low remains the core revenue base and cryogenic storage defines the highest strategic growth. This split is important because it changes vendor priorities, site planning, and service needs at the same time. Buyers are no longer looking only for temperature performance, but also for documentation, energy profile, facility fit, and refrigerant compliance within each range.

That shift has wider implications for competition and replacement cycles. Ultra-low systems face immediate pressure from operating cost concerns and refrigerant transitions, while cryogenic systems face stronger pressure from workflow design and patient-specific handling. Cryometrix's T-90 platform illustrates the push toward closed-loop, LN2-free cryogenic approaches that address containment and compliance needs in a differentiated way. In practical terms, the US medical cold storage industry is moving toward more specialized product stacks inside each temperature band. The deeper the storage requirement, the more likely equipment qualification becomes tied to end-use process design rather than only to generic capacity needs.

Complete Report Scope:

- By Product Type

- Medical-Grade Refrigerators

- Pharmacy / Vaccine Refrigerators

- Blood Bank Refrigerators

- Laboratory / General-Purpose Refrigerators

- Medical-Grade Freezers

- Low-Temperature Freezers (-20°C to -40°C)

- Ultra-Low Temperature Freezers (-60°C to -90°C)

- Cryogenic Storage Systems (<=-150°C)

- Walk-in Cold Rooms & Chambers

- Monitoring Systems & Accessories

- Medical-Grade Refrigerators

- By Storage Temperature Range

- Controlled Room Temperature / Ambient

- Refrigerated (+2°C to +8°C)

- Frozen (-20°C to -40°C)

- Ultra-Low (-60°C to -90°C)

- Cryogenic (<=-150°C)

- By Application

- Vaccines

- Blood & Blood Components

- Medications & Biologics

- Cell & Gene Therapies

- Laboratory / Diagnostic Specimens

- Organs & Tissues

- By End User

- Hospitals & Health Systems

- Pharmacies & Vaccination Sites

- Blood Banks & Transfusion Centers

- Academic & Research Laboratories

- Pharmaceutical & Biotechnology Companies

- CROs, CMOs & Cell Therapy Processing Sites

List of Companies Covered in this Report:

- Accucold

- Aegis Scientific, Inc.

- ARCTIKO A/S

- B Medical Systems S.a r.l.

- BioLife Solutions

- Binder

- Desmon S.p.A.

- Eppendorf

- Follett Products, LLC

- Haier Biomedical

- Helmer Scientific

- LabRepCo, LLC

- Liebherr Group

- Migali Scientific

- NuAire, Inc.

- PHC Holdings

- Philipp Kirsch

- So-Low Environmental Equipment Co.

- Thermo Fisher Scientific

- Vestfrost Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Biologics and Specialty-Drug Cold Storage Demand

- 4.2.2 Rising Vaccine Inventory Complexity Across Care Settings

- 4.2.3 Tighter FDA, CDC, and Accreditation Compliance Requirements

- 4.2.4 Cell And Gene Therapy Scale-Up Requiring Cryogenic Capacity

- 4.2.5 ENERGY STAR-Led Replacement of Aging Installed Base

- 4.2.6 Decentralized Clinical Trials Creating Distributed Storage Nodes

- 4.3 Market Restraints

- 4.3.1 High Capital and Lifecycle Energy Costs of ULT Assets

- 4.3.2 Calibration, Monitoring, and Audit Burden Across Facilities

- 4.3.3 Refrigerant-Transition Procurement Complexity

- 4.3.4 Backup-Power and Disaster-Resilience Requirements

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Medical-Grade Refrigerators

- 5.1.1.1 Pharmacy / Vaccine Refrigerators

- 5.1.1.2 Blood Bank Refrigerators

- 5.1.1.3 Laboratory / General-Purpose Refrigerators

- 5.1.2 Medical-Grade Freezers

- 5.1.2.1 Low-Temperature Freezers (-20°C to -40°C)

- 5.1.2.2 Ultra-Low Temperature Freezers (-60°C to -90°C)

- 5.1.3 Cryogenic Storage Systems (<=-150°C)

- 5.1.4 Walk-in Cold Rooms & Chambers

- 5.1.5 Monitoring Systems & Accessories

- 5.1.1 Medical-Grade Refrigerators

- 5.2 By Storage Temperature Range

- 5.2.1 Controlled Room Temperature / Ambient

- 5.2.2 Refrigerated (+2°C to +8°C)

- 5.2.3 Frozen (-20°C to -40°C)

- 5.2.4 Ultra-Low (-60°C to -90°C)

- 5.2.5 Cryogenic (<=-150°C)

- 5.3 By Application

- 5.3.1 Vaccines

- 5.3.2 Blood & Blood Components

- 5.3.3 Medications & Biologics

- 5.3.4 Cell & Gene Therapies

- 5.3.5 Laboratory / Diagnostic Specimens

- 5.3.6 Organs & Tissues

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Pharmacies & Vaccination Sites

- 5.4.3 Blood Banks & Transfusion Centers

- 5.4.4 Academic & Research Laboratories

- 5.4.5 Pharmaceutical & Biotechnology Companies

- 5.4.6 CROs, CMOs & Cell Therapy Processing Sites

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Accucold

- 6.3.2 Aegis Scientific, Inc.

- 6.3.3 ARCTIKO A/S

- 6.3.4 B Medical Systems S.a r.l.

- 6.3.5 BioLife Solutions, Inc.

- 6.3.6 BINDER GmbH

- 6.3.7 Desmon S.p.A.

- 6.3.8 Eppendorf SE

- 6.3.9 Follett Products, LLC

- 6.3.10 Haier Biomedical

- 6.3.11 Helmer Scientific Inc.

- 6.3.12 LabRepCo, LLC

- 6.3.13 Liebherr Group

- 6.3.14 Migali Scientific

- 6.3.15 NuAire, Inc.

- 6.3.16 PHC Holdings Corporation

- 6.3.17 Philipp Kirsch GmbH

- 6.3.18 So-Low Environmental Equipment Co.

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Vestfrost Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment