PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072700

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072700

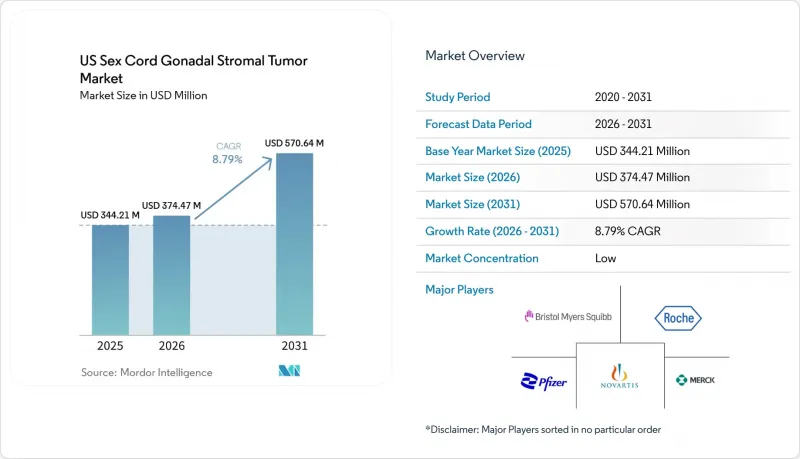

US Sex Cord Gonadal Stromal Tumor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the US sex cord gonadal stromal tumor market size is projected to expand from USD 344.21 million in 2025 and USD 374.47 million in 2026 to USD 570.64 million by 2031, registering a CAGR of 8.79% between 2026 to 2031.

This report is Segmented by Tumor Type (Adult Granulosa Cell, Juvenile Granulosa Cell, Sertoli-Leydig Cell, Thecoma, Fibroma and Fibrothecoma, Steroid Cell, and Other Sex Cord Tumors), Product Type (Diagnosis and Treatment), and End User (Hospitals, Specialty Cancer Centers, Ambulatory Surgical Centers, Diagnostic Laboratories, and Academic Institutes). Market Forecasts are in Terms of Value (USD).

US Sex Cord Gonadal Stromal Tumor Market Trends and Insights

Rising FDA-Backed Treatment Access for Rare Ovarian Sex Cord-Stromal Tumors

The FDA approved Verastem's Avmapki Fakzynja Co-Pack in May 2025, combining avutometinib and defactinib for KRAS-mutated recurrent low-grade serous ovarian cancer. This approval highlights the potential of precision oncology and sets a precedent for hormone-sensitive ovarian tumor treatments. It demonstrates that niche, molecularly defined segments can achieve regulatory approval and secure 7-year Orphan Drug exclusivity. The FDA's Real-Time Oncology Review is encouraging biomarker-driven strategies like FOXL2, DICER1, and NOTCH1 in the United States sex cord gonadal stromal tumor market, where competition remains limited.

Expanding Biomarker-Driven Patient Identification

Biomarker testing is broadening the patient base in the United States sex cord gonadal stromal tumor market. Institutions like UCSF Health and Mayo Clinic Laboratories now offer FOXL2 C402G testing through standardized workflows, enabling faster treatment planning and reliable monitoring. A 2025 study showed FOXL2-mutant circulating tumor DNA predicts post-operative disease progression in adult granulosa cell tumors. Another study highlighted that DICER1-mutant Sertoli-Leydig cell tumors have higher proliferative activity and worse prognosis, emphasizing the importance of genotyping at diagnosis. These advancements enhance diagnostic accuracy and create recurring revenue streams.

Very Small Eligible Patient Pool and Late Recurrence Patterns

The United States market for sex cord gonadal stromal tumors faces constraints due to a small patient base, with only 1,500-2,000 new cases annually. Adult granulosa cell tumors add complexity as recurrences often occur years after diagnosis, spreading demand over an extended timeline. A 2024 study in the Journal of Ovarian Research reported recurrence rates of 6-48%, with 50-80% of fatal cases occurring after relapse. Treatment intensity is concentrated on a small recurrent subset, limiting market growth more by disease epidemiology than treatment adoption.

Other drivers and restraints analyzed in the detailed report include:

- Growing Clinical Use of Surgery Plus Systemic Therapy

- Increasing Trial Activity in Low-Grade Serous and Granulosa Cell Tumors

- High Dependence on Expert Pathology and Molecular Confirmation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, adult granulosa cell tumors accounted for 59.6% of the United States sex cord gonadal stromal tumor market. Juvenile granulosa cell tumors are projected to grow at a 9.88% CAGR through 2031. Adult-type tumors dominate revenue due to their clinical prevalence and long-term recurrence, which drives extended surveillance and treatment. CDK4/6 inhibitor combinations are gaining traction as a later-line option for recurrent adult granulosa cell tumors, with studies showing partial response rates of 27.3% and stable disease rates of 54.5%. Juvenile granulosa cell tumors are expanding faster due to increased DICER1-focused pediatric programs, while Sertoli-Leydig cell tumors are becoming diagnostically significant with TERT and TP53 mutations indicating a less favorable prognosis. Thecomas, fibroma/fibrothecomas, and steroid cell tumors maintain stable demand, with potential for future advancements as molecular features are clarified.

Complete Report Scope:

- By Tumor Type

- Adult Granulosa Cell Tumor

- Juvenile Granulosa Cell Tumor

- Sertoli-Leydig Cell Tumor

- Thecoma

- Fibroma and Fibrothecoma

- Steroid Cell Tumor

- Other Sex Cord Gonadal Stromal Tumors

- By Product Type

- Diagnosis

- Imaging

- Histopathology

- Immunohistochemistry

- Molecular Testing

- Tumor Marker Testing

- Treatment

- Surgery

- Chemotherapy

- Hormonal Therapy

- Targeted Therapy

- Immunotherapy

- Radiation Therapy

- Diagnosis

- By End User

- Hospitals

- Specialty Cancer Centers

- Ambulatory Surgical Centers

- Diagnostic Laboratories

- Academic and Research Institutes

List of Companies Covered in this Report:

- Abbvie

- Amgen

- AstraZeneca

- Bayer

- Biocon Biologics Inc.

- Bristol-Myers Squibb

- Eisai

- Eli Lilly and Company

- Roche

- Genentech

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Merck

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceuticals Industries

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Verastem, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising FDA-Backed Treatment Access for Rare Ovarian Subtypes

- 4.2.2 Expanding Biomarker-Driven Patient Identification

- 4.2.3 Growing Clinical Use of Surgery Plus Systemic Therapy Pathways

- 4.2.4 Increasing Trial Activity in Low-Grade Serous and Granulosa Cell Disease

- 4.2.5 Improved Referral Networks to Sarcoma and Gynecologic Oncology Centers

- 4.2.6 Wider Adoption of Oral Targeted and Hormonal Regimens

- 4.3 Market Restraints

- 4.3.1 Very Small Eligible Patient Pool and Late Recurrence Pattern

- 4.3.2 High Dependence on Expert Pathology and Molecular Confirmation

- 4.3.3 Limited Label-Specific Commercial Products for Most Subtypes

- 4.3.4 Reimbursement Friction for Off-Label Hormonal and Targeted Use

- 4.4 Value Chain and Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Tumor Type

- 5.1.1 Adult Granulosa Cell Tumor

- 5.1.2 Juvenile Granulosa Cell Tumor

- 5.1.3 Sertoli-Leydig Cell Tumor

- 5.1.4 Thecoma

- 5.1.5 Fibroma and Fibrothecoma

- 5.1.6 Steroid Cell Tumor

- 5.1.7 Other Sex Cord Gonadal Stromal Tumors

- 5.2 By Product Type

- 5.2.1 Diagnosis

- 5.2.1.1 Imaging

- 5.2.1.2 Histopathology

- 5.2.1.3 Immunohistochemistry

- 5.2.1.4 Molecular Testing

- 5.2.1.5 Tumor Marker Testing

- 5.2.2 Treatment

- 5.2.2.1 Surgery

- 5.2.2.2 Chemotherapy

- 5.2.2.3 Hormonal Therapy

- 5.2.2.4 Targeted Therapy

- 5.2.2.5 Immunotherapy

- 5.2.2.6 Radiation Therapy

- 5.2.1 Diagnosis

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Cancer Centers

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Academic and Research Institutes

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca PLC

- 6.3.4 Bayer AG

- 6.3.5 Biocon Biologics Inc.

- 6.3.6 Bristol-Myers Squibb Company

- 6.3.7 Eisai Co., Ltd.

- 6.3.8 Eli Lilly and Company

- 6.3.9 F. Hoffmann-La Roche AG

- 6.3.10 Genentech, Inc.

- 6.3.11 GSK plc

- 6.3.12 Hikma Pharmaceuticals PLC

- 6.3.13 Merck & Co., Inc.

- 6.3.14 Novartis AG

- 6.3.15 Pfizer Inc.

- 6.3.16 Sanofi S.A.

- 6.3.17 Sun Pharmaceutical Industries Limited

- 6.3.18 Takeda Pharmaceutical Company Limited

- 6.3.19 Teva Pharmaceutical Industries Limited

- 6.3.20 Verastem, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment