PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072726

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072726

GCC Swollen Knee Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

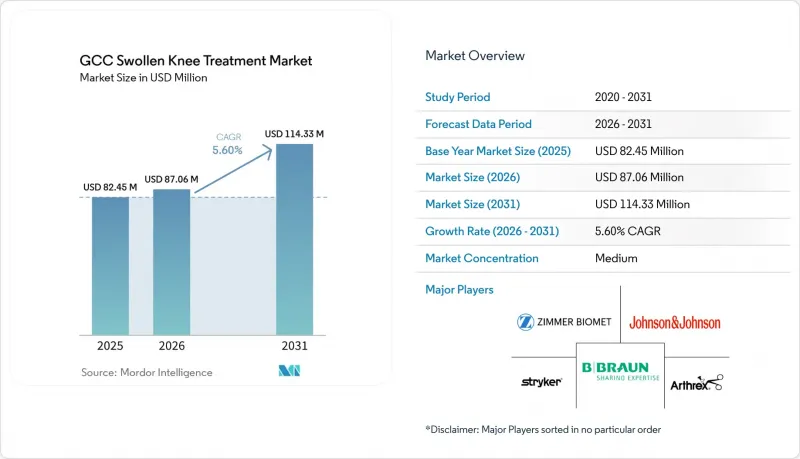

According to Mordor Intelligence, the GCC swollen knee treatment market size is expected to increase from USD 82.45 million in 2025 to USD 87.06 million in 2026 and reach USD 114.33 million by 2031, growing at a CAGR of 5.60% over 2026-2031.

This report is Segmented by Treatment Type (Pharmacological, Non-Pharmacological, Minimally Invasive, Surgical), Cause (OA, Sports Injury, RA, Bursitis, Post-Traumatic), Route (Oral, Topical, Injectable, Procedural), End User (Hospitals, Ortho Clinics, Ascs, Rehab Centers, Home Care), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Rest of GCC). Forecasts in Value (USD).

GCC Swollen Knee Treatment Market Trends and Insights

Rising Knee Osteoarthritis Burden Across GCC Countries

Knee osteoarthritis (OA) in the GCC is no longer confined to the elderly, impacting both national and expatriate populations. Women often face a higher burden, and working-age adults are entering treatment earlier. Between 1990 and 2024, Bahrain and the UAE recorded some of the steepest global increases in knee OA incidence. This long-term trend is driving repeated demand for analgesics, injections, rehabilitation, and imaging. As orthopedic access improves, the GCC swollen knee treatment market is expected to capture a larger share of untreated cases.

Growth In Obesity And Diabetes Linked To Joint Inflammation

High obesity and diabetes rates in the GCC are expanding the patient base for swollen knee treatments through mechanical stress and inflammation. From 2020 to 2024, over 65% of Saudi adults were classified as overweight or obese. In 2024, the MENA region had 84.7 million adults with diabetes, with a prevalence of 17.6%. These conditions complicate treatment and follow-up care, increasing demand for precise dosing and specialist oversight in the GCC swollen knee treatment market.

Limited Local Clinical Standardization For Swollen Knee Pathways

Inconsistent clinical standards across the GCC hinder efficient patient treatment. Referral practices vary significantly, leading to different treatment approaches for similar cases. This inconsistency impacts the adoption of premium therapies. Regulatory fragmentation further complicates product approvals and reimbursement processes, creating challenges for suppliers, especially with newer treatments. Without standardization, the GCC swollen knee treatment market will remain below its potential.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Private Orthopedic And Sports Medicine Clinics

- Wider Adoption Of Minimally Invasive Injection Therapies

- High Out-Of-Pocket Cost For Repeated Injection-Based Care

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, pharmacological treatments accounted for 31.1% of the GCC swollen knee treatment market, highlighting the reliance on drug-based management for early and mid-stage care. Oral NSAIDs, topical diclofenac, and hospital-administered analgesics dominate due to their established use in primary care, emergency settings, and outpatient follow-ups. Corticosteroids remain significant but are used cautiously in diabetic patients due to potential complications in glucose management. Non-pharmacological treatments are gaining traction with expanded rehabilitation networks, while surgical treatments are shifting towards minimally invasive arthroscopy and shorter recovery pathways.

Minimally invasive procedures are projected to grow at a 5.98% CAGR through 2031, driven by physician acceptance of viscosupplementation and PRP, improved imaging-guided delivery, and patient preference for non-surgical options. These procedures align with ambulatory care economics, offering faster delivery and higher per-episode value. Anika Therapeutics reported 16% growth in international osteoarthritis pain management revenue in 2024, supported by geographic expansion into markets like the GCC. This trend is reshaping the treatment mix, moving care towards planned outpatient procedures over repeat symptomatic medication.

Osteoarthritis led the GCC swollen knee treatment market in 2025 with a 32.4% share, driven by obesity trends, an aging population, and improved early diagnosis of degenerative diseases. Obesity-related cytokines like leptin and TNF-a are linked to synovial inflammation, intensifying some cases through metabolic pathways. Rheumatoid arthritis and other inflammatory conditions, though smaller in volume, require complex biologic and specialist care. Secondary cases like bursitis, tendinitis, and post-traumatic swelling remain significant, especially in labor-intensive sectors, ensuring a diverse clinical mix in the market.

Sports injuries are forecasted to grow at a 6.25% CAGR from 2026 to 2031, making them the fastest-growing indication in the GCC swollen knee treatment market. This growth is fueled by investments in youth sports, organized athletic participation, and treatments for ligament injuries and training-related swelling. The UAE data highlights a male-skewed burden of knee osteoarthritis, linked to the active expatriate workforce. The demand is shifting towards active patients seeking structured recovery, reflecting a transformation in care episodes and patient expectations.

Complete Report Scope:

- By Treatment Type

- Pharmacological Treatment

- Non-Pharmacological Treatment

- Minimally Invasive Procedures

- Surgical Treatment

- By Cause or Clinical Indication

- Osteoarthritis

- Sports Injury

- Rheumatoid Arthritis and Other Inflammatory Arthritis

- Bursitis and Tendinitis

- Post-Traumatic Swelling

- Others

- By Route of Administration

- Oral

- Topical

- Injectable

- Procedural and Device-Based

- By End User

- Hospitals

- Orthopedic and Sports Medicine Clinics

- Ambulatory Surgical Centers

- Physiotherapy and Rehabilitation Centers

- Home Care Settings

- By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of GCC

List of Companies Covered in this Report:

- Abbvie

- Anika Therapeutics

- Arthrex

- B. Braun

- Bayer

- Bioventus Inc.

- Enovis Corporation

- Ferring Pharmaceuticals

- Haleon plc

- Hikma Pharmaceuticals

- IBSA Institut Biochimique SA

- Johnson & Johnson

- Medtronic

- Novartis

- Pfizer

- Sanofi

- Smiths Group

- Stryker

- Teva Pharmaceutical Industries

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Knee Osteoarthritis Burden Across GCC Countries

- 4.2.2 Growth in Obesity and Diabetes Linked To Joint Inflammation

- 4.2.3 Expansion of Private Orthopedic and Sports Medicine Clinics

- 4.2.4 Wider Adoption of Minimally Invasive Injection Therapies

- 4.2.5 Stronger Health Insurance Penetration for Specialist Care

- 4.2.6 Digital Triage and Tele-Rehabilitation Supporting Follow-Up Care

- 4.3 Market Restraints

- 4.3.1 Limited Local Clinical Standardization for Swollen Knee Pathways

- 4.3.2 High Out-of-Pocket Cost For Repeated Injection-Based Care

- 4.3.3 Dependence on Imported Orthopedic and Injectable Products

- 4.3.4 Patient Preference for Conservative Self-Medication Before Specialist Visit

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Treatment Type

- 5.1.1 Pharmacological Treatment

- 5.1.2 Non-Pharmacological Treatment

- 5.1.3 Minimally Invasive Procedures

- 5.1.4 Surgical Treatment

- 5.2 By Cause or Clinical Indication

- 5.2.1 Osteoarthritis

- 5.2.2 Sports Injury

- 5.2.3 Rheumatoid Arthritis and Other Inflammatory Arthritis

- 5.2.4 Bursitis and Tendinitis

- 5.2.5 Post-Traumatic Swelling

- 5.2.6 Others

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Topical

- 5.3.3 Injectable

- 5.3.4 Procedural and Device-Based

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Orthopedic and Sports Medicine Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Physiotherapy and Rehabilitation Centers

- 5.4.5 Home Care Settings

- 5.5 By Country

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Oman

- 5.5.6 Bahrain

- 5.5.7 Rest of GCC

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Anika Therapeutics, Inc.

- 6.3.3 Arthrex, Inc.

- 6.3.4 B. Braun SE

- 6.3.5 Bayer AG

- 6.3.6 Bioventus Inc.

- 6.3.7 Enovis Corporation

- 6.3.8 Ferring B.V.

- 6.3.9 Haleon plc

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 IBSA Institut Biochimique SA

- 6.3.12 Johnson and Johnson

- 6.3.13 Medtronic plc

- 6.3.14 Novartis AG

- 6.3.15 Pfizer Inc.

- 6.3.16 Sanofi S.A.

- 6.3.17 Smith and Nephew plc

- 6.3.18 Stryker Corporation

- 6.3.19 Teva Pharmaceutical Industries Limited

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment