PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072744

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072744

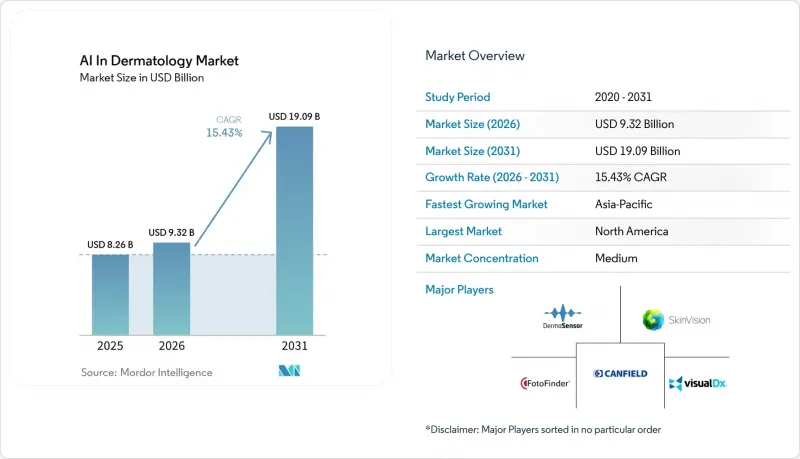

AI In Dermatology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the AI in dermatology market is expected to increase from USD 8.26 billion in 2025 to USD 9.32 billion in 2026 and is forecasted to reach USD 19.09 billion by 2031, advancing at a CAGR of 15.43% over 2026-2031.

This report is Segmented by Product Type (AI Diagnostic Software, and Others), Deployment Mode (Cloud-Based, On-Premise, and Edge/Device-Based), Condition (Skin Cancer, and Others), End-User (Hospitals, Dermatology Clinics, Academic Institutes, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD)

Global AI In Dermatology Market Trends and Insights

Increasing Accuracy of Deep-Learning Skin-Lesion Classifiers

The AI in dermatology market is gaining momentum because classifier performance has moved close to specialist-level results in real clinical settings. A prospective multicenter study across 8 German university hospitals found that the ADAE ensemble reached balanced accuracy of 0.798 versus 0.781 for dermatologists, while sensitivity reached 0.922 versus 0.734, with especially strong performance in lentigo maligna and superficial spreading melanoma. That improvement matters because it changes procurement discussions from whether the software works to how it should be calibrated in practice. The tradeoff is that higher sensitivity can reduce specificity, which means over-referral risk increases unless thresholds are adjusted for local patient profiles. In UK teledermatology deployment, Skin Analytics' DERM was estimated to save GBP 156,063.79 and 259 specialist hours per 1,000 patients versus standard care, which gives the AI in dermatology market a clearer economic argument when calibration is managed carefully.

Accelerating Dermatology Image-Database Partnerships Between Hospitals And AI Vendors

The AI in dermatology market is also being shaped by hospital data partnerships that strengthen model quality and make replacement more difficult once systems are embedded. PathAI announced a strategic collaboration with Northwestern Medicine in June 2025 to deploy the AISight digital pathology platform and co-develop new AI diagnostics, tying image management and workflow integration directly to clinical operations. In Japan, the National Skin Disease Database led under the Japanese Dermatological Association supported domestic model development and enabled skin tumor detection accuracy above 90%, creating a national training asset that is difficult for outside vendors to replicate quickly. These partnerships matter because they reduce institution-specific performance swings that appeared in earlier validation work. As a result, the AI in dermatology market is building entry barriers through data access, workflow integration, and switching costs before application features become more standardized.

Dataset Bias Causing Reduced Accuracy on Darker Skin Tones

The AI in dermatology market faces a major limit because training data still underrepresent darker skin tones in a way that affects both equity and commercial reach. ICCS 2025 research found only 10 images of Fitzpatrick skin type V and 1 image of type VI across major dermatological training datasets, which is far from global demographic reality. A 2025 study in npj Digital Medicine further showed that missing skin-tone labels inside large datasets is a direct cause of performance gaps, and it found that synthetic augmentation cannot replace authentic image diversity in high-stakes diagnosis. This matters commercially because the AI in dermatology market cannot scale evenly across South Asia, sub-Saharan Africa, Latin America, and diverse populations in North America and Europe if approvals or labels are narrowed by performance concerns. Vendors that build broader community-based datasets early are therefore likely to hold both a regulatory and a commercial advantage as the AI in dermatology market expands.

Other drivers and restraints analyzed in the detailed report include:

- Payers Piloting AI-Triage Reimbursement Codes in the United States and Europe

- Rise of Multimodal Models Integrating Dermoscopy, Genomics, and EHR Data

- Fragmented Global Regulatory Guidance for Adaptive Algorithms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AI diagnostic software held 44.36% of AI in dermatology market share in 2025, which made it the largest product category by revenue. That lead reflects the cost profile of software-only SaMD offerings and their ability to fit into existing clinical systems without hardware procurement. The AI in dermatology market still gives software an operational advantage because implementation can move through IT and workflow budgets instead of capital equipment cycles. This position also benefits from faster regulatory pathways relative to hardware-embedded alternatives in many deployment settings.

AI-integrated imaging devices are projected to grow at a 17.43% CAGR through 2031, making them the fastest-rising product segment in the AI in dermatology market. DermaSensor reported 96% sensitivity for melanoma, basal cell carcinoma, and squamous cell carcinoma in a validation study of 1,005 patients across 22 primary care sites, and the company said the device cut physicians' missed skin cancer referrals by 50%. That kind of handheld performance matters because it narrows the gap between primary care and specialist review at the point of care. The AI in dermatology industry is therefore seeing software remain the revenue core while device growth rises faster where immediate imaging feedback, triage, and non-specialist use are becoming more valuable.

Cloud-based deployment accounted for 51.73% of the AI in dermatology market size in 2025, which keeps it as the leading deployment architecture. Large hospital networks favor this approach because centralized model management, easier software updates, and scalable computing fit enterprise procurement patterns. The AI in dermatology market still leans toward cloud systems where data governance permits it, especially in organizations that want one managed environment across many facilities. That position is strengthened by the fact that cloud tools are easier to update as evidence, algorithms, and compliance needs evolve.

Edge or device-based deployment is expected to grow at a 17.63% CAGR through 2031, the fastest rate in this segmentation of the AI in dermatology market. This growth is tied to use cases where latency is a clinical issue or where data sovereignty rules make full cloud transfer less practical. The AI in dermatology market is also opening up in rural, remote, and resource-limited settings because offline-capable tools can keep working without stable bandwidth. The likely direction is a hybrid model, with centralized cloud training and local inference at the point of care, because that structure fits both performance and privacy needs.

Complete Report Scope:

- By Product Type

- AI Diagnostic Software

- AI-Integrated Imaging Devices

- Clinical Decision-Support Platforms

- Virtual Care and Tele-Dermatology Platforms

- By Deployment Mode

- Cloud-Based

- On-Premise

- Edge / Device-Based

- By Dermatology Condition

- Skin Cancer

- Psoriasis

- Acne

- Atopic Dermatitis

- Other Conditions

- By End-User

- Hospitals

- Dermatology Clinics

- Academic and Research Institutes

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 49.81% of AI in dermatology market share in 2025, which made it the largest regional contributor. The AI in dermatology market in this region benefits from a mature reimbursement environment, clearer clinical procurement pathways, and stronger early adoption across hospital networks. The United States remains the anchor because regulatory precedent, specialist demand, and private-sector buying capacity all support faster commercialization. DermaSensor's January 2025 FDA authorization for objective melanoma, basal cell carcinoma, and squamous cell carcinoma risk assessment in primary care strengthened the practical case for non-specialist use of the AI in dermatology market in the United States.

Europe is moving forward on two tracks inside the AI in dermatology market. Northern and Western Europe are advancing faster because public health systems, digital referral models, and clinical evidence programs support structured deployment. NICE conditionally recommended Skin Analytics' DERM for autonomous use in the NHS urgent suspected skin cancer pathway, which gives the AI in dermatology market in England a visible benchmark for other vendor. In Germany, DKFZ reported in 2024 that explainable AI combining predictions with visual and textual dermoscopic justification improved dermatologist accuracy and reduced cognitive fatigue, supporting a more evidence-based case for explainability-first positioning. The AI in dermatology market in Europe also faces heavier compliance work because the EU AI Act and MDR or IVDR must be managed together, which can slow smaller vendors more than larger ones.

Asia-Pacific is projected to grow at an 18.43% CAGR through 2031, making it the fastest-growing regional segment in the AI in dermatology market. The main reason is structural demand, since dermatologist shortages and broader digital health programs create stronger incentives for scaled AI triage. Japan provides one of the clearest institutional examples in the AI in dermatology market, with the National Skin Disease Database helping domestic researchers build models that exceeded 90% accuracy in skin tumor detection. The AI in dermatology market in China, India, and South Korea is also supported by government-backed digital health mandates that make remote triage more practical at large population scale. The Middle East and Africa and South America remain earlier-stage regions, where smartphone-enabled apps and teledermatology platforms are moving ahead of hospital-grade deployments, but the AI in dermatology market still has meaningful longer-term room to expand in those settings as evidence and reimbursement mature.

- AIBerry Derm

- Canfield Scientific

- DeepSkin

- DermaSensor

- DermTech

- Diagnoskin

- FotoFinder Systems

- Heidelberg Engineering

- IBM

- Legit.Health

- Lunit

- MedX Health

- MetaOptima (MoleScope)

- PROscia

- Quantificare

- Skin Analytics

- SkinIO

- SkinVision

- VisualDx

- VUNO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Accuracy of Deep-Learning Skin-Lesion Classifiers

- 4.2.2 Accelerating Dermatology Image-Database Partnerships Between Hospitals and AI Vendors

- 4.2.3 Smartphone Penetration Enabling Direct-to-Consumer Skin-Health Apps

- 4.2.4 Payers Piloting AI-Triage Reimbursement Codes in the United States and Europe

- 4.2.5 FDA Fast-Track Pathways for Software-as-a-Medical-Device (SAMD)

- 4.2.6 Rise of Multimodal Models Integrating Dermoscopy, Genomics, and EHR Data

- 4.3 Market Restraints

- 4.3.1 Dataset Bias Causing Reduced Accuracy on Darker Skin Tones

- 4.3.2 Fragmented Global Regulatory Guidance for Adaptive Algorithms

- 4.3.3 Limited Clinician Trust in AI Black-Box Decisions

- 4.3.4 High Liability Risk for Misdiagnosis in Direct-to-Consumer Apps

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 AI Diagnostic Software

- 5.1.2 AI-Integrated Imaging Devices

- 5.1.3 Clinical Decision-Support Platforms

- 5.1.4 Virtual Care and Tele-Dermatology Platforms

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Edge / Device-Based

- 5.3 By Dermatology Condition

- 5.3.1 Skin Cancer

- 5.3.2 Psoriasis

- 5.3.3 Acne

- 5.3.4 Atopic Dermatitis

- 5.3.5 Other Conditions

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Dermatology Clinics

- 5.4.3 Academic and Research Institutes

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 AIBerry Derm

- 6.3.2 Canfield Scientific

- 6.3.3 DeepSkin

- 6.3.4 DermaSensor

- 6.3.5 DermTech

- 6.3.6 Diagnoskin

- 6.3.7 FotoFinder Systems

- 6.3.8 Heidelberg Engineering

- 6.3.9 IBM

- 6.3.10 Legit.Health

- 6.3.11 Lunit

- 6.3.12 MedX Health

- 6.3.13 MetaOptima (MoleScope)

- 6.3.14 PROscia

- 6.3.15 Quantificare

- 6.3.16 Skin Analytics

- 6.3.17 SkinIO

- 6.3.18 SkinVision

- 6.3.19 VisualDx

- 6.3.20 VUNO

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment