PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072749

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072749

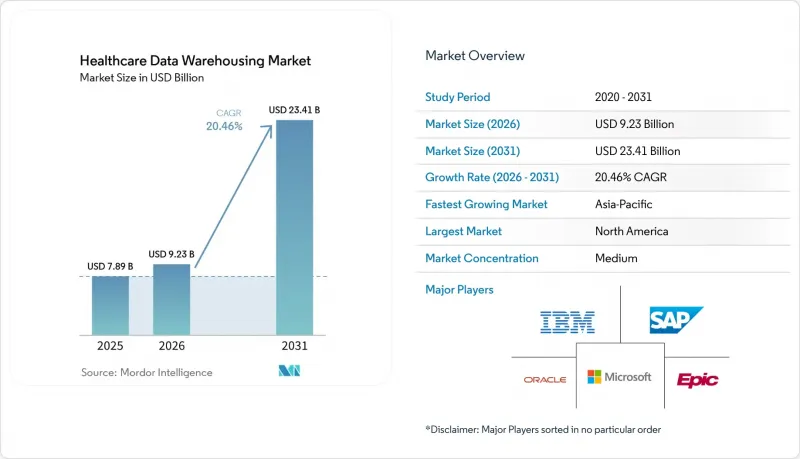

Healthcare Data Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the healthcare data warehousing market is expected to increase from USD 7.89 billion in 2025 to USD 9.23 billion in 2026 and reach USD 23.41 billion by 2031, growing at a CAGR of 20.46% over 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Deployment Mode (On-Premise, Cloud-Based, and Hybrid), Application (Financial Data Warehousing, Clinical Data Warehousing, and Others), End-User (Healthcare Providers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Data Warehousing Market Trends and Insights

Growing Regulatory Mandates for Healthcare Interoperability

The healthcare data warehousing market is seeing direct support from interoperability rules that now carry firm implementation expectations. CMS-0057-F requires impacted payers to support Prior Authorization, Provider Access, and Payer-to-Payer APIs, and those interfaces depend on persistent patient data stores that can be queried in standardized ways.This changes the spending logic for both payers and providers because data warehousing is no longer treated as a back-office improvement that can be deferred. Organizations that only meet the surface API requirement can satisfy the rule in narrow terms, but those taking a longer view are using the same investment to support analytics, population health, and AI development from the same repository. ONC's standards bulletin for 2026 broadens the structured data set for certified health IT products, which expands the amount of clinical, administrative, and related data that must be ingested and stored in a reliable form. That combination gives the healthcare data warehousing market a regulatory floor for investment that is less tied to normal budget timing and more tied to compliance exposure.

Accelerating Shift Toward Value-Based Reimbursement Models

The healthcare data warehousing market is also being shaped by reimbursement models that depend on ongoing measurement of quality, utilization, and outcomes. CMS value-based programs require providers to track performance against benchmark populations, and that work depends on combining claims, clinical, and operational data at a level that standard EHR reporting tools do not consistently support. The 2025 finalized MIPS Value Pathways guide keeps the 75% data completeness threshold in place through at least the 2028 performance period, which increases the need for data environments that can aggregate and validate multi-source records on a continuous basis. In practice, this means providers in accountable care, bundled payment, and similar programs need warehouse-backed score tracking rather than periodic manual reporting. The effect is cumulative because poor measurement in one contract period can affect future payment performance and create stronger pressure to improve attribution, stratification, and reporting workflows. As a result, the healthcare data warehousing market is increasingly tied to payment reform as much as to pure IT modernization.

High Upfront and Maintenance Costs of Large-Scale DW Infrastructure

The healthcare data warehousing market still faces a major drag from the cost of building and maintaining large-scale data environments across fragmented clinical systems. Organizations rarely start from a clean architecture because EHR platforms, laboratory systems, imaging archives, and payer records often sit in separate systems with different update cycles and inconsistent interfaces. Research published in Frontiers in Digital Health identifies legacy system integration as a central challenge in healthcare data warehouse programs because middleware, API management, and governance tooling all add continuing expense rather than one-time expense. Migration to cloud-native models can reduce some long-run complexity, but the transition itself often requires pipeline redesign, source mapping, and validation work that many organizations must fund before benefits appear. The budget strain becomes sharper when cybersecurity, regulatory compliance, and analytics modernization are financed from the same pool. The healthcare data warehousing market therefore continues to see slower adoption among buyers that recognize the strategic value of warehousing but struggle to absorb the full cost of integration and maintenance.

Other drivers and restraints analyzed in the detailed report include:

- Exponential Growth of Multimodal Healthcare Big Data

- Rapid Adoption of Cloud-Native Data Warehouse Platforms

- Shortage of Skilled Health Data Engineers and Informaticists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment held 52.64% of the healthcare data warehousing market share in 2025, which reflected buyer preference for integrated platforms that combine ETL tools, clinical data models, governance functions, and analytics in one environment. This lead was reinforced by enterprise buyers that wanted fewer integration gaps and faster deployment across multi-facility health systems. In the healthcare data warehousing industry, software platforms also gained ground because they reduced the need to assemble separate tools for ingestion, modeling, and reporting. Large providers and payers favored platforms that could support both compliance reporting and broader analytics from the same data foundation.

That position did not remove the need for hardware, but it did narrow hardware demand to more selective use cases. Local infrastructure remains relevant in government health agencies, academic medical centers, and other settings where control over compute and storage stays a top requirement. The services segment is expected to grow at the fastest pace, with 22.70% CAGR through 2031, as health systems convert large one-time implementation projects into recurring managed service relationships. Those agreements are attractive because they cover deployment support, HIPAA-oriented maintenance, training, and workflow alignment while reducing the pressure to build large internal engineering teams. This pattern shows the healthcare data warehousing market shifting from product ownership alone toward operating models that bundle technology and ongoing execution.

Cloud-based deployment held 50.33% of the healthcare data warehousing market in 2025, making it the leading deployment model as providers and payers sought more scalable infrastructure. The main appeal of cloud deployment was not only lower hardware dependence, but also easier access to elastic compute for AI, analytics, and high-volume data processing. For the healthcare data warehousing industry, cloud environments also simplified expansion across distributed organizations that needed a common platform for claims, clinical, and administrative records. This has kept cloud adoption closely tied to enterprise modernization programs rather than isolated infrastructure refresh cycles.

Hybrid deployment is anticipated to expand at the fastest pace, with a 23.57% CAGR through 2031, because many organizations still need a mixed model for governance and performance reasons. Sensitive protected health information often remains in certified local or private environments, while compute-heavy analytics and model workloads move to cloud clusters. This architecture is especially relevant in jurisdictions with stronger data residency expectations and in research-heavy institutions managing large imaging and genomics workloads.

Complete Report Scope:

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

- By Application

- Financial Data Warehousing

- Clinical Data Warehousing

- Operational and Administrative Data Warehousing

- Research and Population Health Data Warehousing

- By End-User

- Healthcare Providers

- Healthcare Payers

- Government and Public Health Agencies

- Research and Academic Institutions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 45.87% of the global healthcare data warehousing market in 2025, which made it the clear regional leader. The United States anchors this position through its dense base of large health systems, high EHR penetration, and strong regulatory pressure around interoperability and data access. Canada and Mexico remain smaller contributors, but both are expanding as national and regional digital health strategies move forward. The healthcare data warehousing market in North America also benefits from deeper vendor presence, stronger cloud adoption, and a larger installed base of enterprise analytics programs. Europe ranked second, with Germany, the United Kingdom, and France leading demand as providers and payers balance modernization goals with GDPR-driven controls on data residency and sharing.

Asia-Pacific is the fastest-growing region and is projected to expand at a 24.39% CAGR through 2031, giving it the strongest growth profile in the healthcare data warehousing market size. India's Ayushman Bharat Digital Mission is building a national health data layer that supports interoperability across public and private providers, which creates structural need for population-scale data repositories. China's hospital grading digitization standards are also supporting demand because hospitals need stronger data platforms to meet compliance, workflow, and reporting expectations. Japan adds a different growth path through federated and privacy-aware analytics models that help institutions collaborate on AI and research without fully centralizing sensitive records.

The Middle East and Africa and South America remain smaller in total size, but they present distinct openings within the healthcare data warehousing market. In the GCC, national AI programs and sovereign data strategies are supporting larger enterprise warehouse projects, particularly in the United Arab Emirates and Saudi Arabia. Oracle, Cleveland Clinic, and G42 announced a strategic partnership in May 2025 to build an AI-based global healthcare delivery platform for the United States and the UAE, which highlights the role of sovereign and cross-border infrastructure in this region. In South America, Brazil and Argentina remain the main demand centers, with public budget limits slowing some projects while private network digitization continues to support new warehouse adoption.

- Allscripts

- Amazon Web Services Inc.

- Atos SE

- Cloudera Inc.

- Dell Technologies

- Epic Systems

- GE Healthcare

- Health Catalyst

- IBM

- Intersystems

- Koninklijke Philips

- Mckesson

- Microsoft

- Optum

- Oracle

- SAP

- SAS Institute

- Siemens Healthineers

- Snowflake Inc.

- Teradata Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Regulatory Mandates for Healthcare Interoperability

- 4.2.2 Accelerating Shift Toward Value-Based Reimbursement Models

- 4.2.3 Exponential Growth of Multimodal Healthcare Big Data

- 4.2.4 Rapid Adoption of Cloud-Native Data Warehouse Platforms

- 4.2.5 Integration of SDoH and Patient-Generated Data into Analytics

- 4.2.6 Early Investments in Privacy-Preserving Analytics Frameworks

- 4.3 Market Restraints

- 4.3.1 High Upfront and Maintenance Costs of Large-Scale DW Infra

- 4.3.2 Shortage of Skilled Health Data Engineers and Informaticists

- 4.3.3 Data Quality Issues from Legacy Clinical Systems

- 4.3.4 Rising Cyber-Security Insurance Premiums Squeezing Budgets

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Financial Data Warehousing

- 5.3.2 Clinical Data Warehousing

- 5.3.3 Operational and Administrative Data Warehousing

- 5.3.4 Research and Population Health Data Warehousing

- 5.4 By End-User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.4.3 Government and Public Health Agencies

- 5.4.4 Research and Academic Institutions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Allscripts Healthcare Solutions

- 6.3.2 Amazon Web Services Inc.

- 6.3.3 Atos SE

- 6.3.4 Cloudera Inc.

- 6.3.5 Dell Technologies

- 6.3.6 Epic Systems Corporation

- 6.3.7 GE Healthcare

- 6.3.8 Health Catalyst

- 6.3.9 IBM

- 6.3.10 InterSystems Corporation

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 McKesson Corporation

- 6.3.13 Microsoft Corporation

- 6.3.14 Optum Inc.

- 6.3.15 Oracle

- 6.3.16 SAP SE

- 6.3.17 SAS Institute Inc.

- 6.3.18 Siemens Healthineers

- 6.3.19 Snowflake Inc.

- 6.3.20 Teradata Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment