PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072753

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072753

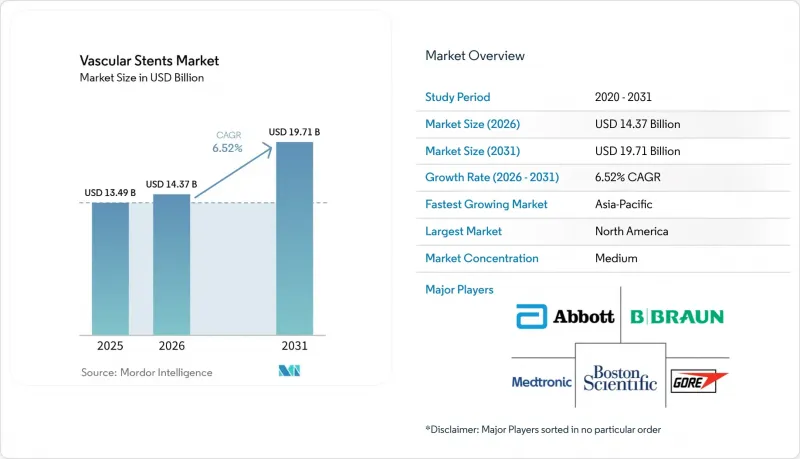

Vascular Stents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vascular stents market size is projected to expand from USD 13.49 billion in 2025 and USD 14.37 billion in 2026 to USD 19.71 billion by 2031, registering a CAGR of 6.52% between 2026 to 2031.

This report is Segmented by Product Type (Coronary Stents [Drug-Eluting Coronary Stents and More, and More), Technology (Drug-Eluting Stents, Covered Stents, and More), Material (Metallic, Polymeric), Mode of Delivery (Balloon-Expandable, Self-Expanding), End User (Hospitals, Cardiac Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts are Provided in Value (USD).

Global Vascular Stents Market Trends and Insights

Rising Coronary and Peripheral Artery Disease Burden

The vascular stents market continues to draw strength from the global rise in ischemic heart disease, which reached 31.9 million new cases in 2021 and is projected to climb to 56.4 million annual cases by 2046. This pattern keeps the vascular stents market tied to long-term disease progression, because treatment demand remains linked to aging populations and widening metabolic risk exposure instead of short-term procedure cycles. The burden is also widening across lower and middle Socio-Demographic Index regions, where high fasting plasma glucose is becoming a stronger contributor to atherosclerotic disease and is changing which devices are purchased first. In those settings, the vascular stents market is not moving through the same premium platform curve seen in higher income economies, because cost-sensitive acute care still favors simpler device choices in many cases. Peripheral artery disease is adding a separate patient pool for the vascular stents market, which means demand is not dependent only on coronary referrals or established PCI pathways.

Expanding Minimally Invasive Intervention Volumes

The vascular stents market is also benefiting from a steady shift toward minimally invasive treatment settings, as outpatient and ambulatory models are receiving broader procedural support. A Medicare analysis presented at SCAI 2025 projected a 21% increase in PCI volume in ambulatory surgical centers over the next decade, which supports longer-term placement demand for devices designed around faster workflows and predictable outcomes. This site-of-care shift matters for the vascular stents market because physician-led procurement often moves faster when platform performance is clear and formulary layers are lighter. The same trend also raises the value of systems that shorten procedure time and reduce repeat intervention risk, which keeps premium device adoption linked to operational efficiency as much as to clinical differentiation.

Device Thrombosis, Restenosis, and Reintervention Risk

The vascular stents market still faces a clear device-level limitation, because late scaffold thrombosis and restenosis remain unresolved in several use cases and still influence physician confidence. Pooled 5-year ABSORB data published in 2025 showed higher adverse event rates for bioresorbable vascular scaffolds than for metallic drug-eluting stents during years 1 through 3, which explains why broad uptake was delayed after early enthusiasm. This issue matters beyond product reputation, because the vascular stents market depends on durable outcome data when new scaffolds seek broader reimbursement and guideline support. The problem is not limited to coronary use, since peripheral lesions also carry high reintervention exposure and keep repeat care costs elevated over the patient pathway. That creates a difficult balance for the vascular stents market, where repeat interventions can support short-term device revenue but can also weaken long-term outcome credibility and invite tighter scrutiny from regulators and payers.

Other drivers and restraints analyzed in the detailed report include:

- Faster Adoption of Drug-Eluting and Covered Stent Platforms

- Imaging-Guided Precision Implantation and Complex Lesion Planning

- Reimbursement Constraints in Price-Sensitive Care Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coronary stents held 56.31% of vascular stents market share in 2025, which kept them as the core revenue segment across the vascular stents market. Drug-eluting coronary platforms remained the procedural base in developed systems because they combine long clinical experience with payer familiarity and broad physician acceptance. The product mix also reflects how the vascular stents market still depends heavily on PCI as the dominant global revascularization route, especially in systems that already have mature catheterization capacity. Coronary use has therefore stayed commercially central even while newer device classes have gained attention in more specialized settings. The same base gives large manufacturers a stable platform for launching incremental upgrades, because coronary accounts usually support training, inventory depth, and evidence generation at scale.

Peripheral stents, carotid systems, and neurovascular devices broaden the vascular stents market beyond coronary disease, but their commercial profiles remain more fragmented and more dependent on indication-specific data. The vascular stents industry also shows wider variability across these categories, since vessel anatomy, stroke protection needs, and reimbursement rules differ more than they do in coronary care. Neurovascular stents keep a technically differentiated role because pipeline embolization and intracranial applications command specialist use and often benefit from dedicated reimbursement pathways. EVAR stent grafts are the fastest-growing product category, and vascular stents market size for this segment is projected to expand at a 9.38% CAGR through 2031 as abdominal and thoracoabdominal aortic repair volumes rise. The 2026 ESVS guideline shift toward fenestrated and branched repair as the preferred treatment for thoracoabdominal aneurysms expands the addressable pool for the vascular stents market beyond standard infrarenal anatomy and brings more complex cases into endovascular pathways.

Covered stents accounted for 38.24% of the market in 2025, which made them the largest technology segment within the vascular stents market. Their role is broader than aneurysm exclusion alone, because they also support peripheral and aortic repair in lesions where vessel sealing and structural durability matter as much as lumen patency. Drug-eluting stents remained the core value driver in coronary care, where second-generation thin-strut platforms and biodegradable polymer coatings improved the balance between radial support and vessel healing. Bare-metal platforms retained a narrower role in emergency use and in settings where dual antiplatelet adherence remains uncertain, which shows that technology replacement across the vascular stents market is still incomplete. This uneven transition keeps older and newer technologies commercially relevant at the same time, especially across mixed reimbursement environments.

Bioabsorbable stents are forecast to grow at 8.52% CAGR from 2026 to 2031, and vascular stents market size in this technology band is moving faster than any other technology segment. Abbott's Esprit BTK, Biotronik's Freesolve program, and MicroPort's Firesorb all show how the vascular stents market is building a new scaffold pipeline around improved degradation profiles, longer lesion usability, and lower repeat procedure expectations. The vascular stents industry is not seeing immediate displacement of metallic DES, because long-term evidence and commercialization timelines still favor established platforms in the largest coronary accounts. A 2025 systematic review in Biomedicines reported clinically equivalent 12-month outcomes between biodegradable polymer DES and polymer-free DES, which is already narrowing the premium attached to durable-polymer systems and pressuring pricing within this subsegment. The technology path in the vascular stents market therefore points to coexistence, with evidence-backed incumbent platforms retaining scale while scaffold-based systems expand first in targeted lesions and patient groups.

Complete Report Scope:

- By Product Type

- Coronary Stents

- Drug-Eluting Coronary Stents

- Bare-Metal Coronary Stents

- Covered Coronary Stents

- Bioabsorbable Coronary Stents

- Peripheral Stents

- Carotid Artery Stents

- Femoral Artery Stents

- Iliac Artery Stents

- Renal Artery Stents

- Other Peripheral Stents

- EVAR Stent Grafts

- Abdominal Aortic Aneurysm Stent Grafts

- Thoracic Aortic Aneurysm Stent Grafts

- Neurovascular Stents

- Flow-Diverter Stents

- Intracranial Atherosclerotic Stents

- Coronary Stents

- By Technology

- Drug-Eluting Stents

- Covered Stents

- Bare-Metal Stents

- Bioabsorbable Stents

- By Material

- Metallic Materials

- Cobalt Chromium

- Platinum Chromium

- Nickel Titanium

- Stainless Steel

- Polymeric Materials

- Biodegradable Polymers

- Non-Biodegradable Polymers

- Metallic Materials

- By Mode of Delivery

- Balloon-Expandable Stents

- Self-Expanding Stents

- By End User

- Hospitals

- Cardiac Centers

- Ambulatory Surgical Centers

- Cath Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 41.22% of vascular stents market share in 2025, which kept it as the largest regional contributor to the vascular stents market. Its position rests on mature reimbursement systems, high interventional volumes, and broad physician access to advanced imaging and device options. The 2025 ACC, AHA, and SCAI guideline update is supporting more imaging-guided complex stenting, which can lift device value per case even when regional procedure growth is moderate. The United States therefore remains the main premium platform market, especially for advanced coronary and below-the-knee technologies that need both evidence and payment support. Canada also supports the vascular stents market through adoption pathways for newer dissolvable scaffolds, as seen in the September 2025 authorization for Abbott's Esprit BTK.

Europe remains an important stabilizing region for the vascular stents market because of its large procedure base and strong specialty center infrastructure. Germany is a key example, with a large coronary disease burden and a high volume of hospital admissions that keep cardiovascular intervention demand structurally relevant. The ESVS 2026 guideline is also expanding support for fenestrated and branched endovascular repair, which benefits device makers active in complex aortic treatment. At the same time, MDR compliance is narrowing European portfolios toward suppliers with established regulatory depth, which favors larger companies with already certified platforms. This keeps the vascular stents market in Europe more selective, with fewer commercialization shortcuts and a stronger premium on clinical follow-up data.

Asia-Pacific is the fastest-growing region, and vascular stents market size in the region is forecast to advance at an 8.85% CAGR through 2031. China remains central to that growth because its centralized procurement system now operates at very large scale, with the second 2026 coronary stent round covering 2.73 million units across 4,468 institutions. This means the vascular stents market in Asia-Pacific combines strong demand expansion with intense price discipline, which creates a different growth model than the one seen in North America. India adds another layer through a mix of price-sensitive public accounts and a growing private hospital base, which keeps room open for both multinational and local DES suppliers. The Middle East and Africa and South America remain smaller in absolute value, but they continue to gain relevance as training capacity, catheterization infrastructure, and cost-competitive imports expand access to intervention across more health systems.

- Abbott Laboratories

- Artivion, Inc.

- B. Braun

- Beckton Dickinson

- Biosensors International Group, Ltd.

- BIOTRONIK

- Boston Scientific

- Cook Group

- Cordis

- Endologix LLC

- Lepu Medical Technology (Beijing) Co., Ltd.

- LifeTech Scientific Corporation

- Medtronic

- Meril Life Science

- MicroPort

- Sahajanand Medical Technologies

- Stryker

- Terumo

- Translumina

- W. L. Gore and Associates, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Coronary and Peripheral Artery Disease Burden

- 4.2.2 Expanding Minimally Invasive Intervention Volumes

- 4.2.3 Faster Adoption of Drug-Eluting and Covered Stent Platforms

- 4.2.4 Aging Population and Higher Reintervention Demand

- 4.2.5 Imaging-Guided Precision Implantation and Complex Lesion Planning

- 4.2.6 Cost Pressure Shifting Purchasers Toward High-Value Stent Platforms

- 4.3 Market Restraints

- 4.3.1 Device Thrombosis, Restenosis, and Reintervention Risk

- 4.3.2 Stringent Regulatory Evidence and Post-Market Surveillance Burden

- 4.3.3 Reimbursement Constraints in Price-Sensitive Care Settings

- 4.3.4 Procedural Preference for Alternative Revascularization Approaches in Select Cases

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Coronary Stents

- 5.1.1.1 Drug-Eluting Coronary Stents

- 5.1.1.2 Bare-Metal Coronary Stents

- 5.1.1.3 Covered Coronary Stents

- 5.1.1.4 Bioabsorbable Coronary Stents

- 5.1.2 Peripheral Stents

- 5.1.2.1 Carotid Artery Stents

- 5.1.2.2 Femoral Artery Stents

- 5.1.2.3 Iliac Artery Stents

- 5.1.2.4 Renal Artery Stents

- 5.1.2.5 Other Peripheral Stents

- 5.1.3 EVAR Stent Grafts

- 5.1.3.1 Abdominal Aortic Aneurysm Stent Grafts

- 5.1.3.2 Thoracic Aortic Aneurysm Stent Grafts

- 5.1.4 Neurovascular Stents

- 5.1.4.1 Flow-Diverter Stents

- 5.1.4.2 Intracranial Atherosclerotic Stents

- 5.1.1 Coronary Stents

- 5.2 By Technology

- 5.2.1 Drug-Eluting Stents

- 5.2.2 Covered Stents

- 5.2.3 Bare-Metal Stents

- 5.2.4 Bioabsorbable Stents

- 5.3 By Material

- 5.3.1 Metallic Materials

- 5.3.1.1 Cobalt Chromium

- 5.3.1.2 Platinum Chromium

- 5.3.1.3 Nickel Titanium

- 5.3.1.4 Stainless Steel

- 5.3.2 Polymeric Materials

- 5.3.2.1 Biodegradable Polymers

- 5.3.2.2 Non-Biodegradable Polymers

- 5.3.1 Metallic Materials

- 5.4 By Mode of Delivery

- 5.4.1 Balloon-Expandable Stents

- 5.4.2 Self-Expanding Stents

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Cardiac Centers

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Cath Labs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Artivion, Inc.

- 6.3.3 B. Braun SE

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Biosensors International Group, Ltd.

- 6.3.6 Biotronik SE and Co. KG

- 6.3.7 Boston Scientific Corporation

- 6.3.8 Cook Medical LLC

- 6.3.9 Cordis Corporation

- 6.3.10 Endologix LLC

- 6.3.11 Lepu Medical Technology (Beijing) Co., Ltd.

- 6.3.12 LifeTech Scientific Corporation

- 6.3.13 Medtronic plc

- 6.3.14 Meril Life Sciences Pvt. Ltd.

- 6.3.15 MicroPort Scientific Corporation

- 6.3.16 Sahajanand Medical Technologies Limited

- 6.3.17 Stryker Corporation

- 6.3.18 Terumo Corporation

- 6.3.19 Translumina GmbH

- 6.3.20 W. L. Gore and Associates, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment