PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072755

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072755

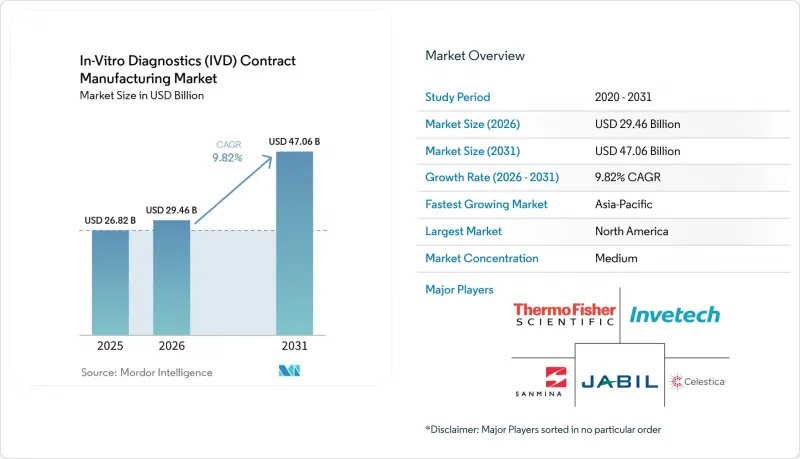

In-Vitro Diagnostics (IVD) Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the in-Vitro diagnostics (IVD) contract manufacturing market size is projected to expand from USD 26.82 billion in 2025 and USD 29.46 billion in 2026 to USD 47.06 billion by 2031, registering a CAGR of 9.82% between 2026 to 2031.

This report is Segmented by Product Type (Instruments, Reagents and More), Service Type (Manufacturing Services, Assay Development, and More), Technology (Immunoassays, Molecular Diagnostics, Clinical Chemistry, and More), End User (Medical Device/Biotech, Pharma, Hospitals/Labs, Research), and Geography (North America, Europe, Asia-Pacific, and More). Forecasts in Value (USD).

Global In-Vitro Diagnostics (IVD) Contract Manufacturing Market Trends and Insights

Rising Outsourcing of IVD Manufacturing by OEMs

The IVD contract manufacturing market is benefiting from a clear change in OEM behavior, as outsourcing is now used to transfer operating risk and compliance burden, not only to reduce cost. Diagnostic platforms now combine multiplex chemistries, microfluidic cartridges, and embedded software, which makes it harder to justify separate in-house production lines for every product variation. The IVD contract manufacturing market is therefore expanding because validated external capacity offers a practical alternative to repeated capital spending on specialized facilities. In 2026, the FDA implements the Quality Management System Regulation, which aligns 21 CFR Part 820 with ISO 13485:2016 and reinforces accountability across outsourced operations. That regulatory structure does not reduce sponsor responsibility, but it does make experienced partners more valuable because they already operate within mature quality frameworks. The IVD contract manufacturing market is gaining from this preference for fewer and more deeply integrated manufacturing relationships.

Expanding Molecular Diagnostics and Immunoassay Pipelines

The IVD contract manufacturing market is also being lifted by broader test menu expansion across immunoassay, molecular, and point-of-care formats. Roche Diagnostics disclosed a pipeline of around 130 new tests planned for launch across 2025 to 2028, which shows the scale of commercialization work that large OEMs are trying to manage without building all related manufacturing internally. The IVD contract manufacturing market benefits when OEMs choose to direct capital toward pipeline expansion and leave process scale-up, batch transfer, and production readiness to outside partners. This pattern is especially supportive for CMOs that can handle development transfer and manufacturing ramp-up within the same operating model. It shortens the path from assay design to commercial output and reduces friction between R&D teams and production teams. The IVD contract manufacturing market is therefore seeing stronger demand for partners that can absorb both scientific complexity and launch execution.

Intellectual Property Leakage Risk Across Multi-Site Partners

The IVD contract manufacturing market still faces a basic tension between scale expansion and protection of core assay know-how. Assay formulations, antibody clone identities, and reagent compositions remain central competitive assets for OEMs, and wider distribution across multiple partner sites increases exposure. The IVD contract manufacturing market is constrained because smaller innovators are often cautious about how far they extend production across a broader network, especially when workflows cross several jurisdictions. In practice, many programs respond through compartmentalized tech transfer, narrower information access, and site-specific process segregation. Those controls reduce risk, but they also add coordination time and management overhead. The IVD contract manufacturing market therefore expands more slowly in some programs than demand alone would suggest, because IP protection still shapes partner selection and network design.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Burden Favoring Specialist Contract Manufacturers

- Scaling Need for High-Mix, Low-Volume Diagnostic Production

- High Validation, Documentation, and Quality System Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and Consumables held 70.31% share of the IVD contract manufacturing market size in 2025, which kept this category as the core revenue base for outsourced diagnostics production. The IVD contract manufacturing market depends heavily on this recurring demand because reagent replenishment happens continuously across hospital laboratories, point-of-care settings, and research workflows. The reagent-lease model in clinical chemistry and immunoassay systems supports long-tail reagent volumes after instrument placement, which makes demand more predictable for manufacturing partners. Lateral flow strips, ELISA components, and monoclonal antibody-based reagent kits remain central product classes in this part of the IVD contract manufacturing market.

The smallest product category still adds strategic value because software and related services are increasingly bundled with premium manufacturing contracts instead of being sold as stand-alone add-ons. Instruments are the fastest-growing product segment, with a forecast CAGR of 12.38% over 2026-2031, and this is one of the clearest signs that the IVD contract manufacturing market is moving deeper into higher-complexity hardware work. OEMs are handing over PCB assembly, optical subsystems, and full final assembly to partners with electronics manufacturing heritage because in-house hardware lines are harder to justify for anything other than the highest-volume platforms. As next-generation systems combine microfluidics, embedded software, wireless connectivity, and tighter quality assurance needs, the IVD contract manufacturing market is seeing more value move toward CMOs that can manage complete instrument builds instead of only consumables.

Manufacturing Services captured 45.24% of the IVD contract manufacturing market size in 2025, which shows that core production work still anchors most commercial relationships. In the IVD contract manufacturing industry, this segment is often the first point of entry because OEMs begin with fill-finish, kitting, lot release, or basic production support before expanding the scope of work. The IVD contract manufacturing market continues to rely on these services across nearly every product and technology category, which makes the segment less exposed to shifts in any single platform type. Packaging, labeling, and quality support are also expanding because OEMs increasingly want one partner to absorb more downstream execution.

Assay Development Services are growing faster, with a 10.52% CAGR projected for 2026-2031, and that growth reflects a more involved relationship between development and manufacturing. The IVD contract manufacturing market is increasingly shaped by early-stage collaboration, where manufacturability is addressed before a product reaches full commercial transfer. That model is attractive because even small assay changes can lead to fresh validation work, which keeps development support relevant well after launch. The IVD contract manufacturing industry is therefore shifting away from simple build-to-print engagement and toward longer partnerships where development, validation, and production are managed as one continuous workflow.

Complete Report Scope:

- By Product Type

- Instruments

- Reagents and Consumables

- Software and Services

- By Service Type

- Manufacturing Services

- Assay Development Services

- Packaging, Labeling, and Quality and Regulatory Support Services

- By Technology

- Immunoassays

- Molecular Diagnostics

- Clinical Chemistry

- Hematology

- Microbiology

- Coagulation and Hemostasis

- By End User

- Medical Device and Biotechnology Companies

- Pharmaceutical Companies

- Hospitals and Clinical Laboratories

- Research and Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 41.22% of the IVD contract manufacturing market size in 2025, which kept it as the largest regional base for outsourced diagnostics production. The region benefits from a dense concentration of OEM headquarters, a large network of FDA-registered manufacturing sites, and stronger demand for audit-ready partners. The IVD contract manufacturing market in North America is also being lifted by the 2026 QMSR implementation, because OEMs are already favoring partners that can show stronger alignment with mature quality systems before enforcement hardens. Roche announced a USD 550 million investment in its Indianapolis diagnostics manufacturing hub in May 2025, aimed at expanding domestic diagnostics capacity and supporting supply security. That kind of investment shows why the IVD contract manufacturing market in the region remains closely tied to reshoring, regulatory readiness, and the value of domestic manufacturing depth.

Europe held the second-largest regional position in 2025, and the IVD contract manufacturing market there continues to be shaped by the IVDR transition and the need for certified capacity. Germany remained the largest national IVD base in Europe. bioMerieux broke ground on 29 May 2026 for a new EUR 250 million (USD 296.25 million) PCR test production facility in La Balme-les-Grottes, France, which is intended to strengthen European supply security for BIOFIRE syndromic panels. The IVD contract manufacturing market in Europe is therefore moving toward fewer, larger, and more compliance-ready production platforms.

Asia-Pacific is the fastest-growing region in the IVD contract manufacturing market, with a forecast CAGR of 12.65% over 2026-2031. Growth is supported by expanding hospital infrastructure, rising chronic disease burden, and policy support for local diagnostics manufacturing in countries such as China, India, and South Korea. The IVD contract manufacturing market in Asia-Pacific also benefits from the fact that OEMs want production closer to end demand in order to reduce logistics exposure and respond faster to regional procurement conditions. Middle East and Africa and South America remain smaller in absolute terms, but the IVD contract manufacturing market is still gaining ground there as regional demand builds around local supply security and targeted specialist production.

- Abbott Laboratories

- Beckton Dickinson

- Benchmark Electronics, Inc.

- bioMerieux

- Bio-Rad Laboratories

- Celestica

- Danaher

- Flex

- Gerresheimer

- Invetech

- Jabil

- Merck

- Phillips-Medisize

- Roche

- Sanmina Corporation

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Outsourcing of IVD Manufacturing by OEMs

- 4.2.2 Expanding Molecular Diagnostics and Immunoassay Pipelines

- 4.2.3 Regulatory Burden Favoring Specialist Contract Manufacturers

- 4.2.4 Scaling Need for High-Mix, Low-Volume Diagnostic Production

- 4.2.5 Rapid Localization of Supply Chains Near Demand Centers

- 4.2.6 More Frequent Platform Revalidation After Minor Assay Changes

- 4.3 Market Restraints

- 4.3.1 Intellectual Property Leakage Risk Across Multi-Site Partners

- 4.3.2 High Validation, Documentation, and Quality System Costs

- 4.3.3 Capacity Bottlenecks for Specialized Reagents and Cartridges

- 4.3.4 Supplier Qualification Complexity for Critical Inputs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Reagents and Consumables

- 5.1.3 Software and Services

- 5.2 By Service Type

- 5.2.1 Manufacturing Services

- 5.2.2 Assay Development Services

- 5.2.3 Packaging, Labeling, and Quality and Regulatory Support Services

- 5.3 By Technology

- 5.3.1 Immunoassays

- 5.3.2 Molecular Diagnostics

- 5.3.3 Clinical Chemistry

- 5.3.4 Hematology

- 5.3.5 Microbiology

- 5.3.6 Coagulation and Hemostasis

- 5.4 By End User

- 5.4.1 Medical Device and Biotechnology Companies

- 5.4.2 Pharmaceutical Companies

- 5.4.3 Hospitals and Clinical Laboratories

- 5.4.4 Research and Academic Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Benchmark Electronics, Inc.

- 6.3.4 bioMerieux SA

- 6.3.5 Bio-Rad Laboratories, Inc.

- 6.3.6 Celestica Inc.

- 6.3.7 Danaher Corporation

- 6.3.8 Flex Ltd.

- 6.3.9 Gerresheimer AG

- 6.3.10 Invetech

- 6.3.11 Jabil Inc.

- 6.3.12 Merck KGaA

- 6.3.13 Phillips-Medisize

- 6.3.14 Roche Diagnostics

- 6.3.15 Sanmina Corporation

- 6.3.16 Siemens Healthineers AG

- 6.3.17 Sysmex Corporation

- 6.3.18 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment