PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072824

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072824

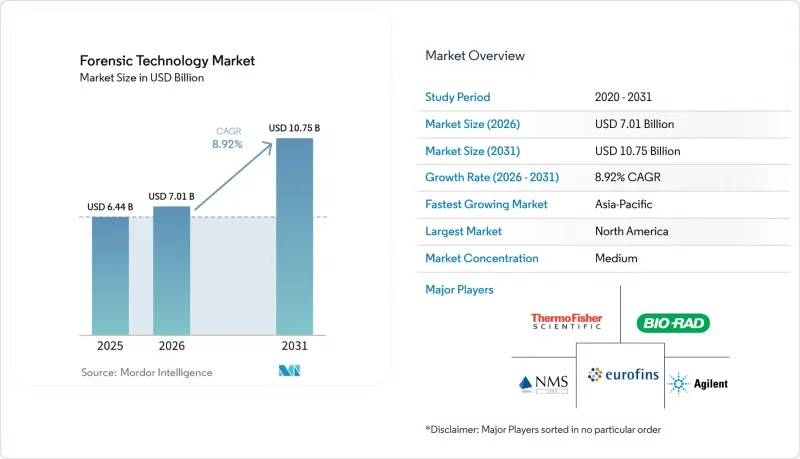

Forensic Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the forensic technology market size is expected to grow from USD 6.44 billion in 2025 to USD 7.01 billion in 2026 and is forecast to reach USD 10.75 billion by 2031 at 8.92% CAGR over 2026-2031.

This report is Segmented by Technology (PCR, Fingerprint Imaging, Facial Recognition, and More), Service (DNA Profiling, Chemical, and More), Application (Criminal, Counterterrorism, Civil, Cold Case), End User (Law Enforcement, Government Labs, Defense, Private Labs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Forensic Technology Market Trends and Insights

Rising Digital Evidence Volumes Across Mobile, Cloud, and Endpoints

Forensic technology is experiencing increased demand due to the growing volume of digital evidence. Criminal investigations now involve encrypted messaging, cloud storage, vehicle telematics, and smart-home records. Smartphone data has become the largest source of evidence requests, driving demand for specialized extraction and decryption tools over traditional IT investigation software. Cloud-based evidence introduces delays as cross-border legal steps are often required before data extraction. Vendors offering integrated extraction and legal workflow solutions are reducing wait times, enhancing their competitive position. This shift emphasizes the importance of software orchestration and secure evidence transfer in the forensic technology market.

Expansion of DNA Databases and Rapid DNA Workflows

Changes in DNA workflow policies, particularly the integration of Rapid DNA results with national search systems, are driving growth in the forensic technology market. The FBI updated its Quality Assurance Standards for Forensic Laboratories in January 2025, enabling DNA profiles from Rapid DNA analyses to be searched in the national CODIS database starting July 1, 2025. Pennsylvania State Police launched a Rapid DNA program in 2025, generating an investigative lead within 2 hours during its first week of operation. As Rapid DNA aligns with approved search pathways, demand is shifting toward consumables, software, and validated integrations, benefiting vendors like Thermo Fisher Scientific with its Applied Biosystems RapidHIT ID system.

High Cost of Advanced Instrumentation, Licensing, and Validation

Smaller jurisdictions face challenges in adopting advanced forensic technologies due to high costs. Platforms like next-generation sequencing and high-sensitivity mass spectrometers often exceed USD 500,000 per lab, making them inaccessible without grant support. Additionally, these systems require method validation, staff training, and documentation, delaying their integration into casework. Despite the Coverdell Program being authorized at USD 151 million, actual appropriations were limited to USD 120 million for fiscal years 2024 and 2025. This funding gap slows direct instrument procurement, even as outsourced casework temporarily increases.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Triage of Multimedia and Encrypted Data Repositories

- Shift Toward Interoperable, Cross-Agency Evidence Sharing Platforms

- Shortage of Skilled Examiners and Accredited Laboratory Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Digital Forensics held a 34.23% share of the forensic technology market, leading all other technology segments. This growth was driven by the increasing reliance on smartphone evidence and the shift of criminal communications to encrypted platforms requiring specialized tools. Mobile and computer forensics remain key drivers as agencies handle significantly more data per device. Platforms integrating extraction, analytics, and secure collaboration continue to see strong demand.

Capillary Electrophoresis is the fastest-growing segment, with an 11.45% CAGR projected through 2031. Its relevance stems from its role in DNA profiling, the standard for individual identification in forensic genetics. Rapid DNA deployment and the central role of PCR in workflows further support its growth. While next-generation sequencing shows potential, its adoption is limited by cost and complexity. Advancements in biometric systems like fingerprint and facial recognition also highlight the market's technological diversity.

DNA Profiling accounted for 44.23% of revenue in 2025, making it the largest service in the forensic technology market. Its trusted role in criminal investigations, disaster victim identification, and civil kinship testing ensures consistent demand. Database expansion and faster workflows further strengthen its position, driving demand for instruments and software.

Biometric Analysis is the fastest-growing service, with a 12.55% CAGR projected through 2031. Growth is fueled by multimodal deployments in border control and civil identification, emphasizing unified platforms for multiple biometric checks. Chemical Analysis and Firearms Identification remain significant, especially with the rise of synthetic drugs. The market's expansion is evident in services like audio forensics and deepfake detection.

Complete Report Scope:

- By Technology

- Polymerase Chain Reaction (PCR)

- Capillary Electrophoresis

- Next Generation Sequencing (NGS)

- Rapid DNA Analysis

- Automated Liquid Handling Technology

- Microarrays

- Fingerprint Imaging and Matching

- Facial Recognition

- Iris and Palm Vein Recognition

- Voice Biometrics

- Digital Forensics

- Computer Forensics

- Mobile Device Forensics

- Others

- By Service

- DNA Profiling

- Chemical Analysis

- Biometric Analysis

- Firearms Identification

- Others

- By Application

- Criminal Investigations

- Counterterrorism and Intelligence

- Disaster Victim Identification

- Civil and Private Investigations

- Regulatory and Compliance Investigations

- Cold Case Review and Exoneration

- By End User

- Law Enforcement Agencies

- Government Forensic Laboratories

- Defense and Intelligence Organizations

- Private Forensic Laboratories

- Corporates and Law Firms

- Insurance and Fraud Investigation Firms

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America secured 40.24% of the total revenue in the forensic technology market, maintaining its leadership position. The region benefits from consistent procurement cycles from federal agencies, state crime labs, and private forensic providers, ensuring steady spending. The FBI's Quality Assurance Standards update in July 2025 enabled Rapid DNA profiles to be searched against CODIS, driving a shift from reference-lab workflows to point-of-arrest DNA processing. This transition supports demand for equipment upgrades, software integration, and consumables. North America's mature digital forensics environment prioritizes evidence extraction, multimedia analysis, and secure cloud reviews in procurement decisions.

Asia-Pacific is projected to grow at a 9.67% CAGR through 2031, making it the fastest-growing region in the forensic technology market. Growth is driven by institutional expansions rather than increased penetration of existing tools. India leads with investments in laboratory capacity, training, campus expansion, and national forensic data infrastructure. China's public-security digitization integrates forensic capabilities with surveillance and evidence management systems. South Korea is advancing biometric capabilities at borders, while Japan focuses on high-throughput DNA systems for national programs. These developments expand laboratory networks and evidence systems, driving future demand for software, maintenance, and reagents.

The Middle East and Africa, though smaller in revenue, are experiencing rising investments in smart-city, border-security, and national security programs, particularly in the GCC. The UAE and Saudi Arabia have adopted large-scale fingerprint and facial recognition systems, aligning with NIST-style interoperability standards. South Africa leads in sub-Saharan Africa with its government-backed laboratory network. In South America, Brazil and Argentina drive demand, with Brazil investing in digital forensics for financial crime and federal prosecution. Regional growth is shaped by replacement demand, policy-driven expansion, and new institutional developments.

- ADF Solutions, Inc.

- Agilent Technologies

- Bio-Rad Laboratories

- Cellebrite DI Ltd.

- Eurofins

- Exterro, Inc.

- GE HealthCare Technologies Inc.

- HORIBA

- IDEMIA Group

- Kroll, LLC

- LGC Group

- Magnet Forensics Inc.

- MSAB AB

- NMS Labs

- Nuix Limited

- OpenText

- Oxygen Forensics, Inc.

- Paraben Corporation

- Promega

- Shimadzu

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Digital Evidence Volumes Across Mobile, Cloud, and Endpoint Sources

- 4.2.2 Expansion of DNA Databases and Rapid DNA Workflows

- 4.2.3 Public-Safety Modernization and Forensic Lab Digitization Programs

- 4.2.4 Courtroom Demand for Faster, More Defensible Chain-of-Custody Workflows

- 4.2.5 AI-Assisted Triage of Multimedia and Encrypted Data Repositories

- 4.2.6 Shift Toward Interoperable, Cross-Agency Evidence Sharing Platforms

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Instrumentation, Licensing, and Validation

- 4.3.2 Shortage of Skilled Examiners and Accredited Laboratory Capacity

- 4.3.3 Privacy, Surveillance, and Evidentiary Admissibility Constraints

- 4.3.4 Fragmented Standards Across Jurisdictions and Evidence Types

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Technology

- 5.1.1 Polymerase Chain Reaction (PCR)

- 5.1.2 Capillary Electrophoresis

- 5.1.3 Next Generation Sequencing (NGS)

- 5.1.4 Rapid DNA Analysis

- 5.1.5 Automated Liquid Handling Technology

- 5.1.6 Microarrays

- 5.1.7 Fingerprint Imaging and Matching

- 5.1.8 Facial Recognition

- 5.1.9 Iris and Palm Vein Recognition

- 5.1.10 Voice Biometrics

- 5.1.11 Digital Forensics

- 5.1.12 Computer Forensics

- 5.1.13 Mobile Device Forensics

- 5.1.14 Others

- 5.2 By Service

- 5.2.1 DNA Profiling

- 5.2.2 Chemical Analysis

- 5.2.3 Biometric Analysis

- 5.2.4 Firearms Identification

- 5.2.5 Others

- 5.3 By Application

- 5.3.1 Criminal Investigations

- 5.3.2 Counterterrorism and Intelligence

- 5.3.3 Disaster Victim Identification

- 5.3.4 Civil and Private Investigations

- 5.3.5 Regulatory and Compliance Investigations

- 5.3.6 Cold Case Review and Exoneration

- 5.4 By End User

- 5.4.1 Law Enforcement Agencies

- 5.4.2 Government Forensic Laboratories

- 5.4.3 Defense and Intelligence Organizations

- 5.4.4 Private Forensic Laboratories

- 5.4.5 Corporates and Law Firms

- 5.4.6 Insurance and Fraud Investigation Firms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 ADF Solutions, Inc.

- 6.3.2 Agilent Technologies, Inc.

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 Cellebrite DI Ltd.

- 6.3.5 Eurofins Scientific SE

- 6.3.6 Exterro, Inc.

- 6.3.7 GE HealthCare Technologies Inc.

- 6.3.8 HORIBA, Ltd.

- 6.3.9 IDEMIA Group

- 6.3.10 Kroll, LLC

- 6.3.11 LGC Group

- 6.3.12 Magnet Forensics Inc.

- 6.3.13 MSAB AB

- 6.3.14 NMS Labs

- 6.3.15 Nuix Limited

- 6.3.16 OpenText Corporation

- 6.3.17 Oxygen Forensics, Inc.

- 6.3.18 Paraben Corporation

- 6.3.19 Promega Corporation

- 6.3.20 Shimadzu Corporation

- 6.3.21 Thermo Fisher Scientific Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment