PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072852

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072852

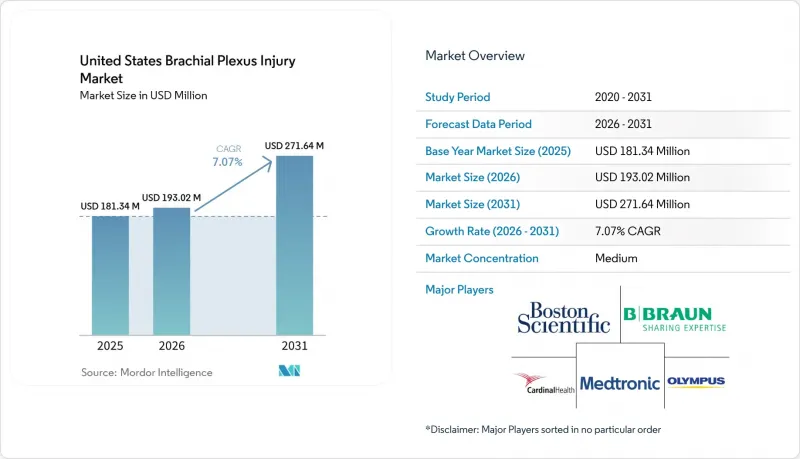

United States Brachial Plexus Injury - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states brachial plexus injury market size is expected to increase from USD 181.34 million in 2025 to USD 193.02 million in 2026 and reach USD 271.64 million by 2031, growing at a CAGR of 7.07% over 2026-2031.

This report is Segmented by Type of Injury (Avulsion, Rupture, Neuroma, Stretch), Treatment Type (Surgical Treatment, Physical Therapy, Medication, Rehabilitation), Patient Demographics (Infants, Adults, Elderly), Diagnostic Method (EMG, Ultrasound, MRI), and End User (Hospitals, Specialty Clinics, Ascs, Rehabilitation Centers). The Market Forecasts are Provided in Terms of Value (USD).

United States Brachial Plexus Injury Market Trends and Insights

Rising Traumatic Injury Burden From Road Accidents and Sports Incidents

Motorcycle accidents represented 32.8% of brachial plexus injury cases in trauma populations, and motor vehicle collisions accounted for another 16.7% of peripheral nerve injuries more broadly, which keeps a steady inflow of severe cases into the United States brachial plexus injury market. This pattern matters because road trauma produces high-force cervical root damage that is more likely to need advanced imaging, surgical triage, and long rehabilitation than lower-energy nerve injuries. The sports burden also matters, especially in younger patients, because pediatric traumatic brachial plexus injury data showed that motor vehicle accidents accounted for 35% of cases and sports incidents for 28%. Those same data showed that microsurgery was indicated in 41% of traumatic cases compared with 13% of birth injury cases, which means trauma cases generate a higher surgical conversion rate once they enter specialist care. As a result, the United States brachial plexus injury market continues to depend on trauma volume not just for patient counts, but for a disproportionate share of complex and high-value treatment episodes.

High Surgical Receptivity for Severe Root Avulsion and Complex Plexus Damage

The United States brachial plexus injury market remains highly responsive to severe cases because root avulsion and complete brachial plexus disruptions carried a 53% operative management rate, and nerve transfers were used in 48% of all brachial plexus injury surgeries. Avulsion injuries create strong procedure demand because preganglionic root loss prevents standard graft-based repair and pushes surgeons toward extraplexal donor strategies such as intercostal transfer or contralateral C7 transfer. Published clinical evidence in 2024 showed that contralateral C7 transfer is now viewed as a reliable pathway for patients with multiple root avulsions who lack intraplexal donor options, which expands the treatable population within the United States brachial plexus injury market. A 2025 meta-analysis also showed that upper trunk repairs achieved a 75% success rate, while complete injuries reached 29%, which reinforces the value of early case selection and rapid referral into specialized centers. That mix of technical feasibility and better-defined outcome expectations keeps surgery at the center of the United States brachial plexus injury market for the most disabling forms of nerve damage.

Narrow Surgical Timing Window Reduces Treatable Patient Pool

The United States brachial plexus injury market faces a hard biological limit because nerve regeneration moves at 1 mm per day, and delays beyond 3 to 6 months lower the chance of meaningful motor recovery. Early intervention matters in practical terms, since one multicenter series reported mean shoulder abduction of 110° for surgery performed within 6 months compared with 51° for delayed cases. This timing problem is especially important in the United States brachial plexus injury market because many patients first present to emergency departments or community hospitals that do not have a direct referral pathway into subspecialty nerve reconstruction. The result is not a full loss of demand, because those patients still use physical therapy and pain management, but it does remove them from the highest-value surgical funnel. That compression of eligible case volume limits how much revenue growth the United States brachial plexus injury market can realize from procedure innovation alone.

Other drivers and restraints analyzed in the detailed report include:

- Faster Adoption of AI-Assisted Imaging and Intraoperative Nerve Monitoring

- Higher Coverage for Medically Necessary Reconstructive Care and Rehabilitation

- Scarcity of Subspecialty Surgeons Slows Referral-to-Treatment Conversion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Avulsion held 34.48% of the United States brachial plexus injury market share in 2025, which reflects its close link with the high-energy trauma patterns that dominate severe adult presentations. Avulsion is the most procedurally demanding form of brachial plexus injury because the nerve root is torn from the spinal cord, which removes the option of standard intraplexal grafting in many cases. That clinical severity raises the average treatment intensity in the United States brachial plexus injury industry, because surgeons often need extraplexal donor strategies such as intercostal or spinal accessory transfers. It also increases the role of academic referral centers, since complete and near-complete plexus injuries demand higher operating room coordination, advanced imaging, and longer follow-up.

Neuroma is the fastest-growing injury subtype, with a 7.36% CAGR through 2031, as clinicians are paying closer attention to painful nerve sequelae after incomplete recovery or failed reconstruction. That shift broadens the United States brachial plexus injury market beyond acute trauma repair and pushes more attention toward chronic functional loss, pain relief, and revision pathways. Rupture and stretch injuries remain important because they create a stable base of lower-acuity treatment demand across diagnostics, medication, therapy, and rehabilitation. Together, that mix leaves the United States brachial plexus injury market anchored by avulsion in value terms, while neuroma expands the addressable pool in later-stage care.

Surgical treatment accounted for 51.17% of the United States brachial plexus injury market size in 2025, which confirms that procedure-based care still drives the largest share of revenue. That segment includes nerve repair, grafting, transfer, and microsurgical reconstruction, which together carry the highest procedural complexity and the strongest reimbursement intensity in the United States brachial plexus injury market. Nerve transfer was used in 48% of all brachial plexus injury surgeries, which shows how central reconstructive strategy has become in current practice. Published outcomes also favor more advanced transfer protocols in selected cases, with the Oberlin 2 technique showing stronger sEMG signals for elbow flexion recovery than intercostal-to-musculocutaneous transfers.

Physical therapy is projected to grow at 8.87% CAGR through 2031, which makes it the fastest-growing treatment category in the United States brachial plexus injury market. This change reflects a broader clinical shift, because rehabilitation is increasingly treated as a co-primary pathway rather than something that starts only after surgery. German clinical guidance published in 2024 placed high importance on long-term ergotherapy and physiotherapy in interdisciplinary peripheral nerve care, and that position aligns with how leading U.S. programs now structure treatment planning. Medication and rehabilitation services, therefore, continue to support the United States brachial plexus injury industry even when delayed presentation, comorbidity, or payer rules prevent surgery.

Complete Report Scope:

- By Type of Injury

- Avulsion

- Rupture

- Neuroma

- Stretch

- By Treatment Type

- Surgical Treatment

- Physical Therapy

- Medication

- Rehabilitation

- By Patient Demographics

- Infants

- Adults

- Elderly

- By Diagnostic Method

- Electromyography

- Ultrasound

- Magnetic Resonance Imaging

- By End User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Rehabilitation Centers

List of Companies Covered in this Report:

- Arthrex

- B. Braun

- Baxter

- Beckton Dickinson

- Boston Scientific

- Cardinal Health

- Cook Group

- FUJIFILM

- HCA Healthcare, Inc.

- Integra LifeSciences

- Johnson & Johnson

- Medtronic

- Olympus

- Orthofix

- Pacira BioSciences

- Smiths Group

- Stryker

- Teleflex

- Terumo

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Traumatic Injury Burden From Road Accidents and Sports Incidents

- 4.2.2 High Surgical Receptivity for Severe Root Avulsion and Complex Plexus Damage

- 4.2.3 Expanding Access to Multidisciplinary Nerve Reconstruction and Rehabilitation Centers

- 4.2.4 Faster Adoption of AI-Assisted Imaging and Intraoperative Nerve Monitoring

- 4.2.5 Higher Coverage for Medically Necessary Reconstructive Care and Rehabilitation

- 4.2.6 Growing Clinical Use of Nerve Transfer and Microsurgical Reconstruction

- 4.3 Market Restraints

- 4.3.1 Narrow Surgical Timing Window Reduces Treatable Patient Pool

- 4.3.2 Scarcity of Subspecialty Surgeons Slows Referral-to-Treatment Conversion

- 4.3.3 High Episode Cost and Rehabilitation Intensity Limit Utilization

- 4.3.4 Uneven Access to Specialized Follow-Up Care Limits Functional Recovery Pathways

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type of Injury

- 5.1.1 Avulsion

- 5.1.2 Rupture

- 5.1.3 Neuroma

- 5.1.4 Stretch

- 5.2 By Treatment Type

- 5.2.1 Surgical Treatment

- 5.2.2 Physical Therapy

- 5.2.3 Medication

- 5.2.4 Rehabilitation

- 5.3 By Patient Demographics

- 5.3.1 Infants

- 5.3.2 Adults

- 5.3.3 Elderly

- 5.4 By Diagnostic Method

- 5.4.1 Electromyography

- 5.4.2 Ultrasound

- 5.4.3 Magnetic Resonance Imaging

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Specialty Clinics

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Rehabilitation Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Baxter International Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Cardinal Health Inc.

- 6.3.7 Cook Medical LLC

- 6.3.8 Fujifilm Holdings Corporation

- 6.3.9 HCA Healthcare, Inc.

- 6.3.10 Integra LifeSciences Holdings Corporation

- 6.3.11 Johnson and Johnson

- 6.3.12 Medtronic plc

- 6.3.13 Olympus Corporation

- 6.3.14 Orthofix Medical Inc.

- 6.3.15 Pacira BioSciences, Inc.

- 6.3.16 Smith and Nephew plc

- 6.3.17 Stryker Corporation

- 6.3.18 Teleflex Incorporated

- 6.3.19 Terumo Corporation

- 6.3.20 Zimmer Biomet Holdings Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment