PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072853

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072853

United States Dental Elevator and Luxator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

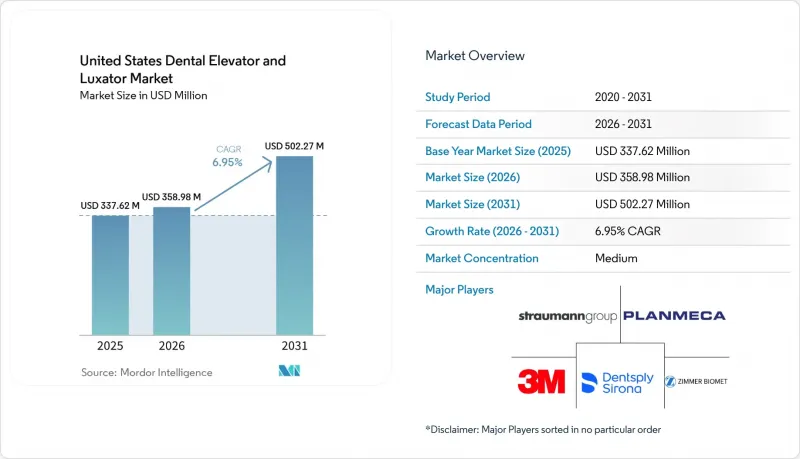

According to Mordor Intelligence, the united states dental elevator and luxator market size is expected to increase from USD 337.62 million in 2025 to USD 358.98 million in 2026 and reach USD 502.27 million by 2031, growing at a CAGR of 6.95% over 2026-2031.

This report is Segmented by Product Type (Dental Elevators, Dental Luxators), Size (5 Mm, 3 Mm, 2 Mm, 4 Mm, 10 Mm), End User (Dental Clinics, Hospitals and Clinics, Research and Academic Institutes). The Market Forecasts are Provided in Terms of Value (USD).

United States Dental Elevator and Luxator Market Trends and Insights

Rising Geriatric Dental Extractions: Aging Demographics Structurally Underpin Instrument Demand

The United States dental elevator and luxator market is closely linked to the fast rise in older adults across the country. The U.S. population aged 65 and older reached 61.2 million in 2024 and accounted for 18% of the total population, with annual growth of 3.1% from 2023 to 2024. Older adults carry heavier tooth loss burdens, and NIDCR reports that people aged 65 and older had 20.7 remaining teeth on average, while 17.3% were fully edentulous. Even among seniors who still retain teeth, the average of 10.7 missing teeth points to a continuing flow of difficult extractions that often involve roots, brittle bone, and periodontally compromised sites. This keeps demand in the United States dental elevator and luxator market tied to necessary procedures rather than optional spending. The long runway also matters because a 2025 article in Frontiers in Dental Medicine projects the U.S. population aged 65 and older to reach 98 million by 2060, which supports sustained extraction-related instrument demand well beyond the current forecast period.

Expansion of Outpatient Dental Care Networks: DSO Scale Generates Standardized Procurement Demand

The United States dental elevator and luxator market is also gaining from the growth of larger outpatient care networks. DSO-affiliated dentists represented 16.1% of all U.S. dentists in 2024, more than double the 7.4% recorded in 2015, and group practice participation has continued to rise. As DSOs expand, purchasing decisions move away from single-clinician choice and toward approved supplier lists, which creates repeatable order flows for oral-surgery hand instruments. Coverage expansion is widening the treatable patient base, because CMS finalized in 2024 that states may add routine adult dental services as an essential health benefit starting in January 2027. A December 2025 Medicaid dental benefits report showed that 38 states and the District of Columbia offered enhanced adult dental benefits in 2025, and 18 states had expanded adult dental benefits since 2021 without any state rolling back benefits. As outpatient care networks scale against this coverage backdrop, the United States dental elevator and luxator market is likely to see fewer minor brands on formularies and greater concentration in approved vendor lists that can support quality and volume at the same time.

Inconsistent Reimbursement for Routine Extraction Instruments: Coverage Gaps Constrain Facility Budgets

The United States dental elevator and luxator market still faces a reimbursement problem because procedure payment does not directly translate into instrument-specific recovery. CareQuest reported in 2025 that 26% of U.S. adults, equal to 69 million people, lacked dental coverage, which leaves many providers operating in unstable demand environments. Safety-net clinics and FQHCs usually manage budgets around reimbursable procedures, staffing, and essential consumables, so hand instruments compete for funds with more immediate operating needs. CMS policy changes improve the long-term coverage environment, but they do not reimburse the purchase of specific elevators or luxators as separate billable items. This creates uneven replacement cycles across states, because better-covered markets can refresh trays more regularly while low-coverage markets stretch instrument life. The result is slower premium adoption in the parts of the United States dental elevator and luxator market that are most budget-sensitive.

Other drivers and restraints analyzed in the detailed report include:

- High Burden of Periodontal Disease and Tooth Loss: Disease Prevalence Generates Recurring Procedure Volume

- Shift Toward Minimally Traumatic Extraction Techniques: Socket Preservation Science Differentiates Luxators from Forceps

- Price Pressure From Standardized Low-Cost Imports: Commodity Tier Erodes Pricing Power for Premium Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dental elevators held 63.48% of the United States dental elevator and luxator market share in 2025, which reflected their long-standing role in routine extraction workflows across U.S. practices. Their wide use across incisor, premolar, and molar procedures keeps them as the default choice in many general dentistry and oral-surgery trays. Straight, cryer, and apical designs remain familiar to clinicians because they are deeply embedded in training, case setup, and basic inventory planning. This entrenched position gives elevators a stable demand base inside the United States dental elevator and luxator market, even as procedural techniques continue to evolve.

Dental luxators are forecast to grow at 7.36% CAGR through 2031, which is faster than the 7% overall pace of the United States dental elevator and luxator market. Their stronger growth reflects the fact that luxators sit closer to atraumatic extraction and implant-preparatory workflows, where bone preservation has direct financial and clinical value. The 2024 expert consensus on minimally invasive extraction specifically supported periodontal ligament instruments as first-line tools, which gives suppliers a clearer clinical basis for tray inclusion and premium positioning. This shift also improves product mix for manufacturers, because luxators, especially ergonomic and premium-finish variants, usually sell at higher average prices than standard elevators.

Complete Report Scope:

- By Product Type

- Dental Elevators

- Dental Luxators

- By Size

- 5 mm

- 3 mm

- 2 mm

- 4 mm

- 10 mm

- By End User

- Dental Clinics

- Hospitals and Clinics

- Research and Academic Institutes

List of Companies Covered in this Report:

- 3M

- Aesculap

- Biolase, Inc.

- B. Braun

- Brasseler Holdings, LLC

- Brasseler USA

- DentalEZ Group

- Dentsply Sirona

- Henry Schein

- Hu-Friedy Mfg

- Kerr Dental

- KLS Martin Group

- Medesy S.r.l.

- Nordent Manufacturing, Inc.

- Otto Leibinger GmbH

- Patterson Companies

- Planmeca

- Straumann Group

- Titan Instruments, Inc.

- Zimmer Biomet

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Dental Extractions

- 4.2.2 Expansion of Outpatient Dental Care Networks

- 4.2.3 High Burden of Periodontal Disease and Tooth Loss

- 4.2.4 Shift Toward Minimally Traumatic Extraction Techniques

- 4.2.5 Ergonomic Tool Design and Material Innovation

- 4.2.6 Sterile, Single-Use, and Clinic-Specific Instrument Bundling

- 4.3 Market Restraints

- 4.3.1 Inconsistent Reimbursement for Routine Extraction Instruments

- 4.3.2 Price Pressure From Standardized Low-Cost Imports

- 4.3.3 Clinical Preference for Multi-Use Alternatives and Conventional Forceps

- 4.3.4 Limited Procedure Differentiation in a Mature Hand Instrument Category

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Dental Elevators

- 5.1.2 Dental Luxators

- 5.2 By Size

- 5.2.1 5 mm

- 5.2.2 3 mm

- 5.2.3 2 mm

- 5.2.4 4 mm

- 5.2.5 10 mm

- 5.3 By End User

- 5.3.1 Dental Clinics

- 5.3.2 Hospitals and Clinics

- 5.3.3 Research and Academic Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M

- 6.3.2 Aesculap, Inc.

- 6.3.3 Biolase, Inc.

- 6.3.4 B. Braun SE

- 6.3.5 Brasseler Holdings, LLC

- 6.3.6 Brasseler USA

- 6.3.7 DentalEZ Group

- 6.3.8 Dentsply Sirona Inc.

- 6.3.9 Henry Schein, Inc.

- 6.3.10 Hu-Friedy Mfg. Co., LLC

- 6.3.11 Kerr Dental

- 6.3.12 KLS Martin Group

- 6.3.13 Medesy S.r.l.

- 6.3.14 Nordent Manufacturing, Inc.

- 6.3.15 Otto Leibinger GmbH

- 6.3.16 Patterson Companies, Inc.

- 6.3.17 PLANMECA OY

- 6.3.18 Straumann Group

- 6.3.19 Titan Instruments, Inc.

- 6.3.20 Zimmer Biomet Holdings, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment