PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072938

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072938

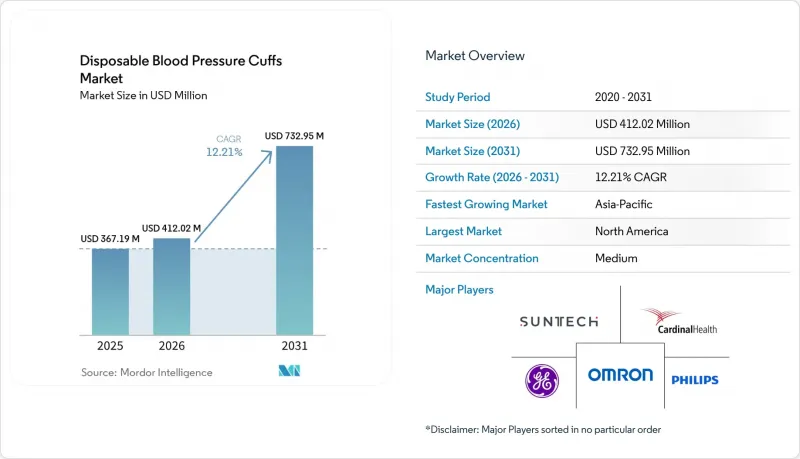

Disposable Blood Pressure Cuffs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the disposable blood pressure cuffs market size is projected to expand from USD 367.19 million in 2025 and USD 412.02 million in 2026 to USD 732.95 million by 2031, registering a CAGR of 12.21% between 2026 to 2031.

This report is Segmented by Product Type (Adult Disposable Blood Pressure Cuffs, and More), Material (Vinyl Disposable Blood Pressure Cuffs, and More), End User (Hospitals, Ambulatory Surgical Centers, Clinics, Home Care Settings, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Disposable Blood Pressure Cuffs Market Trends and Insights

Rising Infection-Control Protocols in Procedures

The disposable blood pressure cuffs market is experiencing growth due to stricter infection-control protocols. In April 2025, the CDC updated its guidelines, requiring reusable medical equipment, including blood pressure cuffs, to be cleaned and reprocessed before reuse. Staff involved in reprocessing must also undergo training and periodic assessments. Evidence shows contamination on portable non-critical devices is frequent enough to influence procurement decisions. When hospitals account for disinfectants, documentation, staff time, and quality checks, the cost difference between reusable and disposable cuffs becomes less clear. Additionally, a 2025 multisociety guidance paper increased pressure on healthcare systems to improve sterilization and disinfection practices, further driving demand for disposable cuffs.

Shift Toward Patient-Per-Use Accessories in ICUs

ICUs and NICUs are significantly contributing to the growth of the disposable blood pressure cuffs market due to high patient vulnerability and intensive monitoring needs. A 2025 study revealed that 40.1% of critically ill neonates developed healthcare-associated infections, with 30.3% experiencing sepsis and higher mortality rates in those under 750 g. Neonatal care involves repeated cuff inflation and skin contact, increasing cross-contamination risks. Standardized neonatal blood pressure charts, implemented in January 2024, have improved monitoring discipline, leading to higher cuff usage per patient. This trend highlights that demand in intensive care grows with monitoring frequency, not just patient admissions.

Higher Per-Patient Consumable Cost Versus Reusable

In budget-conscious hospitals, outpatient clinics, and government-led tenders, financial teams often evaluate disposable blood pressure cuffs based on their per-patient consumable cost. This focus on unit price limits market penetration in facilities with reusable cuffs, trained staff, and established cleaning routines, despite hidden labor and compliance costs. In emerging markets, centralized purchasing separates infection-control decisions from budgets handling clinical and administrative consequences. Transitioning to disposable cuffs requires changes in ordering, storage, staff preferences, and materials management, slowing adoption in price-sensitive environments.

Other drivers and restraints analyzed in the detailed report include:

- Standardization of Cuff Sizing to Reduce Misdiagnosis

- Growth in Contract Manufacturing for Private Label Brands

- Waste-Handling and Sustainability Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, adult disposable blood pressure cuffs accounted for 39.63% of the market, reflecting the routine nature of adult blood pressure monitoring in hospitals, clinics, and surgical centers. This segment dominates the market as adult patients represent the majority of daily monitoring in healthcare facilities. Rising obesity rates are driving demand for the 'others' category, which includes thigh and large-arm formats, where standard adult cuffs are unsuitable.

Pediatric disposable blood pressure cuffs are projected to grow at a 14.38% CAGR through 2031, making them the fastest-growing segment. Increased focus on blood pressure screening and monitoring for at-risk children is driving this growth. Neonatal cuffs, though a smaller niche, require higher sensitivity due to critical factors like fit and monitor performance, positioning suppliers with diverse size ranges favorably in premium hospital accounts.

Complete Report Scope:

- By Product Type

- Adult Disposable Blood Pressure Cuffs

- Pediatric Disposable Blood Pressure Cuffs

- Neonatal Disposable Blood Pressure Cuffs

- Others

- By Material

- Vinyl Disposable Blood Pressure Cuffs

- Nylon Disposable Blood Pressure Cuffs

- Thermoplastic Polyurethane Disposable Blood Pressure Cuffs

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Home Care Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 38.86% of the disposable blood pressure cuffs market share, maintaining its lead due to robust infection prevention systems and a higher willingness to invest in compliance-ready products. The U.S. market benefits from CDC guidelines and accreditation-linked purchasing standards, which drive healthcare facilities toward single-patient-use programs or improved reprocessing practices. Canada follows a similar trend, while Mexico shows growth potential as private hospitals modernize their clinical equipment. Baxter's expansion of U.S. manufacturing for Welch Allyn FlexiPort cuffs in 2025 enhanced supply resilience and strengthened local supply confidence.

Europe held a significant share of the disposable blood pressure cuffs market in 2025, shaped by the balance between infection control needs and environmental concerns. Strong clinical standards in Germany, the U.K., France, and the Nordics support the market, with procurement teams focusing on patient safety and device performance. The U.K. is exploring reusable alternatives to assess their impact on waste and emissions. Regions like Italy, Spain, Eastern Europe, and Turkey offer growth opportunities due to hospital modernization and expanding ambulatory care networks.

Asia-Pacific is projected to grow at a 14.67% CAGR through 2031, making it the fastest-growing region in the disposable blood pressure cuffs market. Growth in China and India is driven by hospital network expansion and demand for cost-effective, compliant consumables, while Japan and South Korea focus on premium care environments. The region benefits from increased manufacturing depth, supported by Covestro's localization of medical-grade TPU production in Taiwan. In the Middle East, Africa, and South America, private hospital expansions and rising infection-control expectations are gradually driving the adoption of single-patient-use cuffs. In the GCC, accreditation goals among private hospitals are boosting demand for disposable monitoring accessories that meet international standards.

- American Diagnostic

- B. Braun

- Baxter

- Beurer

- Cardinal Health

- Contec Medical Systems

- GE HealthCare Technologies Inc.

- Halma

- Koninklijke Philips

- Mckesson

- Medline Industries

- Microlife

- Midmark

- Nihon Kohden

- OMRON

- OSI Systems, Inc.

- Schiller

- Mindray

- Spacelabs Healthcare, Inc.

- SunTech Medical, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Infection-Control Protocols in Procedural and Inpatient Settings

- 4.2.2 Expansion of Single-Use Clinical Consumables Procurement by Hospitals and IDNs

- 4.2.3 Standardization of Cuff Sizing to Reduce Miscuffing and Liability Risk

- 4.2.4 Shift Toward Patient-Per-Use Accessories in High-Acuity and Isolation Workflows

- 4.2.5 Growth in Contract Manufacturing for Private-Label Disposable Monitoring Accessories

- 4.2.6 Compatibility With Multi-Vendor Monitor Fleets Through Universal Connector Designs

- 4.3 Market Restraints

- 4.3.1 Higher Per-Patient Consumable Cost Versus Reusable Cuffs

- 4.3.2 Hospital Reprocessing Habits and Installed Base Stickiness in Low-Infection-Risk Settings

- 4.3.3 Connector Fragmentation Across Monitor Platforms Creates Inventory Complexity

- 4.3.4 Waste-Handling and Sustainability Pressure on Single-Use Medical Textiles and Plastics

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Adult Disposable Blood Pressure Cuffs

- 5.1.2 Pediatric Disposable Blood Pressure Cuffs

- 5.1.3 Neonatal Disposable Blood Pressure Cuffs

- 5.1.4 Others

- 5.2 By Material

- 5.2.1 Vinyl Disposable Blood Pressure Cuffs

- 5.2.2 Nylon Disposable Blood Pressure Cuffs

- 5.2.3 Thermoplastic Polyurethane Disposable Blood Pressure Cuffs

- 5.2.4 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Clinics

- 5.3.4 Home Care Settings

- 5.3.5 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 American Diagnostic Corporation

- 6.3.2 B. Braun Melsungen AG

- 6.3.3 Baxter International Inc.

- 6.3.4 Beurer GmbH

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Contec Medical Systems Co., Ltd.

- 6.3.7 GE HealthCare Technologies Inc.

- 6.3.8 Halma plc

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 McKesson Corporation

- 6.3.11 Medline Industries, LP

- 6.3.12 Microlife Corporation

- 6.3.13 Midmark Corporation

- 6.3.14 Nihon Kohden Corporation

- 6.3.15 OMRON Corporation

- 6.3.16 OSI Systems, Inc.

- 6.3.17 Schiller AG

- 6.3.18 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.19 Spacelabs Healthcare, Inc.

- 6.3.20 SunTech Medical, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment