PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072962

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072962

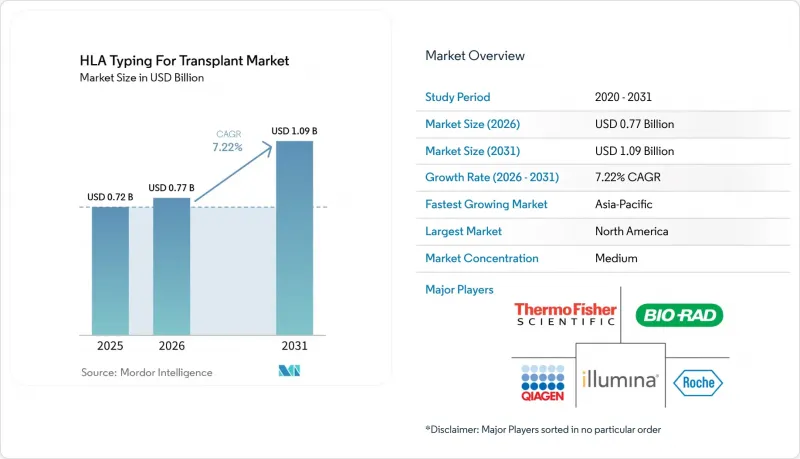

HLA Typing For Transplant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the HLA typing for transplant market size is projected to expand from USD 0.72 billion in 2025 and USD 0.77 billion in 2026 to USD 1.09 billion by 2031, registering a CAGR of 7.22% between 2026 to 2031.

This report is Segmented by Products and Services (Reagents & Consumables, Instruments, Software & Services), Technology (PCR-Based, NGS-Based, Sanger, Other), Transplant Type (Solid Organ, HSCT), End User (Reference Laboratories, Hospitals & Transplant Centers, Research Institutes), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global HLA Typing For Transplant Market Trends and Insights

Rising Organ Transplant Volumes

The HLA Typing for Transplant market continues to gain volume support from the steady expansion of transplant procedures across major organ categories. Global solid organ transplants reached 173,727 procedures in 2024, which marked the highest level recorded by the Global Observatory on Donation and Transplantation. Kidney transplants reached 110,467, liver transplants reached 42,497, lung transplants reached 8,236, and heart transplants reached 10,287 in 2024, and each of these procedures required compatibility testing before transplantation. Donation after circulatory determination of death also expanded by 17% in 2024, which increased the share of time-sensitive deceased-donor typing events and pushed laboratories toward faster workflows. Japan's revised 2025 heart transplantation guidelines further reinforced the clinical role of HLA matching for cardiac recipients, which added another high-value testing layer in a volume-constrained but quality-driven setting. As a result, the HLA Typing for Transplant market is seeing both higher unit demand and a stronger case for rapid, high-resolution assays.

Shift Toward Precise Donor-Recipient Matching

The HLA Typing for Transplant market is moving beyond basic compatibility and toward more precise donor-recipient evaluation. Transplant centers are using epitope-based matching and molecular mismatch scoring more often because these methods support the reduction of antibody-mediated rejection and sensitization events. Research published in 2026 showed that real-time molecular mismatch estimation using rSSO-defined HLA allele strings can be applied in deceased-donor allocation workflows without delaying organ placement. This change is pushing laboratories to supplement or replace PCR-SSP outputs with full-field NGS data, especially for retransplant candidates and sensitized patients. It is also widening the clinical scope of each pre-transplant workup because more data points are being used to judge transplant suitability. That shift is giving the HLA Typing for Transplant market a stronger pull toward premium assays and more advanced interpretation software.

High Cost of NGS-Based HLA Typing Workflows

The HLA Typing for Transplant market still faces a meaningful cost barrier when laboratories move from older sequence-based methods to NGS. Comparative research published in 2024 showed that the transition brings more processing steps, more manual workload, and longer turnaround risk if workflows are not fully optimized. Laboratories also need to absorb maintenance expense, bioinformatics infrastructure, validation requirements, and long-term data retention obligations. In the United States, HLA typing for solid organ transplantation is treated under organ acquisition cost bundles in the Medicare MolDX framework rather than as a separately billable laboratory service, which limits direct recovery of NGS-specific costs. The cost gap remains more visible in smaller public-sector programs and lower-volume transplant centers than in large centralized reference networks. This restraint keeps the HLA Typing for Transplant market tilted toward laboratories that can spread platform and compliance costs across broader testing volumes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Molecular HLA Testing Adoption

- Workflow Automation in High-Throughput Transplant Labs

- Interoperability Gaps Between LIS, HLA Software, and Hospital Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and Consumables accounted for 70.31% share of the HLA Typing for Transplant market size in 2025, which kept this category in the leading revenue position. That share reflected the recurring purchasing pattern attached to molecular transplant diagnostics, where every workup requires fresh assay inputs across typing, crossmatch preparation, and antibody-related testing. The HLA Typing for Transplant market therefore gives reagents a more stable demand profile than instruments, because laboratories can postpone equipment upgrades but cannot avoid daily consumable use. The move toward broader and higher-resolution NGS assays is also lifting per-event reagent value because more loci are being typed and more complex compatibility questions are being addressed in routine workflows. Long-read platform launches are reinforcing that pattern because they expand the range of kits that can command premium pricing in the HLA Typing for Transplant market.

Software and Services is projected to grow at 9.38% CAGR through 2031, which makes it the fastest-growing sub-segment in this part of the HLA Typing for Transplant industry. The traditional gap between assay value capture and informatics value capture is narrowing because NGS has made software central to the commercial proposition and not just to laboratory enablement. Analysis tools now help shape vendor choice, workflow speed, data interpretation, and platform stickiness. That shift is becoming more important as laboratories ask for integrated reporting and fewer handoffs between sequencing, allele calling, and final review. EuroBio Scientific's April 2026 agreement to acquire CareDx's transplant lab products division points to that broader convergence, because assay kits and related workflow assets are being consolidated under the GenDx commercial structure. The HLA Typing for Transplant market is therefore giving software and services a larger role in revenue mix as vendors compete to own more of the sample-to-report path.

Molecular Assay Technologies held 80.24% revenue share in 2025, which kept this category at the center of the HLA Typing for Transplant market. That broad grouping includes PCR-based methods, NGS-based methods, and Sanger sequencing, but the internal growth balance is now shifting more clearly toward NGS. NGS-based HLA typing is projected to expand at 10.52% CAGR through 2031, which places the HLA Typing for Transplant market size for this sub-segment above the overall market growth rate. The main reason is clinical demand for high-resolution allele calls that can support better donor selection and reduce the need for retesting. PCR-based approaches still hold value in rapid or screening-oriented workflows, yet they are increasingly being used as complements to sequencing rather than as full substitutes for high-resolution analysis in the HLA Typing for Transplant market.

Long-read sequencing is also moving from research and validation settings into more visible clinical positioning. GenDx reported robust high-resolution results from blood and buccal swab samples across both Illumina and Oxford Nanopore platforms in 3 independent clinical laboratory validations, which supports a more platform-agnostic commercial environment. Werfen's May 2026 launch of NanoTYPE HLA-11 Plus as a CE-IVD product marked an important regulatory step because it was presented as the first CE-IVD full-gene HLA typing kit across all 11 classical HLA genes. PacBio also remains relevant in this shift because its HiFi sequencing offering is being positioned around 99.9% accuracy and four-field allele resolution across classical HLA loci. Sanger-based typing and non-molecular methods still retain some presence in lower-infrastructure settings, but the HLA Typing for Transplant market is increasingly rewarding workflows that deliver full-gene resolution and stronger validation support.

Complete Report Scope:

- By Products and Services

- Reagents and Consumables

- Instruments

- Software and Services

- By Technology

- Molecular Assay Technologies

- PCR Based HLA Typing

- Next Generation Sequencing Based HLA Typing

- Sanger Sequencing Based HLA Typing

- Other Technologies

- By Transplant Type

- Solid Organ Transplantation

- Kidney Transplantation

- Liver Transplantation

- Heart Transplantation

- Lung Transplantation

- Hematopoietic Stem Cell Transplantation

- By End User

- Independent Reference Laboratories

- Hospitals and Transplant Centers

- Research Laboratories and Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 45.22% share of the HLA Typing for Transplant market size in 2025, which kept it in the leading regional position. The United States remains the main contributor because its transplant ecosystem links organ procurement organizations, transplant centers, and ASHI-accredited histocompatibility laboratories in a structured way. The reimbursement framework also supports procurement continuity because HLA typing costs for solid organ transplantation are embedded within organ acquisition cost bundles under Medicare rules. That structure does not remove all pricing pressure, but it gives laboratories more visibility than in many other regions. Canada is adding to regional demand through continued investment in high-resolution typing capacity, while Mexico remains earlier in development with a smaller but growing private-sector transplant base.

Europe remained the second-largest regional block in the HLA Typing for Transplant market, with Germany, the United Kingdom, and France leading by testing sophistication and institutional depth. German university hospital laboratories such as Charite Berlin, University Medical Center Mainz, and University Hospital Leipzig operate accredited transplant immunology services that support high-resolution HLA typing in clinical practice. The regional product cycle is also becoming more active as vendors position their portfolios for the regulatory transition under IVDR, and Werfen's CE-IVD long-read launch in May 2026 is a clear example of that push. Italy, Spain, and the wider Rest of Europe are increasingly important for outsourced high-resolution services because not every transplant center can sustain in-house NGS operations at accredited scale.

Asia-Pacific is projected to grow at 8.65% CAGR through 2031, which makes it the fastest-growing geography in the HLA Typing for Transplant market. China is a major part of that expansion because 15,387 combined kidney and liver transplants from deceased donors were recorded there in 2024. Japan also supports high per-procedure value through its transplant immunogenetics framework and its revised 2025 heart transplantation guidelines that include HLA matching considerations. India and South Korea are expanding transplant capacity quickly and are creating stronger demand for outsourced molecular typing, while South America and Middle East and Africa remain smaller regional pools with Brazil and GCC countries acting as the main points of structured investment.

- Abbott Laboratories

- BAG Health Care GmbH

- Beckton Dickinson

- Bio-Rad Laboratories

- CareDx, Inc.

- DiaSorin

- Eurofins

- Roche

- GenDx

- HistoGenetics, LLC

- Illumina

- Immucor

- Omixon

- PacBio

- QIAGEN

- Takara Bio

- TBG Diagnostics

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Organ Transplant Volumes

- 4.2.2 Shift Toward Precise Donor Recipient Matching

- 4.2.3 Expansion of Molecular HLA Testing Adoption

- 4.2.4 Growth in Personalized Medicine and Immunogenomics

- 4.2.5 Workflow Automation in High Throughput Transplant Labs

- 4.2.6 Rising Clinical Use of Post Transplant Monitoring Panels

- 4.3 Market Restraints

- 4.3.1 High Cost of NGS Based HLA Typing Workflows

- 4.3.2 Uneven Reimbursement and Procurement Cycles Across Regions

- 4.3.3 Limited Donor Typing Infrastructure in Emerging Markets

- 4.3.4 Interoperability Gaps Between LIS, HLA Software, and Hospital Systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Products and Services

- 5.1.1 Reagents and Consumables

- 5.1.2 Instruments

- 5.1.3 Software and Services

- 5.2 By Technology

- 5.2.1 Molecular Assay Technologies

- 5.2.2 PCR Based HLA Typing

- 5.2.3 Next Generation Sequencing Based HLA Typing

- 5.2.4 Sanger Sequencing Based HLA Typing

- 5.2.5 Other Technologies

- 5.3 By Transplant Type

- 5.3.1 Solid Organ Transplantation

- 5.3.2 Kidney Transplantation

- 5.3.3 Liver Transplantation

- 5.3.4 Heart Transplantation

- 5.3.5 Lung Transplantation

- 5.3.6 Hematopoietic Stem Cell Transplantation

- 5.4 By End User

- 5.4.1 Independent Reference Laboratories

- 5.4.2 Hospitals and Transplant Centers

- 5.4.3 Research Laboratories and Academic Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 BAG Health Care GmbH

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Bio-Rad Laboratories, Inc.

- 6.3.5 CareDx, Inc.

- 6.3.6 DiaSorin S.p.A.

- 6.3.7 Eurofins Scientific SE

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 GenDx

- 6.3.10 HistoGenetics, LLC

- 6.3.11 Illumina, Inc.

- 6.3.12 Immucor, Inc.

- 6.3.13 Omixon Inc.

- 6.3.14 PacBio

- 6.3.15 QIAGEN N.V.

- 6.3.16 Takara Bio Inc.

- 6.3.17 TBG Diagnostics Limited

- 6.3.18 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space and Unmet-Need Assessment