PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072993

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072993

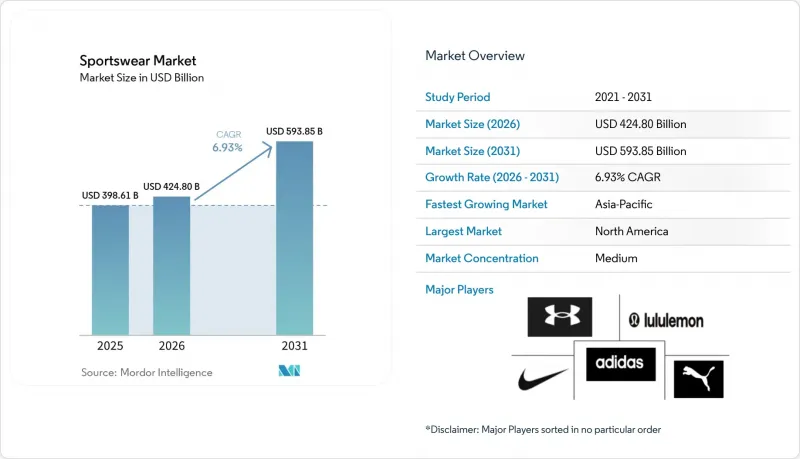

Sportswear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sportswear market size is expected to increase from USD 398.61 billion in 2025 to USD 424.80 billion in 2026 and reach USD 593.85 billion by 2031, growing at a CAGR of 6.93% over 2026-2031.

This report is Segmented by Product Type (Sports Apparel, Sports Shoes, and Accessories), Sports Type (Golf, Soccer, Basketball, and More), End-User (Men, Women, Children), Distribution Channel (Online Retail Stores and Offline Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Sportswear Market Trends and Insights

Rising Fitness Participation Broadens the Consumer Base

The sportswear market is drawing support from historically high sports and fitness participation across mature and developing regions. The Sports & Fitness Industry Association reported that 250 million Americans joined at least 1 sport or fitness activity in 2025, while team sports participation moved past 90 million. The same report showed that only 32% of Americans met the federal guideline for weekly moderate activity, which leaves a large participation gap that can still convert into future apparel demand. This matters for the sportswear market because participation now extends beyond dedicated athletes and into everyday wellness routines. That wider user base supports repeat demand across shoes, apparel, and accessories instead of relying only on event-driven purchases.

Product Innovation in Performance Fabrics Repositions Quality Benchmarks

The sportswear market is also being shaped by a stronger product cycle centered on technical fabrics and material science. Nike introduced Aero-FIT for 2026 football kits with higher airflow and a construction made from 100% textile waste through advanced chemical recycling. In February 2026, Lululemon launched PowerLu, a new proprietary fabric designed for strength training with targeted support and motion range. These launches show that better cooling, support, and recycled inputs are becoming core buying factors instead of optional upgrades. In the sportswear market, brands that connect performance and sustainability in the same product are in a better position to support premium pricing and stronger brand loyalty.

Counterfeit Sportswear Products Erode Brand Revenue and Consumer Trust

Counterfeit supply remains a direct challenge for the sportswear market, especially around high-visibility tournament periods. In April 2025, OLAF and Spanish customs seized 1.5 tonnes of counterfeit sportswear that was headed for a major football event. The European Union Intellectual Property Office reported that counterfeiting continues to damage legitimate clothing sales and employment across the region. The International Trademark Association also noted that mobile-first shopping and deceptive websites are making it harder for consumers to identify genuine sellers . In the sportswear market, brands with stronger authentication tools and better channel control are more likely to protect pricing power and trust through major event cycles.

Other drivers and restraints analyzed in the detailed report include:

- Athleisure Expansion Converts Casual Consumers into Regular Buyers

- Celebrity Endorsements and Major Sporting Events Spike Near-Term Demand

- Supply Chain Disruptions Drive Up Input Costs and Constrain Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sports shoes held 62.0% share in 2025, which made them the largest product category in the sportswear market. Their lead reflects higher average selling prices and steady demand across performance, casual, and sport-casual use. Sportswear remained the second-largest product type and continued to benefit from the same athleisure crossover that supports broader category demand. This pattern shows that the sportswear industry is still anchored by footwear economics, even as apparel narratives become more product-led.

Accessories are projected to grow at an 8.0% CAGR through 2031, making them the fastest-expanding product type in the sportswear market. Growth is being supported by compression gear, sports bags, hydration products, and other performance-adjacent purchases that consumers now treat as part of a full activity setup. PUMA strengthened this part of the innovation chain in March 2026 when it partnered with Shincell New Materials to co-develop the next generation of NITRO foam and opened a joint laboratory in Suzhou. Nike also reported 16% equipment growth in North America in fiscal 2025, which supports the view that accessories are becoming a repeat purchase category rather than an occasional add-on

Running accounted for 38.6% of the sportswear market size in 2025, and it is forecast to expand at an 8.4% CAGR through 2031. That makes running both the largest and fastest-growing sports type in the sportswear market. The segment benefits from recurring demand because runners replace shoes and technical apparel more frequently than many other user groups. Running also sets the tone for fabric innovation, fit, and comfort across the wider portfolio.

Other sports types continue to create focused opportunities in soccer, basketball, golf, and baseball within the sportswear market. Soccer lines are receiving a lift from the 2026 World Cup cycle, which is raising demand in host and participant markets. Basketball remains commercially important in North America and China, while golf keeps high value per unit because of dress codes and premium buyers. The ssportswear industry also benefits when technical credibility in running carries over into lifestyle and multi-sport collections, which helps brands stretch one area of strength across a broader product mix.

Complete Report Scope:

- Product Type

- Sports Apparel

- Sports Shoes

- Accessories

- Sports Type

- Golf

- Soccer

- Basketball

- Baseball

- Running

- Other Sport Types

- End-User

- Men

- Women

- Children

- Distribution Channel

- Online Retail Stores

- Offline Retail Stores

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 42.2% of the sportswear market size in 2025, which made it the largest regional contributor. The region benefits from high fitness spending, strong brand penetration, and a wide retail base across stores and direct digital channels. The 2026 World Cup is adding another layer of demand across the United States, Canada, and Mexico as brands push team kits and event-led collections. Columbia Sportswear disclosed that it paid USD 80 million in tariffs during Q1 2026 while awaiting refunds, which shows that cost pressure is still affecting operators in the region. Even with those pressures, North America remains a key anchor for the sportswear market because participation habits are keeping demand more resilient than broad apparel spending.

Europe remained the second-largest regional block in the sportswear market, with Germany leading demand and the UK set to record the fastest growth in the region through 2031. The region benefits from strong consumer attention to technical quality and from the presence of major brands such as Adidas and PUMA. Adidas reported record revenue of EUR 24,811 million, or USD 27.2 billion, in 2025, with apparel up 15% and footwear up 12% on a currency-neutral basis. That result shows that Europe still matters as both a demand center and a base for global product and brand development.

Asia Pacific is forecast to grow at an 8.6% CAGR through 2031, which makes it the fastest-growing geography in the sportswear market. China and India are the main demand engines as urbanization, younger consumers, and expanding gym culture increase category reach. The region is also becoming more important in competitive terms because Asian brands are pushing beyond their home bases and building larger international ambitions. The Middle East and Africa remain smaller in current value, but government-backed sports development and football visibility are gradually widening the accessible customer base for the sportswear market.

- Nike Inc.

- Adidas Group

- Puma SE

- Under Armour Inc.

- VF Corporation

- Lululemon Athletica Inc.

- Anta Sports Products Ltd.

- Columbia Sportswear Company

- New Balance Athletics Inc.

- ASICS Corporation

- Fila Holdings Corp.

- Li Ning Company Ltd.

- Mizuno Corporation

- Skechers USA Inc.

- Decathlon SA

- Hanesbrands Inc. (Champion)

- Gap Inc. (Athleta)

- JOMA Sport S.A.

- Authentic Brands Group

- Gildan Activewear Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising participation in fitness and sports activities

- 4.2.2 Product innovation in performance fabrics and design

- 4.2.3 Athleisure expansion converts casual consumers into regular buyers

- 4.2.4 Celebrity endorsements and sports sponsorships boosting demand

- 4.2.5 Expansion of organized sports and fitness clubs

- 4.2.6 Growing female participation in sports activities

- 4.3 Market Restraints

- 4.3.1 Counterfeit sportswear products erode brand revenue and consumer trust

- 4.3.2 Supply chain disruptions drive up input costs and constrain availability

- 4.3.3 Seasonal demand fluctuations across regions

- 4.3.4 Fast-changing fashion trends increasing inventory risks

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Sports Apparel

- 5.1.2 Sports Shoes

- 5.1.3 Accessories

- 5.2 Sports Type

- 5.2.1 Golf

- 5.2.2 Soccer

- 5.2.3 Basketball

- 5.2.4 Baseball

- 5.2.5 Running

- 5.2.6 Other Sport Types

- 5.3 End-User

- 5.3.1 Men

- 5.3.2 Women

- 5.3.3 Children

- 5.4 Distribution Channel

- 5.4.1 Online Retail Stores

- 5.4.2 Offline Retail Stores

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nike Inc.

- 6.4.2 Adidas Group

- 6.4.3 Puma SE

- 6.4.4 Under Armour Inc.

- 6.4.5 VF Corporation

- 6.4.6 Lululemon Athletica Inc.

- 6.4.7 Anta Sports Products Ltd.

- 6.4.8 Columbia Sportswear Company

- 6.4.9 New Balance Athletics Inc.

- 6.4.10 ASICS Corporation

- 6.4.11 Fila Holdings Corp.

- 6.4.12 Li Ning Company Ltd.

- 6.4.13 Mizuno Corporation

- 6.4.14 Skechers USA Inc.

- 6.4.15 Decathlon SA

- 6.4.16 Hanesbrands Inc. (Champion)

- 6.4.17 Gap Inc. (Athleta)

- 6.4.18 JOMA Sport S.A.

- 6.4.19 Authentic Brands Group

- 6.4.20 Gildan Activewear Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK