PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073039

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073039

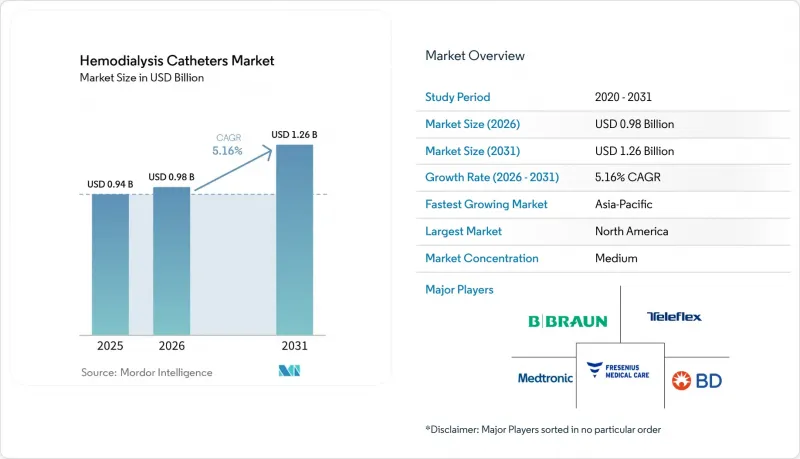

Hemodialysis Catheters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hemodialysis catheters market size is expected to grow from USD 0.94 billion in 2025 to USD 0.98 billion in 2026 and is forecast to reach USD 1.26 billion by 2031 at 5.16% CAGR over 2026-2031.

This report is Segmented by Product Type (Tunneled, Non-Tunneled, and More), Material (Polyurethane, Silicone, and More), Tip Configuration (Step-Tip, Split-Tip, and More), Application (Chronic Hemodialysis, and More), End User (Hospitals, Dialysis Centers, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Hemodialysis Catheters Market Trends and Insights

Rising CKD and End-Stage Renal Disease Burden Structurally Anchors Demand

The hemodialysis catheters market is experiencing increased demand due to the rising global prevalence of chronic kidney disease (CKD). In 2025, 788 million adults worldwide were reported to have CKD, highlighting its growing importance in health system planning. Regions with high disease prevalence but limited treatment access face challenges, leading to late patient arrivals and reliance on emergency catheter placements instead of planned fistula surgeries. In the U.S., the latest USRDS update showed a continued rise in both incident and prevalent end-stage renal disease (ESRD) cases, primarily driven by diabetes and hypertension. Older patients now represent a larger share of the treatment pool, with frailty and comorbidities making traditional access methods less reliable. This has led to increased use of tunneled catheters for extended periods, supporting market growth.

Catheter-Based Hemodialysis Initiation Remains the Clinical Default in Acute Settings

Despite guidelines favoring preplanned permanent access, many patients begin hemodialysis in urgent settings, sustaining demand for hemodialysis catheters. Acute kidney injury and unplanned ESRD presentations make non-tunneled central venous catheters the most practical option in hospitals and emergency units. The CMS 2025 ESRD payment update expanded Medicare coverage for home dialysis related to acute kidney injury, broadening treatment settings for catheter placement. In India, dialysis capacity expanded significantly in 2025 and 2026, with 79 new dialysis centers in Telangana government hospitals and over 6,425 patients served through 4.12 lakh sessions under the PMNDP by December 2025. In emerging markets, limited surgical capacity for fistula creation often results in prolonged use of emergency catheters, driving market growth alongside dialysis network expansion.

CRBSI and Thrombosis Impose Clinical, Regulatory, and Commercial Costs

Catheter-related bloodstream infections (CRBSI) and thrombosis significantly challenge the hemodialysis catheters market by impacting patient safety, increasing hospital costs, and influencing procurement decisions. A 2025 study highlighted that sodium bicarbonate locks achieved infection-free catheter survival rates comparable to gentamicin citrate locks and better than heparin locks. Thrombosis exacerbates these issues by promoting biofilm development, reducing flow, and increasing device abandonment risks. Hospitals now demand measurable performance metrics for premium products, driven by CDC dialysis safety guidance emphasizing strict catheter care, observation, and aseptic practices. This scrutiny raises the competitive bar for manufacturers defending price and market share.

Other drivers and restraints analyzed in the detailed report include:

- Antimicrobial and Biocompatible Catheter Engineering Becomes a Differentiator

- Home Hemodialysis Growth Reshapes Catheter Design Requirements

- Arteriovenous Fistula Prioritization Redirects, but Does Not Eliminate, Catheter Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, tunneled catheters held a 39.81% share of the hemodialysis catheters market, maintaining their position as the leading product type. Their dominance is driven by their widespread use among chronic patients who face challenges with fistula creation, are awaiting access maturation, or are unsuitable for surgical access. Clinicians prefer tunneled systems for their stable flow and extended dwell period, which non-tunneled devices cannot provide. Within this category, cuffed designs are projected to grow at a 6.90% CAGR through 2031, reflecting a shift in demand.

Cuffed designs are gaining traction due to their ability to reduce dislodgement risks and create a barrier against bacterial migration through tissue ingrowth around the cuff. Products like Mozarc Medical's Palindrome Precision line and Teleflex's Arrow ErgoPack systems with antimicrobial technology highlight the segment's evolution toward feature-rich offerings. Non-tunneled catheters remain essential in emergency and ICU settings, where placement speed is critical. The aging dialysis population further drives the relevance of tunneled cuffed devices, as many elderly patients remain catheter-dependent longer than anticipated, balancing urgent-use volume with chronic-care value.

In 2025, polyurethane accounted for 46.35% of the hemodialysis catheters market, making it the leading material. Its mechanical strength, radiopacity, and compatibility with sterilization and coating processes make it suitable for both acute and chronic catheter formats. Polyurethane's leadership is also linked to its adoption in standard product families from major suppliers. Silicone, however, is projected to grow at a 7.25% CAGR through 2031, making it the faster-growing material category.

Material competition is evolving, with future advancements likely to focus on modified polymer chemistry rather than replacing polyurethane or silicone. Polyurethane is expected to maintain its leadership in the short term, while silicone gains traction in applications prioritizing long-dwell comfort and biocompatibility. Both materials are expected to remain relevant for distinct clinical needs.

Complete Report Scope:

- By Product Type

- Tunneled Hemodialysis Catheters

- Cuffed Tunneled Catheters

- Non-Cuffed Tunneled Catheters

- Non-Tunneled Hemodialysis Catheters

- Single Lumen Non-Tunneled Catheters

- Double Lumen Non-Tunneled Catheters

- Triple Lumen Non-Tunneled Catheters

- By Material

- Polyurethane

- Silicone

- Composite and Other Polymer Materials

- By Tip Configuration

- Step-Tip Catheters

- Split-Tip Catheters

- Symmetric Catheters

- Pre-Curved Catheters

- By Application

- Chronic Hemodialysis

- Acute Hemodialysis

- Home Hemodialysis

- By End User

- Hospitals

- Dialysis Centers

- Ambulatory Surgical Centers

- Home Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America held a 42.55% share of the hemodialysis catheters market, maintaining its position as the largest regional player. The United States led this dominance due to its extensive dialysis patient base, advanced insertion capabilities, and widespread use of tunneled catheters in chronic care. The CMS CY 2025 ESRD payment update, which introduced AKI home dialysis payment parity and a new HCPCS code for taurolidine heparin locking solutions, strengthened the catheter care environment. MedPAC projected a 1.7% increase in the 2026 Medicare base payment rate for dialysis services, signaling a positive economic outlook for facilities. In Canada, transplant limitations sustained demand by keeping a significant chronic hemodialysis population in long-term treatment.

Europe remained a key player in the hemodialysis catheters market in 2025, driven by an aging population and a significant CKD burden. As of January 2025, 21.6% of the EU population was aged 65 or older, supporting consistent demand for renal replacement therapies. A CKD analysis reported a median prevalence of 12.8% in Eastern and Central Europe, highlighting the region's renal disease challenges. Germany, the UK, and France led the market, though the adoption of premium-coated catheters varied due to differing reimbursement and procurement policies.

Asia-Pacific is projected to grow at a 6.26% CAGR through 2031, making it the fastest-growing regional segment in the hemodialysis catheters market. China and India are driving this growth by expanding dialysis capacity to address unmet renal care needs. In 2025, China's dialysis population reached 1.34 million, with domestic producers increasing their role in local supply, supporting volume growth and reducing import dependency. India's Pradhan Mantri National Dialysis Programme, with over 1,200 district hospital centers by 2025, enhanced treatment access and increased demand for reliable catheter procurement. Japan remains clinically advanced with stringent standards, while South America and the Middle East and Africa are expanding through public renal care programs and selective private network growth.

- Amecath Medical Technologies

- AngioDynamics

- Asahi Kasei

- B. Braun

- Baxter

- Beckton Dickinson

- Cook Group

- Fresenius Medical Care AG and Co. KGaA

- JMS Co., Ltd.

- Joline GmbH and Co. KG

- Medical Components, Inc.

- Medtronic

- Merit Medical Systems

- Mozarc Medical Holding LLC

- Nikkiso Co., Ltd.

- Nipro

- Poly Medicure Ltd.

- Teleflex

- Toray Medical Co., Ltd.

- Vygon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Kidney Disease and End-Stage Renal Disease Burden

- 4.2.2 Growing Reliance on Catheter-Based Initiation of Hemodialysis

- 4.2.3 Expansion of Dialysis Capacity in Emerging Markets

- 4.2.4 Rising Demand for Antimicrobial and Biocompatible Catheters

- 4.2.5 Increased Home Hemodialysis Adoption and Portable Access Needs

- 4.2.6 Greater Use of Catheter Kits and Procedure-Efficiency Solutions

- 4.3 Market Restraints

- 4.3.1 Catheter-Related Bloodstream Infections and Thrombosis Risk

- 4.3.2 Shift Toward Arteriovenous Fistula First Pathways

- 4.3.3 Shortage of Skilled Vascular Access Operators

- 4.3.4 Hospital Budget Pressure and Reimbursement Sensitivity

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Product Type

- 5.1.1 Tunneled Hemodialysis Catheters

- 5.1.2 Cuffed Tunneled Catheters

- 5.1.3 Non-Cuffed Tunneled Catheters

- 5.1.4 Non-Tunneled Hemodialysis Catheters

- 5.1.5 Single Lumen Non-Tunneled Catheters

- 5.1.6 Double Lumen Non-Tunneled Catheters

- 5.1.7 Triple Lumen Non-Tunneled Catheters

- 5.2 By Material

- 5.2.1 Polyurethane

- 5.2.2 Silicone

- 5.2.3 Composite and Other Polymer Materials

- 5.3 By Tip Configuration

- 5.3.1 Step-Tip Catheters

- 5.3.2 Split-Tip Catheters

- 5.3.3 Symmetric Catheters

- 5.3.4 Pre-Curved Catheters

- 5.4 By Application

- 5.4.1 Chronic Hemodialysis

- 5.4.2 Acute Hemodialysis

- 5.4.3 Home Hemodialysis

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Dialysis Centers

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Home Care Settings

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Amecath Medical Technologies

- 6.3.2 AngioDynamics, Inc.

- 6.3.3 Asahi Kasei Medical Co., Ltd.

- 6.3.4 B. Braun SE

- 6.3.5 Baxter International Inc.

- 6.3.6 Becton, Dickinson and Company

- 6.3.7 Cook Medical, Inc.

- 6.3.8 Fresenius Medical Care AG and Co. KGaA

- 6.3.9 JMS Co., Ltd.

- 6.3.10 Joline GmbH and Co. KG

- 6.3.11 Medical Components, Inc.

- 6.3.12 Medtronic plc

- 6.3.13 Merit Medical Systems, Inc.

- 6.3.14 Mozarc Medical Holding LLC

- 6.3.15 Nikkiso Co., Ltd.

- 6.3.16 Nipro Corporation

- 6.3.17 Poly Medicure Ltd.

- 6.3.18 Teleflex Incorporated

- 6.3.19 Toray Medical Co., Ltd.

- 6.3.20 Vygon SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment