PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073090

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073090

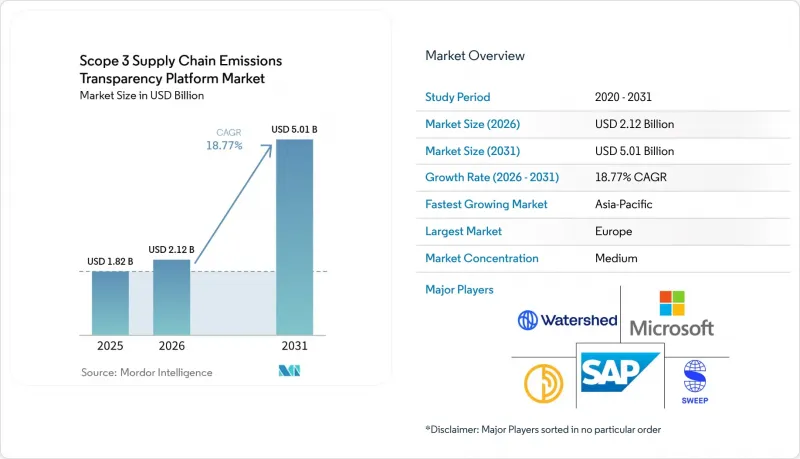

Scope 3 Supply Chain Emissions Transparency Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the scope 3 supply chain emissions transparency platform market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 2.12 billion in 2026 to reach USD 5.01 billion by 2031, at a CAGR of 18.77% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment (Cloud, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Supplier Carbon Emissions Tracking, and More), End-Use Industry (IT and Telecom, Energy and Utilities, BFSI, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Scope 3 Supply Chain Emissions Transparency Platform Market Trends and Insights

Expanding Regulatory Disclosure Mandates

Mandatory disclosure rules are now a direct buying trigger for the scope 3 supply chain emissions transparency platform market because large companies need systems that can gather, structure, and document value chain data in a repeatable way. The Corporate Sustainability Reporting Directive keeps Scope 3 reporting at the center of climate disclosure for large companies, and the Omnibus I changes still preserve the need to collect value chain information within a defined reporting framework. This matters because the reporting challenge is no longer limited to calculating emissions once a year; it now involves maintaining evidence trails that can withstand assurance requirements and internal review. The European Commission also clarified how the value chain cap should be applied, underscoring the need for platforms that can collect the right supplier data without crossing the new legal boundaries imposed on reporting companies. As a result, the scope 3 supply chain emissions transparency platform market is benefiting from a compliance cycle that favors systems with strong supplier workflows, traceable calculations, and documentation controls.

Shift From Spend-Based Estimates to Supplier-Specific Data

The scope 3 supply chain emissions transparency platform market is also advancing, as companies are under pressure to replace broad, spend-based proxies with supplier-specific information wherever possible. MIT Sloan and CSCMP found that supplier data availability was the single largest obstacle to accurate Scope 3 measurement for many organizations, which explains why buyers are looking for platforms that make supplier outreach and data exchange easier. This shift changes the product requirement because enterprises now need supplier portals, product carbon footprint workflows, and structured templates rather than standalone calculation files. WBCSD PACT Methodology v3.0 supports this move by providing trading partners with a common basis for exchanging product carbon footprint data across systems, thereby making automated data transfer at scale more practical. Once buyers start requesting primary data within normal sourcing and reporting cycles, suppliers that can respond in a standard format are easier to retain and compare across product categories. That is why the scope 3 supply chain emissions transparency platform market is expanding beyond carbon accounting alone to include supplier participation and product-level data readiness.

Poor Multi-Tier Data Quality and Traceability

Poor data quality across multi-tier supply chains remains the largest operational restraint on the scope 3 supply chain emissions transparency platform market because companies still struggle to move beyond direct supplier relationships. SBTi noted that supplier response rates in supply chain disclosure programs often remain limited without active engagement, leading to a decline in the availability of primary data as reporting companies move deeper into the supply chain. A 2026 academic paper on multi-tier Scope 3 accounting also noted that the GHG Protocol provides conceptual guidance but does not prescribe algorithms for tracing complex upstream relationships, leaving vendors to develop their own methods. That weakens comparability because two platforms may handle supplier gaps, shared inputs, and circular dependencies differently. The commercial effect is that buyers want systems that can mix primary data, partial estimates, and fallback methods without breaking reporting consistency. Even when demand stays strong, the scope 3 supply chain emissions transparency platform market cannot fully convert that demand into usable deployments unless supplier participation and traceability improve.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Factor Matching and Anomaly Detection

- Procurement Integration Into ERP And P2P Workflows

- High Change Management and Implementation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms accounted for 68.74% of the scope 3 supply chain emissions transparency platform market in 2025, confirming that buyers still prioritize core systems over adjacent support services. The reason is straightforward: enterprises need a single platform to handle emissions calculation, supplier communication, reporting logic, and audit evidence in a connected way. European reporting requirements have made that integrated model even more important, as companies need repeatable workflows rather than one-time manual exercises. SAP and IBM product direction also support this pattern because both companies are expanding features that tie carbon workflows directly to operational and financial systems. That makes software the anchor layer of the scope 3 supply chain emissions transparency platform market, even when service demand remains healthy.

Services still matter because most deployments need configuration, supplier onboarding, data checks, and reporting support before a platform can work well in live disclosure cycles. This part of the market grows as projects become more embedded in procurement and finance processes rather than staying inside stand-alone sustainability teams. The need for services also rises when companies try to align supplier-specific data exchange with WBCSD PACT methods and product carbon footprint requirements. In practice, service demand tends to follow software depth, as more capable platforms often require more setup across internal systems and supplier networks. This means the scope 3 supply chain emissions transparency platform industry is not splitting into separate software and service lanes; it is moving toward bundled delivery models where the service layer helps software become usable at scale.

Cloud accounted for 65.12% of revenue in 2025, reflecting that supplier data collection often spans multiple facilities, partners, and geographies simultaneously. The cloud model fits the scope 3 supply chain emissions transparency platform market because supplier portals, workflow approvals, and cross-company data exchange work better when they are accessible through shared interfaces. WBCSD PACT technical development reinforces this point because standardized product carbon footprint exchange is designed to support system-to-system transfers rather than isolated local files. That interoperability matters more as enterprises request product-level emissions data across categories and geographies. The cloud model also supports faster template changes when disclosure rules or customer requests evolve.

Hybrid is projected to grow at a 18.92% CAGR through 2031 because many large companies still keep core ERP environments and sensitive data controls inside internal systems while using external interfaces for supplier engagement. SAP's updates show why this design is attractive, since carbon calculations can sit close to transaction records while still drawing on wider factor libraries and connected workflows. Hybrid, therefore, addresses a common enterprise concern in the scope 3 supply chain emissions transparency platform market: how to enable supplier collaboration without weakening data governance. On-premises systems still hold a place in sensitive environments, but they are less aligned with large-scale supplier participation and frequent data exchange. For that reason, the market is not moving away from cloud; it is expanding toward more flexible deployment combinations.

Complete Report Scope:

- By Component

- Software Platforms

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By Transparency Function

- Supplier Emissions Data Collection

- Data Validation and Verification

- Product Carbon Footprint Transparency

- Supply Chain Traceability

- Reporting and Disclosure

- Supplier Collaboration

- By End-Use Industry

- Manufacturing

- Retail and E-Commerce

- Transportation and Logistics

- Energy and Utilities

- IT and Telecom

- BFSI

- Construction and Infrastructure

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe held the leading position in the scope 3 supply chain emissions transparency platform market in 2025 because the region combines formal disclosure requirements with dense cross-border supplier relationships. The Corporate Sustainability Reporting Directive has kept Scope 3 disclosures in the reporting framework for large companies, which supports sustained software demand rather than a one-off compliance rush. Clarification on the value chain cap also matters because it shapes how companies request data from suppliers, thereby affecting platform workflow design. Europe is also important because product carbon footprint exchange and digital product data are advancing in parallel with corporate reporting needs. That combination keeps the region at the center of both compliance demand and product feature development for the market.

Asia-Pacific is projected to be the fastest-growing region in the scope 3 supply chain emissions transparency platform market through 2031, supported by export-led supply chains that increasingly need product and supplier emissions data to work with global buyers. Even where local rules vary, manufacturers in the region are still affected by the reporting expectations and product data requests coming from multinational customers. Cross-border relationships gain a practical basis for data exchange, which is important in supplier-heavy manufacturing corridors. Expansion across hundreds of consumer goods categories also reflects why Asia-Pacific matters, because many regional suppliers serve brands that need broad product-level emissions coverage. Supplier network approaches add to this dynamic by making it easier for large buyers to collect standardized information from distributed suppliers across sectors and locations. The regional growth story, therefore, comes from supply chain position as much as from local reporting rules.

North America remains one of the largest demand centers because multinational companies in the region often need systems that can serve both domestic sustainability programs and international reporting obligations. Enterprise solutions support this demand with products that connect carbon workflows to finance and procurement data, which matches the needs of large North American buyers. South America, the Middle East, and Africa are earlier-stage regions in the scope 3 supply chain emissions transparency platform market, but they remain relevant where exporters, industrial groups, and supplier networks are being pulled into multinational data requests. Across all regions, adoption still depends less on local branding and more on whether platforms can collect supplier data, integrate operational records, and support product-level traceability with enough consistency to satisfy large enterprise buyers.

- Persefoni AI Inc.

- Watershed Technology, Inc.

- Sweep SAS

- Normative AB

- Emitwise Limited

- CarbonChain Ltd

- Greenly SAS

- SINAI Technologies, Inc.

- Climatiq GmbH

- Plan A Software GmbH

- Carbon Analytics Limited

- Dcycle Sustainability Solutions, S.L.

- Novata, Inc.

- EcoVadis SAS

- Sphera Solutions, Inc.

- IBM Corporation

- SAP SE

- Microsoft Corporation

- Salesforce, Inc.

- Diligent Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Regulatory Disclosure Mandates

- 4.2.2 Shift From Spend-Based Estimates To Supplier-Specific Data

- 4.2.3 Procurement Integration Into ERP And P2P Workflows

- 4.2.4 AI Enabled Factor Matching And Anomaly Detection

- 4.2.5 Supplier Engagement And Capacity Building Workflows

- 4.2.6 Product And SKU Level Carbon Traceability Demand

- 4.3 Market Restraints

- 4.3.1 Poor Multi-Tier Data Quality And Traceability

- 4.3.2 High Change Management And Implementation Cost

- 4.3.3 Supplier Privacy, NDAs, And Antitrust Friction

- 4.3.4 Methodology Fragmentation Across Frameworks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Medium Enterprises

- 5.4 By Transparency Function

- 5.4.1 Supplier Emissions Data Collection

- 5.4.2 Data Validation and Verification

- 5.4.3 Product Carbon Footprint Transparency

- 5.4.4 Supply Chain Traceability

- 5.4.5 Reporting and Disclosure

- 5.4.6 Supplier Collaboration

- 5.5 By End-Use Industry

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-Commerce

- 5.5.3 Transportation and Logistics

- 5.5.4 Energy and Utilities

- 5.5.5 IT and Telecom

- 5.5.6 BFSI

- 5.5.7 Construction and Infrastructure

- 5.5.8 Government and Public Sector

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Netherlands

- 5.6.3.7 Russia

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Indonesia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Persefoni AI Inc.

- 6.4.2 Watershed Technology, Inc.

- 6.4.3 Sweep SAS

- 6.4.4 Normative AB

- 6.4.5 Emitwise Limited

- 6.4.6 CarbonChain Ltd

- 6.4.7 Greenly SAS

- 6.4.8 SINAI Technologies, Inc.

- 6.4.9 Climatiq GmbH

- 6.4.10 Plan A Software GmbH

- 6.4.11 Carbon Analytics Limited

- 6.4.12 Dcycle Sustainability Solutions, S.L.

- 6.4.13 Novata, Inc.

- 6.4.14 EcoVadis SAS

- 6.4.15 Sphera Solutions, Inc.

- 6.4.16 IBM Corporation

- 6.4.17 SAP SE

- 6.4.18 Microsoft Corporation

- 6.4.19 Salesforce, Inc.

- 6.4.20 Diligent Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Assessment