PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073114

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073114

Brake Lathe Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

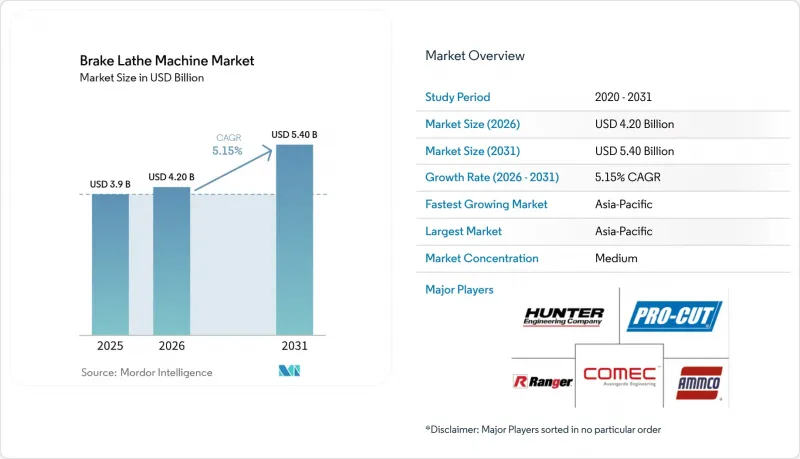

According to Mordor Intelligence, the brake lathe machine market size is projected to expand from USD 3.9 billion in 2025 and USD 4.20 billion in 2026 to USD 5.40 billion by 2031, registering a CAGR of 5.15% between 2026 to 2031.

This report is Segmented by Machine Type (On-Car Brake Lathe Machines, Off-Car (Bench) Brake Lathe Machines), by Automation Type (Manual Brake Lathe Machines, Semi-Automatic Brake Lathe Machines, Fully Automatic/CNC Brake Lathe Machines), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Brake Lathe Machine Market Trends and Insights

Expansion of Automotive Aftermarket Service Networks in Asia-Pacific

The brake lathe machine market is gaining direct support from the build-out of organized aftermarket service networks across Asia-Pacific. Japan continues to provide a stable service floor because its shaken inspection regime requires brake system checks every 24 months for most passenger vehicles. That requirement applies across a very large national vehicle base. China is also moving toward a more professional passenger-vehicle aftermarket, with industry participants describing 2025 as a turning point for broader development and stronger multi-brand service chain activity. As chains expand across cities and store formats, brake maintenance becomes less dependent on ad hoc workshop decisions and more tied to repeatable service protocols. That shift matters for the brake lathe machine market because standardized service menus make equipment purchases easier to justify at the network level. Bosch's 2025 flagship Bosch Car Service opening in Indonesia also showed that large aftermarket brands were still investing in structured service footprints across Southeast Asia.

Growth of Fleet Maintenance and Commercial Vehicle Servicing

The brake lathe machine market also benefits from the recurring maintenance logic of fleet and commercial vehicle operations. The global medium- and heavy-duty truck fleet exceeded 85 million vehicles at the end of 2024, keeping the installed service base large even before replacement cycles are considered. In the United States, annual brake inspections are mandatory for commercial motor vehicles, and carriers must use brake inspectors who meet minimum qualification standards. Brake Safety Week in 2025 found that 15.1% of 15,175 inspected commercial vehicles across 52 North American jurisdictions were placed out of service for brake-related violations, while Brake Safety Day found an 8.7% out-of-service rate among 4,569 inspected vehicles. Those failure rates show that brake remediation remains a persistent operating need rather than a discretionary event. For the brake lathe machine market, that means fleet depots and third-party maintenance sites continue to see resurfacing as a practical first step before moving to higher-cost replacement.

Growing EV Adoption Reducing Brake Wear Frequency

The brake lathe market faces a structural challenge from battery-electric vehicles, as regenerative braking reduces reliance on friction brakes. A 2025 study by EIT Urban Mobility and Transport for London found that BEVs cut brake dust emissions by 83%, plug-in hybrids by 66%, and hybrid vehicles by 10% to 48% in the studied cities. Those reductions matter because they indicate fewer friction-brake events over the vehicle's service life. As electrification increases, rotor and pad service intervals can lengthen, gradually narrowing the pool of resurfacing jobs that justify owning a brake lathe. This does not remove near-term demand from the brake lathe machine market, because the global vehicle base still includes a large internal combustion and hybrid population. Even so, the long-run direction is clear, since a larger EV parc will reduce the recurring brake wear that has historically supported resurfacing volumes.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advancements in CNC and Automatic Brake Lathes

- Rising Brake Rotor Replacement Costs Driving Resurfacing Adoption

- Shift Toward Rotor Replacement Instead of Resurfacing in Low-Cost Passenger Vehicles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Off-car brake lathe machines held 56.43% of the brake lathe market share in 2026, reflecting their long-established role in independent workshops and multi-brand service chains. Their broad fitment range supports work on many rotor and drum sizes, making them the default choice where workshops serve mixed vehicle populations rather than a narrow brand portfolio. This installed-base advantage still matters in the brake lathe machine market because bench units have lower acquisition costs, long service lives, and a well-understood operating model. On-car machines remain smaller by installed share, but the brake lathe machine market in that segment is forecast to grow at a 6.54% CAGR through 2031. That growth rate is supported by the technical benefit of machining the rotor on the vehicle hub, which helps correct lateral runout linked to hub and bearing geometry rather than relying only on adapters and setup accuracy.

The segment mix shows that the brake lathe machine market is moving from wide first-time adoption toward more selective replacement and upgrade demand. Historical growth from 2019 to 2025 ran ahead of the 2025 to 2031 forecast, indicating a more mature phase in which the replacement of aging manual equipment is becoming more important than net-new site creation. Within the off-car segment, high-throughput fleet depots still value durability and flexibility, especially when they service multiple vehicle classes in a single facility. Within the on-car segment, rising attention to pedal pulsation, noise, vibration, and harshness is pushing service operators toward equipment that can deliver better in-vehicle correction. The brake lathe machine industry is therefore dividing more clearly between legacy bench demand that remains broad and a higher-precision niche that is growing faster in organized service environments.

Complete Report Scope:

- By Machine Type

- On-Car Brake Lathe Machines

- Off-Car (Bench) Brake Lathe Machines

- By Automation Type

- Manual Brake Lathe Machines

- Semi-Automatic Brake Lathe Machines

- Fully Automatic/CNC Brake Lathe Machines

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Qatar

- South Africa

- Egypt

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

Asia-Pacific held 35.67% of the brake lathe machine market share in 2026 and is also the fastest-growing region, with 6.8% CAGR projected through 2031. The regional story is not uniform, as some markets are expanding on the back of organized service chain growth, while others are beginning to feel the long-term effects of higher EV penetration on friction-brake service demand. Japan remains structurally supportive because its mandatory shaken regime requires brake inspection at regular intervals across a very large vehicle population. India, Southeast Asia, and the Philippines offer the clearest runway for the brake lathe machine market because service formalization is advancing faster than the installed base of precision brake equipment.

North America maintained the dominant revenue geography through 2025 and continues to represent the largest single market cluster in 2026, driven by its large commercial vehicle service base and strict brake inspection framework. The United States and Canada support a dense network of fleet depots, independent repair centers, and organized service operators that create repeat equipment demand across both replacement and upgrade cycles. CVSA's 2025 inspection data still showed meaningful non-compliance levels, including 15.1% of inspected commercial vehicles being placed out of service during Brake Safety Week, which confirmed that brake remediation remained a recurring operational requirement. Europe held the second-largest share of the brake lathe market, driven by procurement demand in Germany, the United Kingdom, and France. The region combines mature installed bases with a technology shift toward lower-emission, more durable brake disc solutions, gradually changing the resurfacing opportunity in passenger vehicles.

South America remains a moderate but growing part of the brake lathe market, with Brazil leading regional demand through its commercial trucking base and investment in logistics infrastructure. The region's outlook is positive, but capital spending on workshop equipment remains tied to economic conditions and currency pressures. The Middle East and Africa present a mixed picture: Gulf markets are active in fleet management, while African demand remains concentrated in selected countries with deeper service networks. Manual and entry-level systems remain most relevant across much of MEA. At the same time, mining, construction, and fuel retail fleets are more likely to procure heavier-duty configurations for sustained commercial use.

- Hunter Engineering Company

- AMMCO Tools

- Comec Srl

- Pro-Cut International LLC

- Ranger Products

- John Bean Technologies Corporation

- Snap-on Incorporated

- Rotary Lift

- CEMB S.p.A.

- AUTOPSTENHOJ GmbH

- Mad Equipment

- Arcen Equipment

- Precision Brake Company

- KWIK-WAY Products Inc.

- COMEC USA

- ACDelco Tools

- Bosch Automotive Service Solutions

- Launch Tech Co. Ltd.

- Sunbright Equipment

- Xiangsheng Machine Tools Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Brake Rotor Replacement Costs Driving Resurfacing Adoption

- 4.2.2 Expansion of Automotive Aftermarket Service Networks in Asia-Pacific

- 4.2.3 Growth of Fleet Maintenance and Commercial Vehicle Servicing

- 4.2.4 Increasing Adoption of On-Car Brake Lathes for NVH Reduction

- 4.2.5 Technological Advancements in CNC and Automatic Brake Lathes

- 4.2.6 Stricter Vehicle Safety Inspection Standards Supporting Brake Maintenance

- 4.3 Market Restraints

- 4.3.1 Shift Toward Rotor Replacement Instead of Resurfacing in Low-Cost Passenger Vehicles

- 4.3.2 Increasing Use of Lightweight and Coated Brake Rotors Limiting Machining Cycles

- 4.3.3 High Initial Investment for CNC and Heavy-Duty Brake Lathes

- 4.3.4 Growing EV Adoption Reducing Brake Wear Frequency

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts

- 5.1 By Machine Type

- 5.1.1 On-Car Brake Lathe Machines

- 5.1.2 Off-Car (Bench) Brake Lathe Machines

- 5.2 By Automation Type

- 5.2.1 Manual Brake Lathe Machines

- 5.2.2 Semi-Automatic Brake Lathe Machines

- 5.2.3 Fully Automatic/CNC Brake Lathe Machines

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Chile

- 5.3.2.4 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.3.3.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.3.3.9 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines)

- 5.3.4.7 Rest of Asia-Pacific

- 5.3.5 Middle East & Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Turkey

- 5.3.5.4 Qatar

- 5.3.5.5 South Africa

- 5.3.5.6 Egypt

- 5.3.5.7 Nigeria

- 5.3.5.8 Rest of Middle East & Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 6.4.1 Hunter Engineering Company

- 6.4.2 AMMCO Tools

- 6.4.3 Comec Srl

- 6.4.4 Pro-Cut International LLC

- 6.4.5 Ranger Products

- 6.4.6 John Bean Technologies Corporation

- 6.4.7 Snap-on Incorporated

- 6.4.8 Rotary Lift

- 6.4.9 CEMB S.p.A.

- 6.4.10 AUTOPSTENHOJ GmbH

- 6.4.11 Mad Equipment

- 6.4.12 Arcen Equipment

- 6.4.13 Precision Brake Company

- 6.4.14 KWIK-WAY Products Inc.

- 6.4.15 COMEC USA

- 6.4.16 ACDelco Tools

- 6.4.17 Bosch Automotive Service Solutions

- 6.4.18 Launch Tech Co. Ltd.

- 6.4.19 Sunbright Equipment

- 6.4.20 Xiangsheng Machine Tools Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment