PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073121

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073121

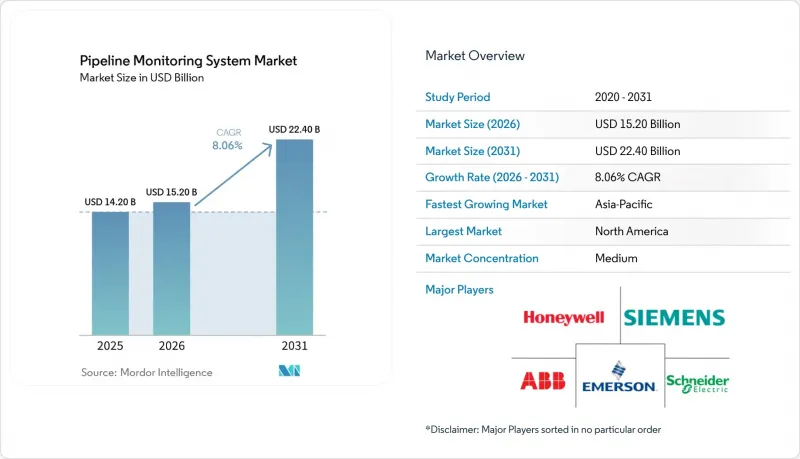

Pipeline Monitoring System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the pipeline monitoring system market size is projected to be USD 14.20 billion in 2025, USD 15.20 billion in 2026, and reach USD 22.40 billion by 2031, growing at a CAGR of 8.06% from 2026 to 2031.

This report is Segmented by Technology (Fiber Optic, Acoustic, and More), by Component (Hardware, Software, Services), by Application (Leak Detection, Operational Monitoring, and More), by Pipeline Type (Oil, Gas, and More), by Deployment (Onshore, Offshore), by Geography (North America, Asia-Pacific, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Pipeline Monitoring System Market Trends and Insights

Increasing Crude Oil and Natural Gas Pipeline Expansion Projects Globally

Pipeline expansion is the clearest near-term demand driver for the pipeline monitoring system market because every new line requires instrumentation from commissioning onward. The United States Energy Information Administration stated in 2026 that 12 new or expanded United States natural gas pipeline projects were scheduled for completion this year, adding close to 18 Bcf/d of capacity, the largest annual addition since 2008. The INGAA Foundation also projected in its 2025 midstream infrastructure report that more than USD 1 trillion in total midstream capital investment will be required through 2052, including at least 37,000 additional miles of United States gas transmission pipelines. In Canada, Enbridge received federal approval in April 2026 for the USD 4 billion Sunrise Expansion Program on the West Coast pipeline system, with construction set to begin in July 2026. The pipeline monitoring system market is also gaining a broader demand base because intrastate pipeline additions accounted for close to 65% of United States capacity added in 2025, indicating that monitoring choices are shaped by a mix of federal rules, state oversight, and operator judgment rather than a single regulatory path.

Increasing Integration of AI, IoT, and Predictive Analytics in Pipeline Operations

The main technology-led growth path in the pipeline monitoring system market is the shift from periodic inspection toward condition-based maintenance supported by AI and connected sensors. A 2026 peer-reviewed study in npj materials degradation described machine learning applied to multi-sensor in-line inspection data as a key step in turning high data volumes into predictive maintenance actions and noted that signal complexity, rather than hardware limitations, is now the main challenge. The Society of Petroleum Engineers also highlighted in 2025 that AI applications for offshore pipeline integrity are enabling real-time condition monitoring in locations where operators once relied mainly on periodic inspection runs. In the pipeline monitoring system market, this is shifting value toward software layers that can score anomalies, support digital twins, and shorten the detection gap between inspections. It is also changing procurement behavior because vendors with stronger data models and longer operating histories are in a better position than firms that sell hardware alone. As a result, the pipeline monitoring system market is seeing a gradual shift toward recurring software and analytics revenue.

High Installation and Integration Costs of Advanced Monitoring Systems

Capital intensity remains the clearest adoption barrier for the pipeline monitoring system market, especially where operators work under tight budgets. Distributed fiber-optic monitoring for long-haul pipelines requires high-grade cable, interrogation units, and integration with existing SCADA systems, and costs rise further in difficult terrain or subsea routes. For mid-sized operators and many state-owned entities in South America and Sub-Saharan Africa, that cost burden still favors legacy periodic inspection over fully digital monitoring. The challenge is greater on live networks because upgrades often require replacing remote terminal units, software licensing, validation work, and long commissioning cycles. The pipeline monitoring system market is gaining some relief as sensor prices fall and cloud analytics reduce the need for on-premises infrastructure. Still, that improvement is uneven across regions and does not remove the near-term funding hurdle. As a result, lifecycle savings are often acknowledged before purchase, but not always enough to accelerate final approvals.

Other drivers and restraints analyzed in the detailed report include:

- Rising Incidents of Pipeline Leaks and Corrosion Failures

- Stringent Environmental and Pipeline Safety Regulations

- Cybersecurity Risks Associated with Connected Pipeline Monitoring Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acoustic and ultrasonic methods accounted for 25.2% of the pipeline monitoring system market share in 2025, maintaining this technology group in the leading position. That leadership reflects broad use across leak detection and corrosion assessment, as well as compatibility across onshore and offshore pipeline configurations. Acoustic emission systems capture stress-wave signals from crack growth and localized leaks, making them useful for passive, continuous surveillance. Ultrasonic testing, including through-wall and guided-wave variants, remains important because it can quantify wall loss with very high resolution on liquid-filled lines.

The pipeline monitoring system market is now seeing faster growth from Smart PIG solutions, as operators need more frequent and more detailed inline inspection on high-consequence transmission lines. Smart PIG platforms are becoming more capable as vendors combine magnetic flux leakage, ultrasonic caliper tools, and inertial measurement systems into a single inspection run. A 2026 peer-reviewed review in npj Materials Degradation stated that machine learning-assisted signal processing is helping convert dense in-line inspection data into predictive maintenance actions, thereby increasing the practical value of these tools. Fiber-optic monitoring is also gaining ground in the pipeline monitoring system market, especially on long-haul gas networks, where distributed acoustic sensing can improve detectability in sections that are difficult to monitor with external installation methods alone. Magnetic flux leakage remains the most widely deployed in-line inspection method in many operating environments, while lower-field variants are attracting attention for defects that conventional high-field tools do not isolate as well. International framework standards such as ISO 13623 and DNV-ST-F101 continue to shape technology selection, especially where domestic rules are still evolving.

Hardware accounted for the largest share of the pipeline monitoring system market in 2025, as every monitored pipeline still requires physical field devices. That includes control systems, remote terminal units, flow computers, pressure transducers, and acoustic or ultrasonic sensor arrays deployed over long distances. New-build pipelines continue to drive incremental hardware demand because instrumentation is required from the first day of operation. Replacement demand is also rising as legacy devices no longer meet updated leak-detection and performance standards.

Software is the fastest-growing component in the pipeline monitoring system market and is projected to grow at a 10.3% CAGR from 2026 to 2031. This growth is tied to cloud-hosted SCADA environments, analytics subscriptions, and digital twin tools that process multi-sensor data in near real time. As sensor hardware becomes more standardized, commercial value is shifting toward interpretation layers that convert field data into alarms, maintenance priorities, and operational decisions. That change is also compressing hardware pricing power in parts of the pipeline monitoring system industry where basic field instrumentation is becoming less differentiated. Services remain an important revenue layer because commissioning, calibration, managed inspection, and long-term maintenance support are still difficult for many operators to manage internally. Vendors with stronger software libraries and longer data histories, therefore, have a clear edge over hardware-only challengers.

Complete Report Scope:

- By Technology

- Fiber Optic Monitoring

- Acoustic Monitoring

- Ultrasonic Monitoring

- Magnetic Flux Leakage (MFL)

- Smart PIG Monitoring

- Others

- By Component

- Hardware

- Software

- Services

- By Application

- Leak Detection

- Corrosion & Integrity Monitoring

- Operational Monitoring

- Real-Time Data Analytics

- By Pipeline Type

- Oil Pipelines

- Gas Pipelines

- Water & Wastewater Pipelines

- Chemical Pipelines

- By Deployment

- Onshore

- Offshore

Geography Analysis

North America held a 28.3% share of the pipeline monitoring system market in 2025, maintaining its leading regional position. The region benefits from a very large regulated pipeline base, strong federal oversight, and a new gas capacity buildout cycle. In the United States, the EIA said 12 natural gas pipeline projects were scheduled for completion in 2026, adding close to 18 Bcf/d of capacity, making this the largest annual buildout since 2008. The PHMSA leak detection rule, finalized in January 2025, and the TSA Security Directive Pipeline-2021-02F, effective in May 2025, have also tightened compliance expectations for gas and hazardous liquid operators. Canada adds to this base through Enbridge's Sunrise Expansion approval in April 2026, while Mexico's growing import pipeline network broadens the regional opportunity beyond long-established operators.

Asia-Pacific is the fastest-growing regional market for pipeline monitoring systems, with a 10.2% CAGR forecast through 2031. India remains central to that growth because the Jagdishpur-Haldia-Bokaro-Dhamra pipeline is targeting completion in September 2026, while other large crude and gas corridor projects are also moving toward commissioning. China is expanding transmission capacity through a new fourth-line contract on the Central Asia-China system in 2026, while domestic gas networks continue to scale to meet industrial and residential demand. Southeast Asia is also becoming a more visible source of monitoring demand as Indonesia, Vietnam, and Malaysia expand offshore gas infrastructure for domestic power and industrial use. The pipeline monitoring system market in this region, therefore, benefits from both onshore transmission growth and offshore surveillance needs.

Europe remains a strategically important market for pipeline monitoring systems, supported by an increasingly stringent regulatory framework and ongoing offshore infrastructure development. The EU Methane Regulation 2024/1787 has strengthened demand for advanced leak detection and repair solutions by establishing mandatory compliance requirements across oil and gas infrastructure, while Romania's Neptun Deep project is expected to generate additional demand for high-specification monitoring systems during pipeline construction and subsequent operations. In the Middle East and Africa, large pipeline networks, expanding energy infrastructure, and high consequence exposure are driving greater adoption of continuous digital corrosion monitoring and integrity management solutions. The region also offers long-term growth potential as increasing upstream oil and gas investment is expected to support new onshore and offshore pipeline developments, creating sustained demand for monitoring technologies throughout the asset lifecycle.

- Honeywell International Inc.

- Siemens AG

- ABB Ltd.

- Emerson Electric Co.

- Schneider Electric SE

- Yokogawa Electric Corporation

- Huawei Technologies Co. Ltd.

- PSI Software SE

- KROHNE Group

- Pure Technologies Ltd.

- Pentair plc

- Orbcomm Inc.

- Synodon Inc.

- Atmos International

- TTK Leak Detection

- Future Fibre Technologies

- Perma-Pipe International Holdings Inc.

- ClampOn AS

- Baker Hughes Company

- ROSEN Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Crude Oil and Natural Gas Pipeline Expansion Projects Globally

- 4.2.2 Rising Incidents of Pipeline Leaks and Corrosion Failures

- 4.2.3 Growing Adoption of Fiber Optic Monitoring in Long-Distance Pipelines

- 4.2.4 Stringent Environmental and Pipeline Safety Regulations

- 4.2.5 Increasing Integration of AI, IoT, and Predictive Analytics in Pipeline Operations

- 4.2.6 Rising Offshore Pipeline Installations and Deepwater Energy Projects

- 4.3 Market Restraints

- 4.3.1 High Installation and Integration Costs of Advanced Monitoring Systems

- 4.3.2 Operational Challenges in Retrofitting Aging Pipeline Infrastructure

- 4.3.3 Limited Monitoring Efficiency in Remote and Harsh Environments

- 4.3.4 Cybersecurity Risks Associated with Connected Pipeline Monitoring Networks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Impact of Geopolitical Events on the market

5 Market Size & Growth Forecasts (Value in USD & Volume in Tons)

- 5.1 By Technology

- 5.1.1 Fiber Optic Monitoring

- 5.1.2 Acoustic Monitoring

- 5.1.3 Ultrasonic Monitoring

- 5.1.4 Magnetic Flux Leakage (MFL)

- 5.1.5 Smart PIG Monitoring

- 5.1.6 Others

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Leak Detection

- 5.3.2 Corrosion & Integrity Monitoring

- 5.3.3 Operational Monitoring

- 5.3.4 Real-Time Data Analytics

- 5.4 By Pipeline Type

- 5.4.1 Oil Pipelines

- 5.4.2 Gas Pipelines

- 5.4.3 Water & Wastewater Pipelines

- 5.4.4 Chemical Pipelines

- 5.5 By Deployment

- 5.5.1 Onshore

- 5.5.2 Offshore

6 By Geography

- 6.1 North America

- 6.1.1 United States

- 6.1.2 Canada

- 6.1.3 Mexico

- 6.2 South America

- 6.2.1 Brazil

- 6.2.2 Argentina

- 6.2.3 Chile

- 6.2.4 Rest of South America

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 United Kingdom

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.3.6 Russia

- 6.3.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 6.3.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 6.3.9 Rest of Europe

- 6.4 Asia-Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.4.6 Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, Philippines)

- 6.4.7 Rest of Asia-Pacific

- 6.5 Middle East & Africa

- 6.5.1 United Arab Emirates

- 6.5.2 Saudi Arabia

- 6.5.3 Turkey

- 6.5.4 Qatar

- 6.5.5 South Africa

- 6.5.6 Egypt

- 6.5.7 Nigeria

- 6.5.8 Rest of Middle East & Africa

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)}

- 7.4.1 Honeywell International Inc.

- 7.4.2 Siemens AG

- 7.4.3 ABB Ltd.

- 7.4.4 Emerson Electric Co.

- 7.4.5 Schneider Electric SE

- 7.4.6 Yokogawa Electric Corporation

- 7.4.7 Huawei Technologies Co. Ltd.

- 7.4.8 PSI Software SE

- 7.4.9 KROHNE Group

- 7.4.10 Pure Technologies Ltd.

- 7.4.11 Pentair plc

- 7.4.12 Orbcomm Inc.

- 7.4.13 Synodon Inc.

- 7.4.14 Atmos International

- 7.4.15 TTK Leak Detection

- 7.4.16 Future Fibre Technologies

- 7.4.17 Perma-Pipe International Holdings Inc.

- 7.4.18 ClampOn AS

- 7.4.19 Baker Hughes Company

- 7.4.20 ROSEN Group

8 Market Opportunities & Future Outlook

- 8.1 White-Space & Unmet-Need Assessment