PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073239

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073239

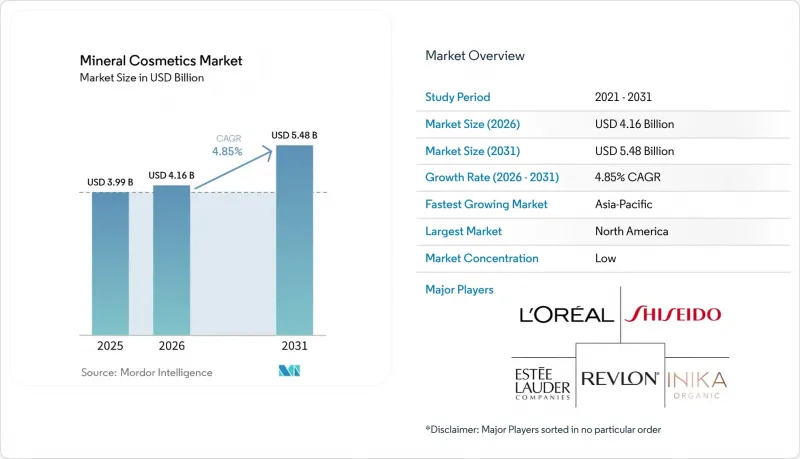

Mineral Cosmetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the mineral cosmetics market size is projected to expand from USD 3.99 billion in 2025 and USD 4.16 billion in 2026 to USD 5.48 billion by 2031, registering a CAGR of 4.85% between 2026 to 2031.

This report is Segmented by Product Type (Skincare Products, Makeup Products, and Haircare Products), End User (Women and Men), Distribution Channel (Supermarkets/Hypermarkets, Specialty/Drug Stores, Online Retail, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Mineral Cosmetics Market Trends and Insights

Growing Demand for Clean-Label Beauty Products

The clean-label shift is supporting the mineral cosmetics market through both consumer demand and regulation. EU Regulation (EU) 2025/877 took effect on September 1, 2025, and added further limits on substances classified as carcinogenic, mutagenic, or toxic for reproduction in cosmetic products. This matters because many mineral-led formulas already rely on simpler ingredient systems, so they face less reformulation pressure than synthetic-heavy alternatives. In the United States, MoCRA has also raised the level of ingredient scrutiny through expanded product listing and compliance requirements, which is pushing brands toward greater traceability and clearer label language. As a result, the mineral cosmetics market benefits from a demand pattern that is being reinforced by both end users and regulatory conditions.

Rising Prevalence of Sensitive Skin and Dermatological Conditions

Sensitive skin is becoming a more important commercial driver for the mineral cosmetics market because it shapes both product choice and channel choice. Galderma reported in September 2025 that up to 70% of people globally say they have sensitive skin, and the study linked this rise to urban living, oxidative stress, and sleep disruption. This pattern lifts demand for formulations that are non-comedogenic, anti-inflammatory, and lower in potential irritants. It also makes pharmacy counters, dermatology clinics, and medi-spa settings more important because shoppers often want validation before moving away from conventional products. Brands that can show clinical tolerability are therefore in a better position to build trust and repeat buying in the mineral cosmetics market.

Premium Pricing Compared to Conventional Cosmetics

Premium pricing remains one of the clearest limits on faster mineral cosmetics market adoption. Higher-purity sourcing, smaller production scale, and certification-related costs make many mineral products more expensive than comparable conventional alternatives. This matters most in Southeast Asia, sub-Saharan Africa, and parts of South America, where premium beauty spending is still narrow outside major urban areas. Cost pressure also rises when brands try to maintain responsible mica sourcing, because tighter sourcing standards can limit procurement flexibility and keep raw material costs elevated. Even when interest is strong, the mineral cosmetics market can lose conversion if the price gap is too wide at the shelf.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Multi-Functional Cosmetics

- Innovation in Mineral Cosmetic Formulations

- Limited Consumer Awareness in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Skincare products held 44.23% of the mineral cosmetics market share in 2025, which made them the largest product category. According to the Tricoci University data from 2026, United States accounts for about 16% of global skincare spending. Moisturizers, cleansers, and toners led this segment because mineral actives fit naturally into products used for barrier support, daily comfort, and lower irritation risk. This part of the mineral cosmetics market also benefits from simpler clinical communication, since tolerability and non-comedogenic positioning are easier to explain than color payoff or wear time. Pharmacy and dermo-cosmetics counters support repeat purchases because the consumer often enters through a skin concern rather than a beauty trend.

Within product type, the mineral cosmetics market size for makeup products is projected to grow at a 5.68% CAGR through 2031, which makes it the fastest-rising category. Face makeup leads this group because foundations, tinted moisturizers, and SPF-infused complexion products offer an easy entry point for buyers who want fewer products in their routine. Jane Iredale's Spring Edit 2026, led by the Skintuition SPF 30 Radiance-Boosting Liquid Foundation in 26 shades, shows how brands are moving deeper into liquid complexion formats rather than staying focused on powders alone. Haircare remains a smaller part of the mineral cosmetics market, but it adds a broader personal care use case for consumers who want fewer synthetic ingredients across the full routine.

Complete Report Scope:

- Product Type

- Skincare Products

- Moisturizers

- Cleansers

- Toners

- Others

- Makeup Products

- Face Makeup

- Eye Makeup

- Lip Makeup

- Haircare Products

- Shampoo

- Conditioners

- Others

- Skincare Products

- End User

- Women

- Men

- Distribution Channels

- Supermarkets/Hypermarkets

- Specialty/Drug Stores

- Online Retail Channels

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Poland

- Belgium

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Vietnam

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Peru

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 35.84% of the mineral cosmetics market share in 2025, which made it the largest regional cluster. The United States set the pace because specialty retail is mature and ingredient scrutiny is high. Canada shows similar demand for clean-label and sensitive-skin products, while Mexico is becoming a premium beauty pocket in major urban centers. Europe followed with Germany and France as anchor markets, supported by stronger ingredient oversight and consistent consumer demand for minimally processed beauty products. The UK also remains relevant for the mineral cosmetics market because premium shelf expansion continued through bareMinerals' rollout into 19 Marks & Spencer beauty halls in 2025.

Asia-Pacific is projected to grow at a 6.52% CAGR through 2031, which gives it the fastest regional mineral cosmetics market size expansion in the forecast period. China leads volume in the region because a larger middle class and stronger attention to product safety are lifting interest in ingredient-validated formulas. South Korea supports category education through its hybrid beauty and skin care culture, where consumers are already familiar with BB creams and cushion formats. India offers large long-run potential because sensitive facial skin is widely reported among internet users, but price sensitivity and strong conventional preferences still slow faster conversion. Vietnam, Indonesia, Thailand, and Singapore are adding incremental demand as e-commerce widens access to imported and premium mineral brands.

South America remains led by Brazil, where spending is concentrated among premium urban consumers and where regulatory documentation is familiar to brands already aligned with European standards. Argentina, Colombia, Chile, and Peru show opportunity, but economic volatility makes distribution planning less predictable. In the Middle East and Africa, the UAE and Saudi Arabia stand out for high beauty spending, while halal alignment can strengthen trust in clean, non-animal-derived mineral formulas. Nigeria, South Africa, Morocco, and Turkey add longer-term potential, especially where high UV exposure, humidity, urbanization, and e-commerce make mineral SPF and complexion products more relevant.

- L'Oreal S.A.

- The Estee Lauder Companies Inc.

- Shiseido Company, Limited

- Revlon, Inc.

- Glo Skin Beauty

- Jane Iredale

- Cover FX Skincare Inc.

- Mineralissima Cosmetics BV

- Ahava Dead Sea Laboratories Ltd.

- Bare Escentuals Beauty, LLC

- Colorescience, Inc.

- Youngblood Mineral Cosmetics LLC

- RMS Beauty LLC

- W3LL People, Inc.

- Au Naturale Cosmetics, LLC

- Inika Organic Pty Ltd

- Alima Pure, LLC

- Lily Lolo Ltd.

- Bellapierre Cosmetics, Inc.

- Everyday Minerals, LLC

- Pur Minerals, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Clean-Label Beauty Products

- 4.2.2 Rising Prevalence of Sensitive Skin and Dermatological Conditions

- 4.2.3 Growing Demand for Multi-Functional Cosmetics

- 4.2.4 Innovation in Mineral Cosmetic Formulations

- 4.2.5 Expansion of Vegan and Cruelty-Free Beauty Products

- 4.2.6 Increasing Disposable Income and Premium Beauty Spending

- 4.3 Market Restraints

- 4.3.1 Premium Pricing Compared to Conventional Cosmetics

- 4.3.2 Limited Consumer Awareness in Emerging Markets

- 4.3.3 Regulatory and Labeling Challenges

- 4.3.4 Performance Perception Challenges

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Skincare Products

- 5.1.1.1 Moisturizers

- 5.1.1.2 Cleansers

- 5.1.1.3 Toners

- 5.1.1.4 Others

- 5.1.2 Makeup Products

- 5.1.2.1 Face Makeup

- 5.1.2.2 Eye Makeup

- 5.1.2.3 Lip Makeup

- 5.1.3 Haircare Products

- 5.1.3.1 Shampoo

- 5.1.3.2 Conditioners

- 5.1.3.3 Others

- 5.1.1 Skincare Products

- 5.2 End User

- 5.2.1 Women

- 5.2.2 Men

- 5.3 Distribution Channels

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Specialty/Drug Stores

- 5.3.3 Online Retail Channels

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Sweden

- 5.4.2.8 Poland

- 5.4.2.9 Belgium

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Vietnam

- 5.4.3.7 Indonesia

- 5.4.3.8 Thailand

- 5.4.3.9 Singapore

- 5.4.3.10 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Peru

- 5.4.4.5 Colombia

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 L'Oreal S.A.

- 6.4.2 The Estee Lauder Companies Inc.

- 6.4.3 Shiseido Company, Limited

- 6.4.4 Revlon, Inc.

- 6.4.5 Glo Skin Beauty

- 6.4.6 Jane Iredale

- 6.4.7 Cover FX Skincare Inc.

- 6.4.8 Mineralissima Cosmetics BV

- 6.4.9 Ahava Dead Sea Laboratories Ltd.

- 6.4.10 Bare Escentuals Beauty, LLC

- 6.4.11 Colorescience, Inc.

- 6.4.12 Youngblood Mineral Cosmetics LLC

- 6.4.13 RMS Beauty LLC

- 6.4.14 W3LL People, Inc.

- 6.4.15 Au Naturale Cosmetics, LLC

- 6.4.16 Inika Organic Pty Ltd

- 6.4.17 Alima Pure, LLC

- 6.4.18 Lily Lolo Ltd.

- 6.4.19 Bellapierre Cosmetics, Inc.

- 6.4.20 Everyday Minerals, LLC

- 6.4.21 Pur Minerals, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK