PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073301

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073301

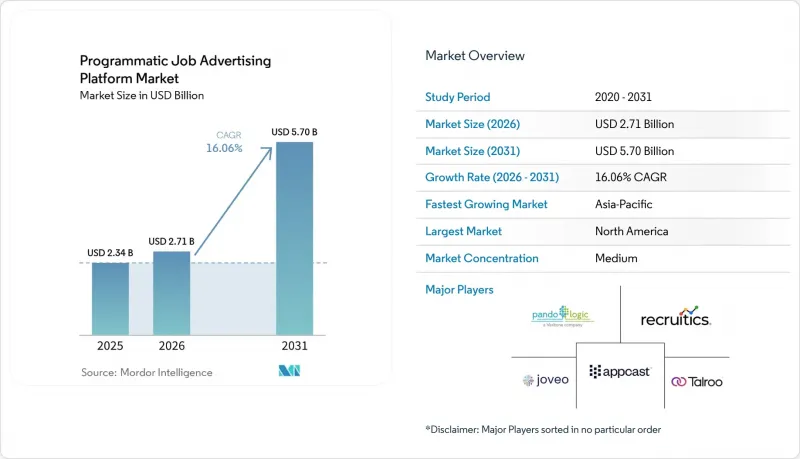

Programmatic Job Advertising Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the programmatic job advertising platform market size is projected to expand from USD 2.34 billion in 2025 and USD 2.71 billion in 2026 to USD 5.70 billion by 2031, registering a CAGR of 16.06% between 2026 to 2031.

This report is Segmented by Component (Solution, and Services), Deployment Mode (Cloud-Based, and On-Premise), Enterprise Size (Small and Medium-Sized Enterprises, and Large Enterprises), Industry Vertical (IT and Telecom, Banking, Financial Services and Insurance, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Programmatic Job Advertising Platform Market Trends and Insights

Programmatic Shift Toward Performance-Based Recruitment Advertising

Employers are reallocating budgets toward platforms that charge only for completed applications, a change that cut cost-per-qualified-candidate by 15% and reduced time-to-fill by 25% in deployments combining automated quality tracking with programmatic bidding.The ability to distribute vacancies across thousands of boards and halt spend on under-performing sources enables recruiters to redeploy 38% of the time previously spent on manual posting toward candidate engagement.

Growing Adoption of AI-Driven Talent Acquisition Workflows

Eighty-four percent of talent acquisition leaders plan to deploy agentic AI by 2026, with Asia-Pacific showing recruiter AI uptake above 75% in India, Singapore, and Australia. Conversational bots embedded in programmatic platforms now screen and schedule around the clock in more than 100 languages, trimming manual coordination by over 90% for Radancy clients.

Cookie Deprecation Impact on Audience Targeting Accuracy

Chrome's phase-out of third-party cookies is eroding behavioral targeting signals, and California's Automated Decision-Making Technology rules now require fresh privacy assessments for algorithmic tools, raising vendor compliance costs. Platforms that integrate first-party ATS data and server-side conversion tracking are mitigating signal loss but smaller vendors lacking engineering depth risk margin compression.

Other drivers and restraints analyzed in the detailed report include:

- Tight Labor Markets in Specialized Skills Segments

- Rising Importance of Employer Branding Across Digital Channels

- Persistent Data Silos Across ATS and Programmatic Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services represented 34.67% of the Programmatic job advertising platform market in 2025, but their 19.03% CAGR through 2031 signals a decisive pivot toward outcome-linked campaign management and privacy consulting. Buyers lean on vendor teams for ATS mapping, taxonomy harmonization, and quality-of-hire analytics that validate spending. Implementation packages often run parallel with change-management programs that reskill recruiters for data-driven workflows. Managed-service offerings have widened as Appcast and Radancy incorporate search, social, and video interviewing, creating bundled propositions attractive to resource-strained talent teams.

Software licenses will keep anchoring topline revenue, yet services are evolving from optional extras into indispensable accelerators of time-to-value. Enterprises facing multi-country regulatory regimes rely on vendor experts to localize consent flows and bias documentation. As a result, services revenue is poised to contribute a larger slice of the Programmatic job advertising platform market size even while software margins remain stable.

On-premise environments retained a majority 58.45% share in 2025 because financial services and healthcare employers prefer in-house custody of candidate data. However, cloud platforms grew almost triple the overall market thanks to elastic capacity, zero-downtime upgrades, and API-level connections to large publisher ecosystems. Vendors now default to cloud-native releases, ensuring parity of features and security patches across their entire user base.

Hybrid adoption is rising, with sensitive applicant records remaining on internal servers while bid optimization, reporting, and AI agents execute in the vendor cloud. California's new audit-trail obligations make centralized logging easier in software-as-a-service environments, nudging risk-averse sectors toward at least partial cloud usage. This interplay of regulatory pressure and product innovation is widening the total addressable Programmatic job advertising platform market without compromising data sovereignty.

Complete Report Scope:

- By Component

- Solution

- Services

- Implementation Services

- Managed Services

- Support and Maintenance Services

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Enterprise Size

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- IT and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare

- Retail and E-Commerce

- Manufacturing

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America generated 38.52% of 2025 revenue, underpinned by the world's most mature ATS ecosystem and early adoption of AI-driven recruitment marketing. BLS figures indicate the region maintained unemployment near a tight 3.8% in early 2026, sustaining employer urgency despite isolated hiring slowdowns in financial services. Federal employment reductions trimmed public-sector demand, yet technology and healthcare hiring pipelines remain resilient.

Asia-Pacific is forecast to post a 17.43% CAGR as India, Singapore, and Australia display recruiter AI adoption rates above 75%, outpacing global benchmarks. High application volumes per posting compel employers to rely on automated quality scoring to sift candidates, making programmatic tools central to recruiter workflow. Startups in Bengaluru and Sydney are piloting outcome-based pricing that pays vendors only for hires, demonstrating the region's willingness to experiment with aggressive commercial models.

Europe's trajectory is shaped by balanced regulation and AI optimism. A European Central Bank survey of 5,000 firms showed AI adopters were 4 percentage points more likely to expand headcount, indicating complementarity with job creation rather than substitution.The continent's stringent GDPR regime continues to steer vendors toward privacy-by-design architectures that are now being exported to other regions. South America, Middle East, and Africa represent emerging corridors where mobile-first hiring and government digitalization programs will gradually lift adoption, though informal labor structures still limit immediate scale.

- Appcast, Inc.

- Joveo, Inc.

- PandoLogic, Inc.

- Talroo, Inc.

- Recruitics, LLC

- Symphony Talent, LLC

- SmartDreamers, Inc.

- JobAdX Corporation

- ClickIQ Ltd.

- HireMya, Inc.

- Adway AB

- Radancy, Inc.

- VONQ B.V.

- Broadbean Technology Limited

- AppVault, LLC

- Joblift GmbH

- Perengo Inc.

- Recooty Technologies Private Limited

- KRT Marketing, Inc.

- Bayard Advertising Agency, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Programmatic Shift Toward Performance-Based Recruitment Advertising

- 4.2.2 Growing Adoption of AI-Driven Talent Acquisition Workflows

- 4.2.3 Tight Labor Markets in Specialized Skills Segments

- 4.2.4 Rising Importance of Employer Branding Across Digital Channels

- 4.2.5 Emergence of Unified Omnichannel Recruitment Campaign Management

- 4.2.6 Proliferation of Privacy-Compliant First-Party Data Partnerships with Job Boards

- 4.3 Market Restraints

- 4.3.1 Persistent Data Silos Across ATS and Programmatic Platforms

- 4.3.2 Cookie Deprecation Impact on Audience Targeting Accuracy

- 4.3.3 Inflation-Driven Hiring Freezes in Key End-Use Industries

- 4.3.4 Escalating Publisher Floor Prices on High-Traffic Job Boards

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Implementation Services

- 5.1.2.2 Managed Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium-Sized Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare

- 5.4.4 Retail and E-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Appcast, Inc.

- 6.4.2 Joveo, Inc.

- 6.4.3 PandoLogic, Inc.

- 6.4.4 Talroo, Inc.

- 6.4.5 Recruitics, LLC

- 6.4.6 Symphony Talent, LLC

- 6.4.7 SmartDreamers, Inc.

- 6.4.8 JobAdX Corporation

- 6.4.9 ClickIQ Ltd.

- 6.4.10 HireMya, Inc.

- 6.4.11 Adway AB

- 6.4.12 Radancy, Inc.

- 6.4.13 VONQ B.V.

- 6.4.14 Broadbean Technology Limited

- 6.4.15 AppVault, LLC

- 6.4.16 Joblift GmbH

- 6.4.17 Perengo Inc.

- 6.4.18 Recooty Technologies Private Limited

- 6.4.19 KRT Marketing, Inc.

- 6.4.20 Bayard Advertising Agency, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment