PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073319

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073319

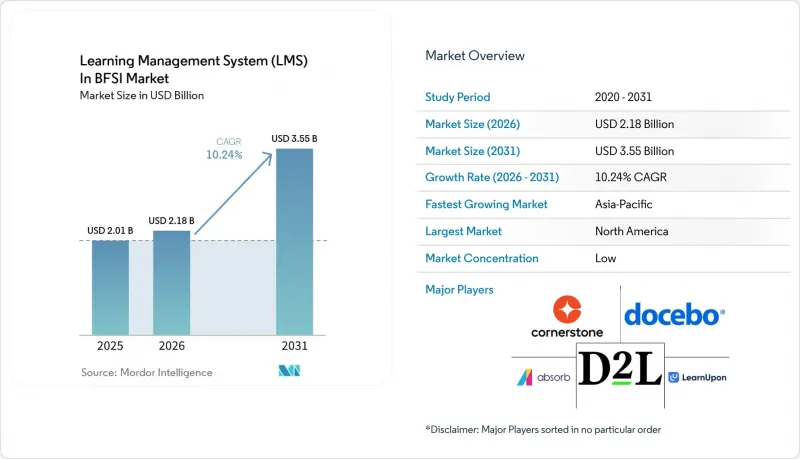

Learning Management System (LMS) In BFSI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the learning management system (LMS) in the BFSI Market is expected to increase from USD 2.01 billion in 2025 to USD 2.18 billion in 2026, and reach USD 3.55 billion by 2031, growing at a CAGR of 10.24% over 2026-2031.

This report is Segmented by Component (Software Platforms and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Delivery Mode (Self-Paced and Distance Learning, and More), Application (Compliance and Regulatory Training, AML/KYC Training, and More), End User (Banks, Insurance Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Learning Management System (LMS) In BFSI Market Trends and Insights

Regulatory Compliance Digitization Across BFSI Workflows

Regulatory compliance digitization has become the primary purchase trigger in the LMS market for the BFSI industry, as supervisors now demand auditable, role-based, and outcome-linked training records. Financial institutions can no longer rely on annual completion certificates when examiners ask whether staff understood and applied the required controls. FINRA's 2026 examination priorities require firms to document the adequacy of Firm Element training, verify remote completion, and integrate regulatory updates promptly, which raises the value of systems with strong audit features and workflow discipline. European resilience expectations have also increased pressure on institutions to maintain current ICT risk learning and defensible training evidence across affected staff groups. In the LMS market in BFSI, platforms that map content completion to job roles, regulatory clauses, and review calendars are steadily replacing static certification routines. This shift keeps training budgets tied to operational risk and examination readiness rather than to discretionary HR planning.

Rising Cybersecurity And Data Privacy Training Mandates

Cybersecurity has moved to the center of training demand in the LMS in the BFSI market because institutions now face a constant stream of threats, privacy obligations, and resilience requirements. The European Banking Authority reported that 82% of EU banks identified cyber risk and data security as their primary concern in March 2025, showing how digital risk has overtaken many traditional operational priorities. In the United States, the New York State Department of Financial Services Part 500 framework requires annual cybersecurity training covering social engineering for all covered entities, supporting recurring enterprise learning cycles. The FFIEC's cybersecurity awareness guidance and the move toward NIST Cybersecurity Framework 2.0 have also strengthened the expectation that training be ongoing and documented rather than event-based. The OCC's 2025 resilience report showed that examiner training already includes ransomware, distributed ledger technology, and AI-enabled fraud, signaling that supervised institutions are increasingly expected to meet this standard. Vendors that can update content quickly in line with regulatory publication calendars are therefore gaining an edge over platforms built around annual refresh cycles.

Legacy Core System And HRIS Integration Complexity

Legacy system architecture remains one of the clearest brakes on the LMS in the BFSI market because implementation quality still depends on identity, data, and user lifecycle connections across old platforms. Many banks and insurers operate with several generations of HRIS, authentication, and core systems, and each mismatch can create missing enrollments, access issues, or incomplete compliance records. When native connectors are available, integration can move in weeks, but custom integration with older self-hosted systems can extend implementation timelines into months and undermine the value of fast procurement decisions. OnCourse Learning identified LMS-HRIS integration failures as a leading cause of auto-enrollment gaps and missing compliance records in examiner reviews, making integration depth a business risk rather than a technical inconvenience. The Federal Reserve OIG also pointed to inconsistent IT examination tooling in its 2025 review, which aligns with the broader governance problems institutions face when learning systems do not connect cleanly to control environments. This restraint is sharper in Asia-Pacific and the Middle East and Africa, where locally built banking systems often lack the standardized interfaces expected by global LMS vendors.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Digital Banking And Insurtech Upskilling Needs

- Cloud-Based Learning Adoption Across Distributed Workforces

- Data Residency And Information Security Concerns In Regulated Learning Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms retained 70% of the component segment in 2025, keeping the core platform layer as the largest revenue base in the LMS market in BFSI. This lead came from the continued shift away from classroom-heavy delivery toward digital systems that can scale across branches, business lines, and compliance programs. Institutions value the platform because it supports audit trails, centralized administration, and near-real-time updates when rules change. That means the platform itself has become a basic requirement for large and mid-sized financial organizations rather than a discretionary tool.

Services are forecast to grow at a 11.52% CAGR through 2031, indicating where buyers are adding the most incremental value around the LMS in the BFSI market. Financial institutions increasingly purchase implementation support, compliance curriculum design, localization, and managed learning operations together with the software license. FINRA's FLEX offering illustrates this split between platform infrastructure and compliance content services because firms can access pre-built learning content while still managing delivery through their own environments. This pattern is strongest among mid-tier banks and insurers that need quick regulatory readiness but lack internal L&D resources to design and maintain a comprehensive compliance curriculum.

Cloud-based deployment accounted for 68.23% of the LMS market in the BFSI market in 2025 and is projected to expand at a 11.53% CAGR through 2031. This position reflects the operational value of systems that can scale during certification peaks, support mobile access, and give compliance leaders a unified reporting view across locations. In the BFSI market, LMSs have favored cloud infrastructure because regulators and internal control teams want evidence that training changes can be distributed quickly when guidance changes. Cloud systems also align better with broader enterprise software stacks, especially when institutions want learning data connected to HR, performance, and access management systems.

On-premises deployments remain relevant for institutions with strict internal hosting policies, especially state-linked banks and regulated entities that retain sensitive employee records within domestic infrastructure. Hybrid deployment is therefore gaining traction because it lets institutions keep learner data in-country while using cloud delivery for speed, reach, and resilience. AWS's European Sovereign Cloud initiative confirms that regulated buyers now expect residency-aware architecture, which supports hybrid and sovereign-ready procurement models. In the LMS in the BFSI industry, this means the long-term winner is less likely to be a pure cloud or pure on-premises model and more likely to be a controlled cloud architecture built around regional compliance needs.

Complete Report Scope:

- By Component

- Software Platforms

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By Delivery Mode

- Self-Paced and Distance Learning

- Instructor-Led Training

- Blended Learning

- Mobile Microlearning

- By Application

- Compliance and Regulatory Training

- AML/KYC Training

- Product Training

- Process and Operational Training

- Risk, Fraud and Cybersecurity Training

- Customer Education and Partner Enablement

- Onboarding

- Sales Enablement

- Leadership and Advisory Training

- Certification and Continuing Education

- By End User

- Banks

- Insurance Firms

- Capital Markets and Wealth Management Firms

- Fintech and Payment Service Providers

- Credit Unions and Cooperative Financial Institutions

- NBFCs and Lending Institutions

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America accounted for 38.12% of the global LMS market in the BFSI market in 2025, making it the largest regional contributor. The region remains the most compliance-driven adoption environment because institutions operate under overlapping federal, self-regulatory, and state training expectations. The New York State Department of Financial Services Part 500 regulation requires covered entities to complete annual cybersecurity training, which supports recurring learning cycles and stronger audit documentation. FINRA's current examination priorities add to this pressure by emphasizing timely training updates, remote completion verification, and documented adequacy of Firm Element programs, all of which keep learning infrastructure tied to supervisory readiness.

Europe is a major demand center for LMSs in the BFSI market because institutions must manage overlapping obligations tied to operational resilience, conduct, privacy, and national banking secrecy rules. The region's compliance stack creates training demand across ICT risk, consumer treatment, product governance, and data handling, which increases the value of platforms with stronger curriculum mapping and evidence controls. European operational resilience requirements have pushed institutions toward more frequent ICT risk learning and away from annual refresh-only models. South America is also becoming more relevant as financial institutions standardize compliance programs across dispersed branch networks and digital channels, even though adoption remains less mature than in North America and Europe.

Asia-Pacific is projected to grow at a 12.84% CAGR through 2031, making it the fastest-expanding regional block in the LMS BFSI market. Growth comes from stronger regulatory maturity in ASEAN and South Asia and from rapid workforce expansion in banking, fintech, and insurtech. Singapore's AI risk management guidelines, published in November 2025, require financial institutions to ensure documented competency among personnel involved in AI development and deployment, thereby creating a clear training demand cycle for governance and oversight. China is also deepening structured learning through formal credit hours and certification pathways, while insurance channel training is being institutionalized through accredited online programs. In the Middle East, adoption is concentrated in Gulf financial centers with stronger cyber and risk training mandates, while Africa remains earlier stage and is better suited to mobile-first deployments that can support expanding digital payments and agent banking networks.

- Cornerstone OnDemand, Inc.

- Docebo Inc.

- D2L Corporation

- Absorb Software Inc.

- LearnUpon Limited

- 360Learning SA

- Epignosis LLC

- Intellum, Inc.

- Thought Industries, Inc.

- iSpring Solutions, Inc.

- Learning Pool Limited

- Heuristix Digital Technologies Private Limited

- Paradiso Solutions LLC

- Neovation Inc.

- TOVUTI, INC.

- SkyPrep Inc.

- Skillcast Group plc

- LearnWorlds (CY) Ltd

- Schoox, LLC

- DigitalChalk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Regulatory Compliance Digitization Across BFSI Workflows

- 4.3.2 Rising Cybersecurity and Data Privacy Training Mandates

- 4.3.3 Accelerating Digital Banking and Insurtech Upskilling Needs

- 4.3.4 Cloud-Based Learning Adoption Across Distributed Workforces

- 4.3.5 AI Literacy and Model Risk Governance Training Demand

- 4.3.6 Extended Enterprise Training for Agents, Brokers, Advisors, and Partners

- 4.4 Market Restraints

- 4.4.1 Legacy Core System and HRIS Integration Complexity

- 4.4.2 Data Residency and Information Security Concerns in Regulated Learning Workflows

- 4.4.3 Training Fatigue From Always-On Regulatory Change Cycles

- 4.4.4 Localization Burden Across Multi-Jurisdiction Rulebooks and Product Taxonomies

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Delivery Mode

- 5.3.1 Self-Paced and Distance Learning

- 5.3.2 Instructor-Led Training

- 5.3.3 Blended Learning

- 5.3.4 Mobile Microlearning

- 5.4 By Application

- 5.4.1 Compliance and Regulatory Training

- 5.4.2 AML/KYC Training

- 5.4.3 Product Training

- 5.4.4 Process and Operational Training

- 5.4.5 Risk, Fraud and Cybersecurity Training

- 5.4.6 Customer Education and Partner Enablement

- 5.4.7 Onboarding

- 5.4.8 Sales Enablement

- 5.4.9 Leadership and Advisory Training

- 5.4.10 Certification and Continuing Education

- 5.5 By End User

- 5.5.1 Banks

- 5.5.2 Insurance Firms

- 5.5.3 Capital Markets and Wealth Management Firms

- 5.5.4 Fintech and Payment Service Providers

- 5.5.5 Credit Unions and Cooperative Financial Institutions

- 5.5.6 NBFCs and Lending Institutions

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Cornerstone OnDemand, Inc.

- 6.4.2 Docebo Inc.

- 6.4.3 D2L Corporation

- 6.4.4 Absorb Software Inc.

- 6.4.5 LearnUpon Limited

- 6.4.6 360Learning SA

- 6.4.7 Epignosis LLC

- 6.4.8 Intellum, Inc.

- 6.4.9 Thought Industries, Inc.

- 6.4.10 iSpring Solutions, Inc.

- 6.4.11 Learning Pool Limited

- 6.4.12 Heuristix Digital Technologies Private Limited

- 6.4.13 Paradiso Solutions LLC

- 6.4.14 Neovation Inc.

- 6.4.15 TOVUTI, INC.

- 6.4.16 SkyPrep Inc.

- 6.4.17 Skillcast Group plc

- 6.4.18 LearnWorlds (CY) Ltd

- 6.4.19 Schoox, LLC

- 6.4.20 DigitalChalk

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment