PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073333

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073333

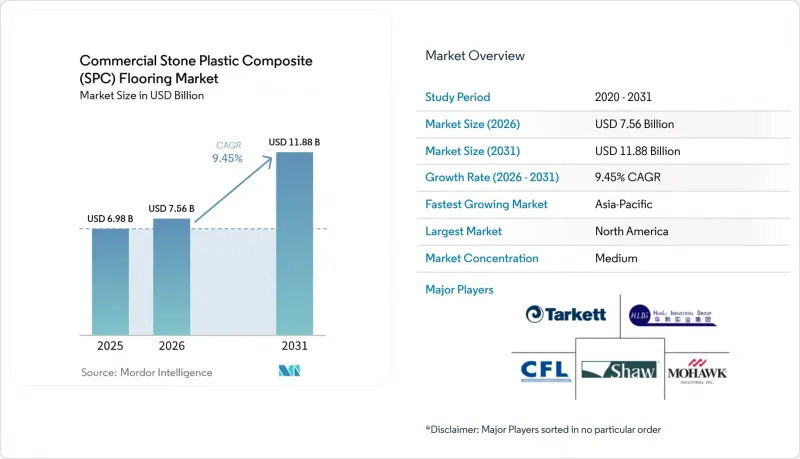

Commercial Stone Plastic Composite (SPC) Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the commercial stone plastic composite flooring Market size was valued at USD 6.98 billion in 2025 and is estimated to grow from USD 7.56 billion in 2026 to reach USD 11.88 billion by 2031, at a CAGR of 9.45% during the forecast period (2026-2031).

This report is Segmented by Product Type (Tiles, Planks), Thickness (4. 0-5. 0 Mm, 5. 1-6. 0 Mm, 6. 1-6. 5 Mm, >6. 5 Mm), Installation Method (Self Adhesive, Glue Down, Click Lock, Others), Distribution Channel (Direct/Contractors, Distributors, Retail, E Commerce), and Geography (North America, South America, Asia-Pacific, and More). Market Forecasts are in Value (USD).

Global Commercial Stone Plastic Composite (SPC) Flooring Market Trends and Insights

Renovation Driven Demand for Fast, Low Downtime Rigid Core in Commercial Interiors

Project owners favor SPC rigid core for renovation schedules that keep facilities operational while construction moves zone by zone. According to supplier installation guides, click lock systems enable floating installation that is significantly faster than glue-down alternatives, with immediate walk-on access and no 24-48 hour adhesive curing time, resulting in reduced labor and minimal business downtime in occupied hospitality and office spaces. These floating assemblies bridge minor subfloor irregularities without extensive surface preparation, lowering callbacks compared with glue-down options that require longer adhesive curing and more intensive prep work. Institutional environments prioritize low-emission certifications to speed re-occupancy after renovation, which is why FloorScore, testing to California Section 01350 VOC limits, has become standard for procurement in healthcare and education facilities seeking LEED, WELL, or CHPS compliance. Suppliers' renovation references highlight cleaner execution, waterproof cores that tolerate daily wet cleaning and spills, and lower risk of moisture-related delays in commercial interiors.

Rigid Core (SPC) Gaining Share Within LVT for Durability and Waterproofing

Rigid core SPC constructions address dimensional stability issues more effectively than traditional flexible LVT. Manufacturer specifications and product comparisons emphasize low expansion rates (typically <=0.05%, with some reporting shrinkage <=0.02%) and stable performance in temperature swings, with high-density cores and thicker commercial wear layers (0.5 mm / 20 mil or more) supporting castor chair tests (often passing 25,000 cycles under 90 kg load) for rolling loads and high footfall zones such as corridors and lobbies. SPC's waterproof core eliminates swelling and surface deformation after daily wet cleaning and spills in healthcare sterile processing, kitchens, and public restrooms, unlike flexible LVT, which can be affected by prolonged moisture exposure around edges. The format is often delivered with click systems under formal license agreements for consistent locking integrity and repeatable quality across large footprints. These product attributes, together, are driving substitution from flexible vinyl toward rigid-core choices within the commercial segment in 2026.

PVC Resin and Additive Price Volatility Impacting Bid Competitiveness

SPC relies on PVC resin alongside calcium carbonate, and several producers flag resin and additive volatility as pricing risks that compress margins on long-lead projects. According to manufacturer formulations and production references, PVC resin typically accounts for 25-30% of the core, while limestone (calcium carbonate) accounts for 60-75%, with prices closely linked to global oil and feedstock fluctuations, such as the documented 3-5¢/lb increases in PVC resin in early 2026. Petrochemical market reports explain how upstream cycles translate into resin price changes that flow through flooring price quotes with timing lags that complicate bidding and procurement. Regional differentials also shape sourcing choices in a given year, prompting buyers to weigh lower-resin-price zones against trade actions and logistics exposures. Many wholesalers and importers have shifted from just-in-time to more buffered inventories to sustain supply continuity during feedstock spikes. The partial mitigation of SPC versus flexible vinyl, due to its higher limestone content, does not eliminate volatility but can moderate exposure relative to fully PVC-dependent constructions.

Other drivers and restraints analyzed in the detailed report include:

- IAQ Certified Low Emitting SPC Easing Specs in Healthcare and Education

- Expanding Commercial Adoption Across Office, Hospitality, Healthcare, Education

- End of Life Recycling Limits and PVC Scrutiny in Specifications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SPC planks captured 68.30% share in 2025, as large-format visuals, realistic wood textures, and efficient installation supported scale across corridors, guest rooms, and open offices. Designers often select long boards to reduce seam frequency and to deliver continuous lines of sight across expansive spaces while maintaining commercial durability. SPC tiles are advancing as the fastest-growing format, with a 9.82% CAGR through 2031, driven by increased interest in modular and geometric patterns for lobbies, reception areas, and branded public spaces. Company design guides show herringbone, chevron, and large-format stone looks implemented via licensed locking systems that support reliable alignment across patterned installations. The functional performance of planks and tiles is comparable because both formats share waterproof rigid cores and commercial wear layers, so selection pivots on design language and installation workflows rather than core differences.

In projects with high aesthetic stakes, stone-look SPC tiles in larger dimensions are gaining traction where maintenance, slip performance, and weight reduction are priorities relative to ceramics. Vendors outline how click-lock assemblies reduce job-site complexity for patterned or large-format designs compared with traditional ceramic-setting materials. As procurement teams standardize on IAQ and Environmental Product Declaration (EPD) documentation for the commercial stone plastic composite flooring market, the adoption of tiles in signature zones complements the broad utility of planks in background and circulation spaces. Specifiers who rely on a single family across both tile and plank formats can consolidate colorways, textures, and trim details while preserving consistent maintenance protocols. This mix supports a balanced volume strategy across the commercial stone plastic composite flooring market as 2026 decisions blend design intent with predictable performance.

The 5.1-6.0 mm band accounted for 42.75% of 2025 demand as buyers balanced unit costs with commercial performance in light-to-mid-duty corridors and multipurpose rooms. Factory-attached acoustic foams in these mid-thickness builds help projects meet baseline impact-isolation targets in many codes, reducing procurement and coordination steps compared with separate underlayment. Above 6.5 mm, products are projected to grow at a 9.65% CAGR through 2031, reflecting tighter acoustic targets and occupant comfort expectations in multifamily and senior living spaces. Supplier documentation points to thicker cores with higher IIC and STC ratings that can avoid the cost and complexity of secondary sound mats in many assemblies, while maintaining waterproof performance and commercial wear layers. These dynamics support a tilt toward premium construction in the commercial stone plastic composite flooring market when long-term lifecycle costs and warranty risk outweigh initial material savings.

Buyers who continue to specify thinner formats usually do so for budget-constrained refreshes or lighter-duty retail and office applications where rolling loads and acoustic transmission are minimal. Where code or brand standards direct higher acoustic values, thicker constructions with integrated foam layers deliver measurable performance benefits without introducing different installation methods across a project. The commercial stone plastic composite flooring industry has also adopted thicker profiles to increase click-joint strength and ease fit-up on large, open floors, thereby shortening installation schedules and reducing rework risk. These advantages now appear in many standard spec templates that institutional procurement teams distribute for fit-outs and renovations. The appeal of thicker profiles, therefore, extends beyond acoustics and reflects a more general desire for stability in heavy wear environments served by the commercial stone plastic composite flooring industry.

Complete Report Scope:

- By Product Type

- SPC Tiles

- SPC Planks

- By Product Thickness

- 4.0-5.0 mm

- 5.1-6.0 mm

- 6.1-6.5 mm

- Above 6.5 mm

- By Installation Method

- Self-Adhesive

- Glue-Down

- Interlocking/Click-lock

- Others

- By Commercial End Users

- Hospitality

- Healthcare Facilities

- Educational Institutes

- Retail (malls, showrooms, stores)

- Offices & Corporate Workspaces

- Other Commercial End Users

- By Distribution Channel

- Direct Sales

- Offline Direct to Projects/Contractors

- Online D2C

- Indirect/Dealers

- Distributors/Wholesalers

- Specialty Retail & Home Improvement

- E-commerce/B2B Marketplaces

- Direct Sales

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

North America accounted for 32.90% of the global market share for commercial stone plastic composite flooring in 2025, driven by institutional renovations in hospitality, healthcare, and education. U.S. and Canadian buyers give weight to IAQ credentials and public documentation of environmental performance, which has reinforced the importance of formal certifications linked to LEED, WELL, and related frameworks. Manufacturers and certification bodies publicly list SPC products that meet emissions standards and maintain active certificates, providing procurement teams and designers with a common language for compliance. This region also benefits from diversified sourcing strategies that combine regional and overseas supply to address project schedules and inventory planning. As a result, specification flow in 2026 favors SPC lines with clear documentation, strong locking systems, and acoustic packages that meet or exceed baseline isolation targets.

Europe combines mature renovation activity with a high bar for environmental and health documentation, which shapes brand assortments and compliance investments. Industry associations have responded by producing verified EPDs that cover vinyl SPC floor coverings to simplify documentation for architects and general contractors. European portfolios also emphasize phthalate-free stabilizers and emission classifications validated under regional schemes, supported by corporate sustainability content that is readily auditable. Localized warehousing and faster service responses support tight construction timelines, and firms maintain European support teams to align with procurement norms and language expectations. These moves help commercial buyers in 2026 align design, performance, and compliance against the broader decarbonization and health priorities that drive large renovation budgets.

Asia-Pacific is the fastest-growing region, with a 10.47% CAGR through 2031, driven by urbanization dynamics and the continued buildout of diversified rigid-core capacity. Vietnam has become a pivotal node in global SPC supply with large factory investments near deepwater ports to serve both exports and domestic demand. Company disclosures indicate that these factories produce advanced acoustic SPC and scratch-resistant variants that complement capacity in the U.S. and China, forming resilient multi-site networks. Comparative guidance from regional suppliers outlines the practical considerations of sourcing SPC from China versus Vietnam, including trade agreements and shipping profiles into North America and Europe. These factors position Asia-Pacific as both a manufacturing anchor and an expanding demand center for the commercial stone plastic composite flooring market.

- CFL Flooring

- Huali Group (Huali Floors)

- Novalis Innovative Flooring (AVA)

- Mohawk Industries (SolidTech)

- Shaw Industries (Floorte Pro)

- Tarkett (ProGen)

- Mannington Mills (ADURA Rigid)

- Karndean Designflooring (Korlok/Art Select Rigid)

- AHF Products (AHF Contract)

- Gerflor (Creation 55 Rigid Acoustic)

- BerryAlloc (Rigid/SPC LVT)

- Metroflor / HMTX (Inception SPC

- Aspecta Contract)

- LX Hausys (HFLOR PRESTG DECORIGID 55)

- Zhejiang Kingdom Plastics (SPC OEM)

- Decno Group (SPC OEM)

- Beauflor / Beaulieu International Group (Rigid LVT)

- NOX Corporation (Rigid Core LVT)

- Power Dekor (Rigid Core SPC)

- Zhejiang Walrus New Material (SPC)

- Zhejiang GIMIG Technology (SPC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation-driven demand for fast, low-downtime rigid core in commercial interiors

- 4.2.2 Rigid core (SPC) gaining share within LVT for durability and waterproofing

- 4.2.3 IAQ-certified low-emitting SPC (FloorScore/Greenguard Gold) easing specs in healthcare and education

- 4.2.4 Expanding commercial adoption across office, hospitality, healthcare, education

- 4.2.5 Acoustic and lightweight core innovations enabling code compliance and occupant comfort

- 4.2.6 Nearshoring/regional SPC plants reducing tariff and lead-time risk

- 4.3 Market Restraints

- 4.3.1 PVC resin and additive price volatility impacting bid competitiveness

- 4.3.2 End-of-life recycling limits and PVC scrutiny in specifications

- 4.3.3 Floating click joints under heavy rolling loads prompting glue-down specs in some applications

- 4.3.4 IP/trade enforcement on click systems raising compliance/import risks

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD Billion)

- 5.1 By Product Type

- 5.1.1 SPC Tiles

- 5.1.2 SPC Planks

- 5.2 By Product Thickness

- 5.2.1 4.0-5.0 mm

- 5.2.2 5.1-6.0 mm

- 5.2.3 6.1-6.5 mm

- 5.2.4 Above 6.5 mm

- 5.3 By Installation Method

- 5.3.1 Self-Adhesive

- 5.3.2 Glue-Down

- 5.3.3 Interlocking/Click-lock

- 5.3.4 Others

- 5.4 By Commercial End Users

- 5.4.1 Hospitality

- 5.4.2 Healthcare Facilities

- 5.4.3 Educational Institutes

- 5.4.4 Retail (malls, showrooms, stores)

- 5.4.5 Offices & Corporate Workspaces

- 5.4.6 Other Commercial End Users

- 5.5 By Distribution Channel

- 5.5.1 Direct Sales

- 5.5.1.1 Offline Direct to Projects/Contractors

- 5.5.1.2 Online D2C

- 5.5.2 Indirect/Dealers

- 5.5.2.1 Distributors/Wholesalers

- 5.5.2.2 Specialty Retail & Home Improvement

- 5.5.2.3 E-commerce/B2B Marketplaces

- 5.5.1 Direct Sales

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South-East Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East & Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East & Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 CFL Flooring

- 6.4.2 Huali Group (Huali Floors)

- 6.4.3 Novalis Innovative Flooring (AVA)

- 6.4.4 Mohawk Industries (SolidTech)

- 6.4.5 Shaw Industries (Floorte Pro)

- 6.4.6 Tarkett (ProGen)

- 6.4.7 Mannington Mills (ADURA Rigid)

- 6.4.8 Karndean Designflooring (Korlok/Art Select Rigid)

- 6.4.9 AHF Products (AHF Contract)

- 6.4.10 Gerflor (Creation 55 Rigid Acoustic)

- 6.4.11 BerryAlloc (Rigid/SPC LVT)

- 6.4.12 Metroflor / HMTX (Inception SPC; Aspecta Contract)

- 6.4.13 LX Hausys (HFLOR PRESTG DECORIGID 55)

- 6.4.14 Zhejiang Kingdom Plastics (SPC OEM)

- 6.4.15 Decno Group (SPC OEM)

- 6.4.16 Beauflor / Beaulieu International Group (Rigid LVT)

- 6.4.17 NOX Corporation (Rigid Core LVT)

- 6.4.18 Power Dekor (Rigid Core SPC)

- 6.4.19 Zhejiang Walrus New Material (SPC)

- 6.4.20 Zhejiang GIMIG Technology (SPC)

7 Market Opportunities & Future Outlook

- 7.1 Spec-grade SPC with verified acoustic assemblies (E90/E492) for office and multifamily

- 7.2 Circular SPC (EPD-backed, take-back) aligned to LEED v5 procurement