PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073355

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073355

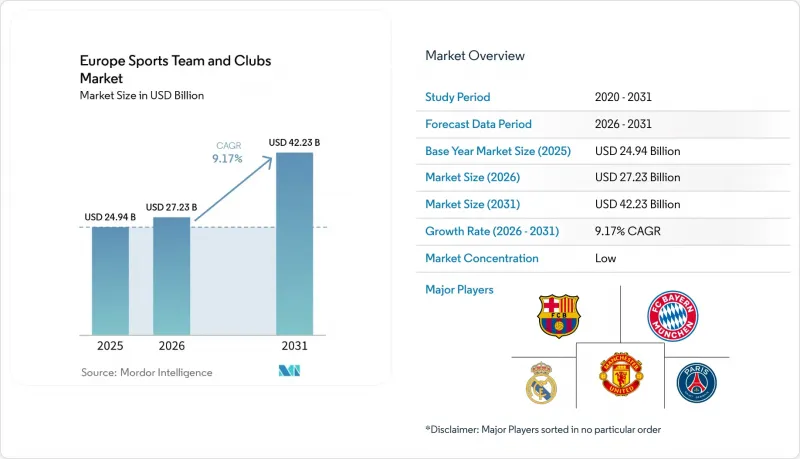

Europe Sports Team and Clubs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe sports team and clubs market size is projected to be USD 24.94 billion in 2025, USD 27.23 billion in 2026, and reach USD 42.23 billion by 2031, growing at a CAGR of 9.17% from 2026 to 2031.

This report is Segmented by Type (Football, Golf, Rugby Union, and More), Revenue Source (Media Rights, Merchandising, and More), Fan Engagement Channel (Club-Owned OTT Platforms, Third-Party Streaming Services, and More), and Geography (United Kingdom, Germany, France, Spain, Italy, BENELUX, NORDICS, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Sports Team and Clubs Market Trends and Insights

Soaring Valuations of Tier-1 Football Clubs

Apollo Sports Capital is driving soaring valuations of Tier-1 football clubs by injecting capital into Atletico de Madrid to expand infrastructure, enhance commercial operations, and strengthen long-term competitiveness. This investment preserves the club's brand and fan loyalty while professionalizing revenue streams from media, sponsorship, and hospitality. By showing how institutional investors can scale clubs into global brands, the deal highlights a pathway for increasing market value across European football. More broadly, private capital is increasingly treating clubs as durable, multi-cycle assets, driving enterprise value growth. Leading European clubs are achieving record valuations, opening opportunities for premium sponsorships, long-term media rights agreements, and infrastructure-led expansion. Stadium projects enhance pricing power and unlock additional revenue from associated real estate, while liquidity in the player market supports asset values and overall balance-sheet stability. Collectively, these trends are powering the rapid increase in valuations of Tier 1 football clubs across Europe.

Media-Rights Inflation Driven by Streaming Wars

Media-rights values are rising as streaming platforms compete for top domestic and international content, boosting revenue across the European sports team and club market. Leagues are leveraging this competition to capture strong pricing power and expand global distribution, enhancing financial resilience. Expanded UEFA competitions provide clubs with additional opportunities to monetize league and tournament participation. Bundled distribution deals allow platforms to preserve premium pricing while reaching wider audiences. Stable domestic rights, combined with international streaming partnerships, are driving higher fan engagement and broader market exposure. This media-rights inflation encourages clubs to invest strategically in commercial operations and infrastructure to maximize returns. It also attracts institutional and private capital, which views clubs as durable, multi-cycle assets with scalable revenue potential. Collectively, these factors are key drivers behind the growth and rising valuations of European sports clubs.

Escalating Player Wage-to-Revenue Ratios

High player wage-to-revenue ratios continue to constrain operating margins across Europe's top leagues, creating financial pressure for clubs. While the Premier League has normalized ratios from pandemic-era peaks, overall wage bills remain elevated, limiting flexibility in other areas of spending. France carries the highest wage burden among major leagues, whereas Germany's governance rules keep costs lower by restricting external capital inflows. New UEFA and domestic spending controls cap squad costs at a percentage of revenue and impose penalties for exceeding limits, forcing clubs to manage expenses more carefully. Clubs with disciplined cost structures can protect margins, but many still rely on occasional player sales to maintain cash flow. Overall, escalating wage obligations and regulatory limits act as a key restraint on market growth, restricting clubs' ability to invest freely in infrastructure, talent, and commercial initiatives.

Other drivers and restraints analyzed in the detailed report include:

- Post-Pandemic Stadium Attendance Recovery

- Surge in Women's Professional Leagues

- Regulatory Caps on Sports Gambling Sponsorship

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Football held 56.43% in 2025 and remained the anchor of the Europe sports team and club market, while women's football recorded the fastest growth trajectory at an 11.87% CAGR for 2026-2031. Within the sport, women's football is emerging as the fastest-growing segment, driven by sustained investment from UEFA and increasing domestic revenue streams in key leagues such as England. Top-tier men's competitions remain supported by large-scale broadcast arrangements, while clubs are adapting to cost controls and shifts in sponsorship by focusing on premium hospitality, digital subscriptions, and data-driven pricing to protect margins. Other sports, including rugby union, cricket, golf, and boxing, contribute to the market through stable broadcast windows, international tournaments, and event-driven income, though they are more dependent on venue throughput and event cadence. Diversified multi-sport clubs also help smooth earnings across cycles, adding stability to the overall market.

The strategic implication for the Europe sports team and club market is a clear reallocation of resources toward women's football, where growth potential remains strong, and investment intensity delivers above-market returns. Leading clubs are increasingly prioritizing the expansion of women's programs while continuing to optimize revenue from men's football and other sports through innovative commercial strategies. Digital content, sponsorship integration, and fan engagement initiatives are becoming key levers across all segments, allowing clubs to diversify income and enhance resilience in a dynamic market environment. Overall, category leaders are balancing stability in established segments with aggressive growth in emerging areas, particularly women's football, to drive long-term market expansion.

Complete Report Scope:

- By Type

- Football

- Golf

- Rugby Union

- Cricket

- Boxing

- Others

- By Revenue Source

- Media Rights

- Merchandising

- Tickets

- Sponsorship

- By Fan Engagement Channel

- Club-Owned OTT Platforms

- Third-Party Streaming Services

- Social-Media Direct-to-Fan

- Stadium & Live Activations

- eSports Integration

- Official Mobile Apps

- By Geography

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

List of Companies Covered in this Report:

- Real Madrid CF

- FC Barcelona

- Manchester United FC

- FC Bayern Munchen AG

- Juventus FC

- Paris Saint-Germain FC

- Liverpool FC

- Arsenal FC

- Chelsea FC

- Manchester City FC

- Tottenham Hotspur FC

- Borussia Dortmund GmbH

- Atletico de Madrid

- AC Milan

- Celtic FC

- Ajax Amsterdam

- Saracens RFC

- Leinster Rugby

- St Andrews Links Trust

- Matchroom Boxing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring valuations of tier-1 football clubs

- 4.2.2 Media-rights inflation driven by streaming wars

- 4.2.3 Post-pandemic stadium attendance recovery

- 4.2.4 Surge in women's professional leagues

- 4.2.5 NFT-based fan-token monetisation

- 4.2.6 Rise of Saudi investment creating 'spill-over' transfer fees

- 4.3 Market Restraints

- 4.3.1 Escalating player wage-to-revenue ratios

- 4.3.2 Regulatory caps on sports gambling sponsorship

- 4.3.3 Macroeconomic squeeze on discretionary spend

- 4.3.4 Fragmented data ownership curbing direct-to-fan plays

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers (Fans & Broadcasters)

- 4.7.3 Bargaining Power of Suppliers (Players & Agents)

- 4.7.4 Threat of Substitutes (eSports, Other Entertainment)

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Football

- 5.1.2 Golf

- 5.1.3 Rugby Union

- 5.1.4 Cricket

- 5.1.5 Boxing

- 5.1.6 Others

- 5.2 By Revenue Source

- 5.2.1 Media Rights

- 5.2.2 Merchandising

- 5.2.3 Tickets

- 5.2.4 Sponsorship

- 5.3 By Fan Engagement Channel

- 5.3.1 Club-Owned OTT Platforms

- 5.3.2 Third-Party Streaming Services

- 5.3.3 Social-Media Direct-to-Fan

- 5.3.4 Stadium & Live Activations

- 5.3.5 eSports Integration

- 5.3.6 Official Mobile Apps

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Real Madrid CF

- 6.4.2 FC Barcelona

- 6.4.3 Manchester United FC

- 6.4.4 FC Bayern Munchen AG

- 6.4.5 Juventus FC

- 6.4.6 Paris Saint-Germain FC

- 6.4.7 Liverpool FC

- 6.4.8 Arsenal FC

- 6.4.9 Chelsea FC

- 6.4.10 Manchester City FC

- 6.4.11 Tottenham Hotspur FC

- 6.4.12 Borussia Dortmund GmbH

- 6.4.13 Atletico de Madrid

- 6.4.14 AC Milan

- 6.4.15 Celtic FC

- 6.4.16 Ajax Amsterdam

- 6.4.17 Saracens RFC

- 6.4.18 Leinster Rugby

- 6.4.19 St Andrews Links Trust

- 6.4.20 Matchroom Boxing

7 Market Opportunities & Future Outlook

- 7.1 Expansion of women's leagues into prime-time broadcast slots

- 7.2 Cross-border club ownership synergies (multi-club groups)