PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073375

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073375

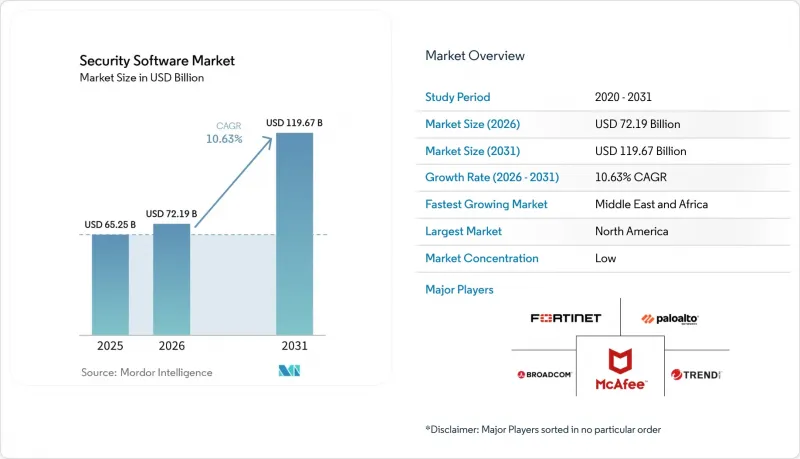

Security Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the security software market size was valued at USD 65.25 billion in 2025 and estimated to grow from USD 72.19 billion in 2026 to reach USD 119.67 billion by 2031, at a CAGR of 10.63% during the forecast period (2026-2031).

This report is Segmented by Product Type (Antivirus/Anti-malware, Firewall & UTM, and Others), Deployment Mode (On-Premises, Cloud-Based and Others), Enterprise Size (Large Enterprises, SME), Application (Mobile Security, Consumer and Others), End-Use Industry (BFSI, Healthcare, Retail & E-Commerce and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Security Software Market Trends and Insights

Escalating Volume & Sophistication of Cyber-Attacks

Attackers are weaponizing generative AI tools that automate spear-phishing, deepfake audio, and polymorphic malware, forcing enterprises to pivot toward adaptive, analytics-driven defenses. In 2024, 25.7% of recorded industrial incidents targeted manufacturing sites, prompting steelmaker Nucor to overhaul its entire detection stack after a breach. APAC accounted for 31% of global attacks last year, and regional cybercrime costs are forecast to reach USD 3.3 trillion by 2025. These threat dynamics accelerate adoption of unified extended detection and response (XDR) platforms within the security software market.

Mandatory Compliance with GDPR, CCPA, DORA & Sectoral Cyber-Rules

Regulators are prescribing technical controls rather than high-level principles. The EU Digital Operational Resilience Act, effective January 2025, compels financial firms to maintain 24-hour incident reporting and third-party risk oversight. Parallel mandates in the Cyber Resilience Act demand secure-by-design software across all connected products. Cross-border organizations therefore favor automated compliance dashboards, boosting platform revenue inside the security software market.

Shortage of Skilled Cyber Personnel Inflates Total Cost of Ownership

A global talent gap of 4.8 million security professionals persists, with the United States alone needing another 265,000 specialists to keep pace with deployment complexity. Scarcity pushes salaries higher, compelling buyers to favour platforms with automation and managed service options. While vendors embed AI-driven orchestration to minimize manual triage, the upfront integration effort still requires scarce engineering skill, slowing rollouts in some verticals.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cloud Workload Expansion Demanding Zero-Trust Security

- Cyber-Insurance Underwriting Now Mandating Software Controls

- Fragmented Tool Sprawl Drives Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity and Access Management platforms generated 22.65% of 2025 revenue, underlining their central role in perimeter-less strategies. The security software market size for IAM is forecast to grow from USD 17.18 billion in 2026 to USD 36.47 billion by 2031, expanding at 16.25% CAGR. IAM suites now bundle password-less authentication, just-in-time privilege, and behavioural analytics, displacing legacy VPNs. Firewall and UTM upgrades remain essential for hybrid traffic inspection, yet spending is shifting toward next-gen offerings aligned to zero-trust principles. Encryption software demand is bolstered by looming quantum threats, with buyers prioritizing vendors offering NIST-validated post-quantum modules. Extended detection and response (XDR) suites unify endpoint, network, and SaaS telemetry, reducing alert fatigue and positioning vendors for wider platform adoption.

Over the forecast period, competitive differentiation will depend on integration depth and AI explainability. Vendors integrating hardware-level root-of-trust, API-first architecture, and built-in compliance mapping are securing larger multiyear renewals. Product roadmaps increasingly feature lightweight agents, confidential computing support, and policy-as-code functions, meeting the orchestration needs of modern DevSecOps pipelines within the security software market.

Cloud-based deployments captured 61.50% revenue in 2025. Organizations cite elastic scalability, continuous feature updates, and opex budgeting benefits. The security software market size for cloud-delivered solutions is projected to climb at an 17.8% CAGR, reaching USD 100.6 billion by 2031. Hybrid models remain vital for regulated workloads; hence leading vendors release on-premises gateways that forward logs to cloud analytics engines for central oversight.

The shift pushes vendors to decouple control planes from data planes, enabling enforcement across container clusters, edge nodes, and SaaS APIs under one policy set. Subscription bundles combining secure access service edge (SASE), cloud access security broker (CASB), and web isolation are resonating, as they cut procurement cycles. On-premises share will gradually decline yet persist in defence, critical infrastructure, and sovereign cloud environments where data-locality rules require in-country processing.

Complete Report Scope:

- By Product Type

- Antivirus / Anti-malware

- Firewall and UTM

- Encryption Software

- Identity and Access Management (IAM)

- Endpoint-protection Platform (EPP / EDR)

- Network Security Platforms

- Other Types

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SME)

- By Application

- Mobile Security

- Consumer Security Suites

- Enterprise / Data-centre Security

- By End-use Industry

- BFSI

- Healthcare

- Retail and e-Commerce

- Manufacturing

- Energy and Utilities

- Aerospace and Defence

- Telecommunications

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America dominated with 37.65% revenue in 2025, supported by the USD 27.5 billion 2025 federal cybersecurity budget. Public-private data-sharing initiatives and a vibrant vendor ecosystem accelerate early adoption of AI-driven analytics. High breach disclosure penalties under U.S. SEC rules further encourage proactive investment.

Europe benefits from harmonized legislation such as the NIS2 Directive and Cyber Resilience Act, providing unified benchmarks for incident response and secure development. Vendors offering built-in multilingual compliance workflows gain traction, especially among pan-EU financial institutions.

The Middle East posts the fastest 14.25% CAGR, spurred by sovereign digital-economy ambitions. Saudi Arabia's cybersecurity market reached SAR 13.3 billion (USD 3.5 billion) in 2025. National regulations mandate local data centers and breach notification within hours, compelling rapid software upgrades. Meanwhile, Asia-Pacific governments invest in joint security centers to mitigate quantum risks and state-sponsored attacks, positioning the region as a significant growth frontier for the security software market.

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Broadcom Inc. (Symantec)

- Check Point Software Technologies Ltd.

- International Business Machines Corporation (IBM)

- Trend Micro Incorporated

- CrowdStrike Holdings, Inc.

- McAfee Corp.

- Kaspersky Lab

- Sophos Group plc

- Bitdefender LLC

- Zscaler, Inc.

- Okta, Inc.

- Cloudflare, Inc.

- SentinelOne, Inc.

- Proofpoint, Inc.

- Rapid7, Inc.

- Qualys, Inc.

- Trellix (Musarubra US LLC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating volume and sophistication of cyber-attacks

- 4.2.2 Mandatory compliance with GDPR, CCPA, DORA and sectoral cyber-rules

- 4.2.3 Rapid cloud workload expansion demanding zero-trust security

- 4.2.4 Cyber-insurance underwriting now mandating software controls

- 4.2.5 Convergence of OT and IT triggering spend on specialised ICS security

- 4.2.6 AI-powered "offensive security tooling" arms-race among threat actors

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled cyber personnel inflates total cost of ownership

- 4.3.2 Fragmented tool sprawl drives integration complexity

- 4.3.3 Rising open-source security stack cannibalises licence revenue

- 4.3.4 Quantum-safe migration uncertainty delaying long-term contracts

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Antivirus / Anti-malware

- 5.1.2 Firewall and UTM

- 5.1.3 Encryption Software

- 5.1.4 Identity and Access Management (IAM)

- 5.1.5 Endpoint-protection Platform (EPP / EDR)

- 5.1.6 Network Security Platforms

- 5.1.7 Other Types

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SME)

- 5.4 By Application

- 5.4.1 Mobile Security

- 5.4.2 Consumer Security Suites

- 5.4.3 Enterprise / Data-centre Security

- 5.5 By End-use Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 Retail and e-Commerce

- 5.5.4 Manufacturing

- 5.5.5 Energy and Utilities

- 5.5.6 Aerospace and Defence

- 5.5.7 Telecommunications

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Cisco Systems, Inc.

- 6.4.3 Palo Alto Networks, Inc.

- 6.4.4 Fortinet, Inc.

- 6.4.5 Broadcom Inc. (Symantec)

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 International Business Machines Corporation (IBM)

- 6.4.8 Trend Micro Incorporated

- 6.4.9 CrowdStrike Holdings, Inc.

- 6.4.10 McAfee Corp.

- 6.4.11 Kaspersky Lab

- 6.4.12 Sophos Group plc

- 6.4.13 Bitdefender LLC

- 6.4.14 Zscaler, Inc.

- 6.4.15 Okta, Inc.

- 6.4.16 Cloudflare, Inc.

- 6.4.17 SentinelOne, Inc.

- 6.4.18 Proofpoint, Inc.

- 6.4.19 Rapid7, Inc.

- 6.4.20 Qualys, Inc.

- 6.4.21 Trellix (Musarubra US LLC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment