PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073378

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073378

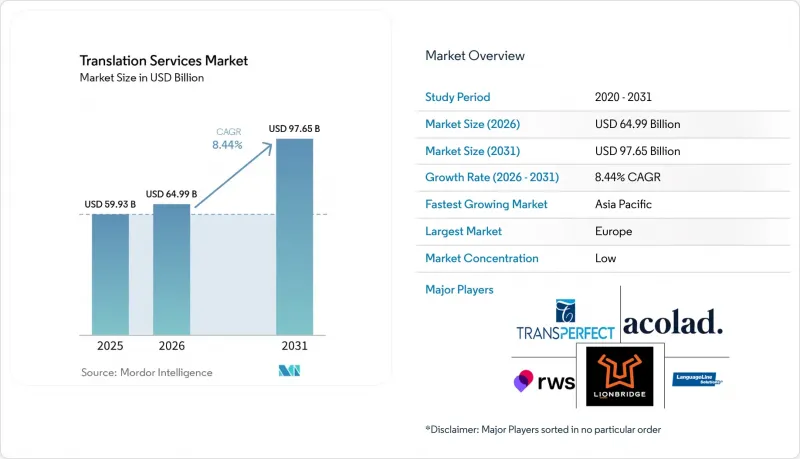

Translation Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, translation services market size in 2026 is estimated at USD 64.99 billion, growing from 2025 value of USD 59.93 billion with 2031 projections showing USD 97.65 billion, growing at 8.44% CAGR over 2026-2031.

This report is Segmented by Component (Hardware, Software), Operation (Human Technical Translation, Machine/Neural Machine Translation), Service (Written Translation, Interpretation, and More), End-User (IT and Telecom, BFSI, Automotive and Manufacturing, Healthcare and Life-Sciences, Legal and Public Sector, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Translation Services Market Trends and Insights

Growth of Global E-Commerce

Online retail sales are heading toward USD 7.4 trillion in 2025 as buyers demand native-language experiences; 76% of shoppers decline purchases when content is not localized.Retailers now translate everything from checkout flows to post-sale support, which lifts revenue performance by 1.5 times for firms that invest in end-to-end localization. City-level cultural tailoring is emerging as brands pursue hyper-local resonance, a nuance machine translation alone cannot guarantee. The smartphone surge in emerging markets fuels voice-to-text translation features that let retailers reach first-time mobile buyers. These dynamics collectively raise transaction conversion rates and sustain recurring demand for the translation services market.

Explosion of Multimedia/Streaming Content

Subscriber growth on global platforms is steering demand toward multilingual subtitles, dubbing, and voice synthesis. AI captioning now cuts production cycles by 60% while retaining emotional fidelity through neural speech cloning. Netflix-style quality frameworks have spawned certification courses that blend technical and cultural skills. Gaming studios mirror this trend by localizing character voices and narratives; titles localized into 14 languages have multiplied revenue across Southeast Asia. Added to this is the rise of live-event interpretation, which broadens revenue streams for language service providers and intensifies competition within the translation services market.

Data-Privacy and Security Concerns

GDPR forces vendors to route EU source text through regional data centers and maintain ISO 27001 controls, raising operating expenses by up to 20%. Enterprises handling sensitive legal or financial documents increasingly insist on on-premises or private-cloud workflows to avert breaches that free online engines might invite. HIPAA overlays further escalate costs for U.S. healthcare content, a barrier that deters smaller providers from scaling. Fragmented global privacy statutes amplify admin workloads, tempering the translation services market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Language Access in Public Services

- Accelerating Cross-Border SaaS Deployments

- Shortage of Qualified Domain-Specialist Linguists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software systems generated 72.88% of the translation services market share in 2025 and are forecast to widen their lead at a 10.34% CAGR. Neural-enhanced translation management systems cut project turnarounds by up to 80%, enabling enterprises to scale global content without proportional staffing. Cloud-native architectures integrate with e-commerce, CRM, and CMS platforms through open APIs, turning localization into a continuous background process.

Hardware retains presence for on-premises conference interpretation and secure healthcare kiosks, yet its revenue weight is sliding as workloads migrate to cloud services. Translation memories now operate as neural suggestion engines that lift domain-specific accuracy to 90%, and automated QA modules use large language models to flag anomalies in a fraction of the time needed by manual reviewers. These advances underscore the structural shift from labor-intensive workflows to technology-centric models that underpin the translation services market.

Machine and neural machine translation streams captured 61.25% of 2025 revenues. Neural MT with targeted post-editing is poised for an 10.76% CAGR because enterprises accept 80% machine-quality output that costs 80% less and arrives 10 times faster. Domain-critical fields such as pharmaceuticals and litigation still require human first-pass translations to mitigate liability, yet hybrid setups prevail elsewhere.

Providers now sell "engine-agnostic" pipelines that automatically pick the best model per language pair, then send results to linguists for light edits. Translators themselves are becoming data curators who train custom engines and monitor outputs for hallucinations. These role shifts are redefining skills demand across the translation services market.

Complete Report Scope:

- By Component

- Hardware

- Software

- By Operation

- Human Technical Translation

- Machine / Neural Machine Translation

- By Service

- Written Translation

- Interpretation (On-site, OPI, VRI)

- Transcreation and Multimedia Localisation

- By End-User

- IT and Telecom

- BFSI

- Automotive and Manufacturing

- Healthcare and Life-Sciences

- Legal and Public Sector

- Media, Gaming and Entertainment

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe generated 44.12% of global revenue in 2025, supported by GDPR-driven multilingual documentation across 24 official languages. Demand remains durable as corporations headquartered in Germany, France, and the UK must file technical and legal content in multiple languages. Brexit complexities add volume as UK firms navigate overlapping EU and domestic regulations, sustaining premium pricing for specialized legal translations.

Asia-Pacific is advancing at a 15.02% CAGR and threatens Europe's lead by 2031. China, Japan, and South Korea are funneling investment into neural MT research, while Southeast Asian gaming studios localize content across Bahasa Indonesia, Thai, Tagalog, and Vietnamese to capture smartphone-native audiences. Mobile commerce dominance also fuels voice translation tools, intensifying growth in the translation services market.

North America maintains a robust compliance-driven base: U.S. federal agencies spend USD 700-800 million a year on outsourced language services for courts, immigration, and public health. Section 1557 enforcement spurs hospital spending on interpreters, and Silicon Valley's SaaS exporters keep pushing continuous localization practices. Canada's bilingual statutes and Mexico's manufacturing-supply-chain role further diversify regional demand.

- TransPerfect

- Lionbridge

- LanguageLine Solutions

- RWS Group

- Acolad Group

- Welocalize

- Smartling

- SDL Trados (now RWS)

- Pactera EDGE

- Phrase (Memsource)

- CyraCom

- Unbabel

- Gengo (Lionbridge AI)

- Appen

- BLEND (One-Hour Translation)

- TextMaster

- LanguageWire

- Pangeanic

- Straker Translations

- Bureau Works

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of Global E-Commerce

- 4.2.2 Explosion of Multimedia/Streaming Content

- 4.2.3 Regulatory Push for Language Access in Public Services

- 4.2.4 Accelerating Cross-Border SaaS Deployments

- 4.2.5 Shift to Continuous Localisation Pipelines

- 4.3 Market Restraints

- 4.3.1 Data-privacy and Security Concerns

- 4.3.2 Shortage of Qualified Domain-specialist Linguists

- 4.3.3 Good-enough- Free MT Eroding Price Realisations

- 4.3.4 Rising Gen-AI Hallucination Risk in Regulated Verticals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Operation

- 5.2.1 Human Technical Translation

- 5.2.2 Machine / Neural Machine Translation

- 5.3 By Service

- 5.3.1 Written Translation

- 5.3.2 Interpretation (On-site, OPI, VRI)

- 5.3.3 Transcreation and Multimedia Localisation

- 5.4 By End-User

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Automotive and Manufacturing

- 5.4.4 Healthcare and Life-Sciences

- 5.4.5 Legal and Public Sector

- 5.4.6 Media, Gaming and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 South-East Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TransPerfect

- 6.4.2 Lionbridge

- 6.4.3 LanguageLine Solutions

- 6.4.4 RWS Group

- 6.4.5 Acolad Group

- 6.4.6 Welocalize

- 6.4.7 Smartling

- 6.4.8 SDL Trados (now RWS)

- 6.4.9 Pactera EDGE

- 6.4.10 Phrase (Memsource)

- 6.4.11 CyraCom

- 6.4.12 Unbabel

- 6.4.13 Gengo (Lionbridge AI)

- 6.4.14 Appen

- 6.4.15 BLEND (One-Hour Translation)

- 6.4.16 TextMaster

- 6.4.17 LanguageWire

- 6.4.18 Pangeanic

- 6.4.19 Straker Translations

- 6.4.20 Bureau Works

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment