PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073456

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073456

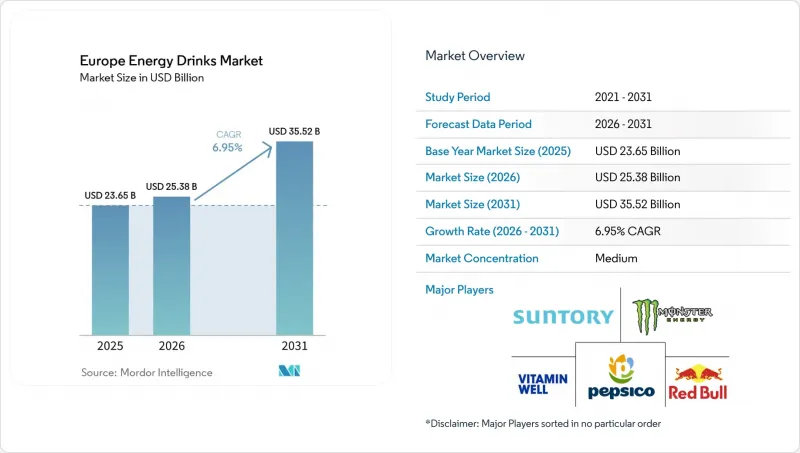

Europe Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe energy drinks market size is projected to be USD 23.65 billion in 2025, USD 25.38 billion in 2026, and reach USD 35.52 billion by 2031, growing at a CAGR of 6.95% from 2026 to 2031.

This report is Segmented by Type (Traditional, Sugar-Free or Low-Calorie, Natural/Organic, Energy Shots, and Other), Packaging Type (PET Bottles, Glass Bottles, Metal Can, Aseptic Packages, and Disposable Cups), Functionality (Endurance/Energy Boost, Muscle Recovery, and Other), Distribution Channel (HoReCa, Retail), and Geography. Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

Europe Energy Drinks Market Trends and Insights

EU Sugar Tax-Prompted Shift to Sugar-Free Energy Drinks

Fiscal measures targeting sugar-sweetened beverages have driven swift reformulation cycles across Europe. By 2025, twelve European Union member states had implemented sugar taxes. The World Health Organization reported that all European countries enforcing soft-drink excise duties also include energy drinks in their scope. The UK's Soft Drinks Industry Levy, introduced in 2018 and expanded in 2024, led Red Bull to release a zero-sugar variant, which now accounts for over 40% of its UK sales. France's tiered tax system, which imposes penalties on beverages containing more than 5 grams of sugar per 100 milliliters, prompted Monster Beverage Corporation to reformulate its core product line with sucralose and acesulfame potassium by mid-2024. In the same year, Belgium and the Netherlands adopted similar frameworks, creating a complex regulatory environment. This situation primarily benefits multinational brands with the R&D resources to develop region-specific products. Meanwhile, smaller regional players, unable to reformulate, face margin pressures or market exits, consolidating market share among the top five brands.

Gen Z and E-Sports Fueled Consumption Surge

Demographic shifts are redefining consumption patterns, placing flavor innovations in the spotlight. Red Bull, with a global presence, supports over 800 athletes and 250 e-sports teams, with a strong focus on Europe's League of Legends and Counter-Strike tournaments. Similarly, Monster Energy secures title sponsorships across various esports franchises. These partnerships are transforming passive viewers into active consumers: 2024 Nielsen data shows that 18-24-year-olds in Germany and Poland consume energy drinks an average of 3.2 times per week, double the frequency of the 35-44 age group. Gen Z increasingly prefers energy drinks offering functional benefits beyond caffeine, such as B-vitamins, taurine, and cognitive enhancers. This trend drove the Q1 2024 launch of Monster Energy's Green Zero Sugar in 16 European markets, featuring 160 mg of caffeine along with L-carnitine and ginseng. Reflecting the changing marketing dynamics, e-sports arenas in the Netherlands and Sweden now host branded lounges where fans can try exclusive flavors, creating a direct marketing loop that bypasses traditional retail channels.

Tighter EU Caps on Caffeine, Taurine, and Youth Advertising

Regulatory frameworks are tightening the permissible formulation envelope. The European Food Safety Authority sets a 200 mg single-dose caffeine cap and a 400 mg daily limit for adults, while children are restricted to 3 mg per kilogram of body weight. EU Regulation 1169/2011 mandates warning labels on beverages surpassing 150 mg of caffeine per liter. Additionally, Lithuania, Latvia, Poland, Romania, Hungary, and Bulgaria have outright bans on sales to minors. In 2025, the UK government proposed extending these age restrictions to those under 16, a move set to heavily impact the UK energy drinks market. Meanwhile, Sweden is mulling over point-of-sale ID checks for energy drinks. Such regulations are reshaping marketing strategies: Red Bull found itself under an EU antitrust probe in November 2025, accused of using exclusivity clauses to limit retailers from stocking rival brands. With advertising bans on youth-targeted campaigns, brands are shifting focus to adults, but this pivot diminishes their reach among the 18-24 age group, which constitutes 35% of the category's volume. Moreover, compliance costs for labeling adjustments and age-verification systems inflate operating expenses by 2-3%, a significant strain for smaller entities.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Convenience and E-Commerce Channels

- Boom in Premium Plant-Based Caffeine Options Like Yerba Mate and Guayusa

- Rising Cardiovascular and Sugar-Linked Health Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, traditional energy drinks, led by Red Bull's original formulation and Monster Energy's core line, held a 41.38% market share. However, natural and organic energy drinks are projected to grow at 8.69% through 2031, driven by a consumer shift toward clean-label ingredients. Within the traditional category, sugar-free and low-calorie variants are the fastest-growing sub-segment, supported by EU sugar taxes and reformulation mandates. Brands like Rockstar and Burn Energy launched zero-sugar SKUs in 2024 to meet this demand. Energy shots, popularized by 5-hour Energy in North America, remain niche in Europe, capturing less than 5% of the volume due to caffeine restrictions and limited retail presence. Other energy drinks, such as functional waters and lightly carbonated blends, attract health-conscious consumers but face challenges scaling due to limited brand equity and marketing resources.

Natural and organic energy drinks, using plant-based caffeine from guayusa, yerba mate, and green tea, command a 25-35% price premium over traditional options. Targeting millennials in Germany, Sweden, and the Netherlands, these products align with the European Commission's Farm to Fork Strategy promoting organic sourcing but face supply-chain constraints limiting growth. Monster Beverage Corporation's Green Zero Sugar, launched in 16 European markets in Q1 2024, bridges traditional and natural segments by combining synthetic caffeine with botanical extracts, appealing to consumers seeking taste and clean labels. Navigating EFSA's caffeine limits and Regulation 1169/2011's labeling requirements adds complexity but offers differentiation in a competitive market.

In 2025, metal cans accounted for 53.64% of the packaging market, valued for their recyclability, portability, and carbonation retention. Glass bottles are expected to grow at 8.15% through 2031, driven by premiumization and sustainability trends. PET bottles, with a 20% volume share, cater to multipacks and value-tier products but face criticism over single-use plastics. This has led brands to adopt recycled PET (rPET) with 50-100% post-consumer content. Aseptic packages, such as Tetra Pak cartons and pouches, face consumer concerns about product quality but offer cost advantages for private-label brands in discount channels. Disposable cups, mainly used in HoReCa settings, represent less than 3% of the volume and are under pressure from the EU's Single-Use Plastics Directive.

In 2024, aluminum can shortages extended lead times to 16-20 weeks and increased packaging costs by 15-20%, prompting brands to shift to glass despite higher costs. Hell Energy and Vitamin Well introduced 250 ml glass bottles in Sweden and Germany in 2024, positioning them as premium alternatives for on-premise consumption in bars and restaurants. Glass's recyclability and inert properties appeal to eco-conscious consumers, but its weight raises freight costs by 30-40%, limiting distribution to regional markets. Ball Corporation and other manufacturers are investing over EUR 1 billion in new European facilities by 2026, but capacity growth lags demand, keeping prices high and driving packaging innovation. Brands with long-term can-supply agreements gain an edge, while smaller players risk stock-outs during peak demand.

Complete Report Scope:

- By Type

- Traditional Energy Drinks

- Sugar-free or Low-calories Energy Drinks

- Natural/Organic Energy Drinks

- Energy Shots

- Other Energy Drinks

- By Packaging Type

- PET Bottles

- Glass Bottles

- Metal Can

- Aseptic packages

- Disposable Cups

- Fucntionality

- Endurance/Energy Boost

- Muscle Recovery

- Other

- By Distribution Channel

- HoReCa

- Retail

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

- Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

List of Companies Covered in this Report:

- Red Bull GmbH

- Monster Beverage Corporation

- PepsiCo, Inc.

- Suntory Holdings Limited

- Vitamin Well Limited

- Hell Energy Magyarorszag Korlatolt Felelossegu Tarsasag

- The Coca-Cola Company

- Primo Water Corporation

- S. Spitz GmbH

- The Monarch Beverage Company Inc.

- Beverage Brands Holding Limited

- Congo Brands

- Dark Dog Drink Co. (Asia) Pte Ltd

- Nocco (Sweden)

- Olvi (Finland)

- Vita Cola GmbH (Germany)

- Mutalo Group (Poland) - producer of Kabisa Energy

- QPower Energy Drink

- Energy Drink Max

- Hell Energy Magyarorszag Kft.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Sugar Tax-Prompted Shift to Sugar-Free Energy Drinks

- 4.2.2 Gen Z and E-Sports Fueled Consumption Surge

- 4.2.3 Rise in Convenience and E-Commerce Channels

- 4.2.4 Boom in Premium Plant-Based Caffeine Options Like Yerba Mate and Guayusa

- 4.2.5 Launch of Nootropic-Enhanced Energy-Plus Beverages

- 4.2.6 Cost Advantages in Central-Eastern Europe Manufacturing

- 4.3 Market Restraints

- 4.3.1 Tighter EU Caps on Caffeine, Taurine, and Youth Advertising

- 4.3.2 Rising Cardiovascular and Sugar-Linked Health Risks

- 4.3.3 Aluminum Can Shortages Driving Up Packaging Expenses

- 4.3.4 Cannibalization from RTD Cold-Brew Coffee

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Traditional Energy Drinks

- 5.1.2 Sugar-free or Low-calories Energy Drinks

- 5.1.3 Natural/Organic Energy Drinks

- 5.1.4 Energy Shots

- 5.1.5 Other Energy Drinks

- 5.2 By Packaging Type

- 5.2.1 PET Bottles

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 Aseptic packages

- 5.2.5 Disposable Cups

- 5.3 Fucntionality

- 5.3.1 Endurance/Energy Boost

- 5.3.2 Muscle Recovery

- 5.3.3 Other

- 5.4 By Distribution Channel

- 5.4.1 HoReCa

- 5.4.2 Retail

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience/Grocery Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channels

- 5.5 Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Netherlands

- 5.5.8 Poland

- 5.5.9 Belgium

- 5.5.10 Sweden

- 5.5.11 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Red Bull GmbH

- 6.4.2 Monster Beverage Corporation

- 6.4.3 PepsiCo, Inc.

- 6.4.4 Suntory Holdings Limited

- 6.4.5 Vitamin Well Limited

- 6.4.6 Hell Energy Magyarorszag Korlatolt Felelossegu Tarsasag

- 6.4.7 The Coca-Cola Company

- 6.4.8 Primo Water Corporation

- 6.4.9 S. Spitz GmbH

- 6.4.10 The Monarch Beverage Company Inc.

- 6.4.11 Beverage Brands Holding Limited

- 6.4.12 Congo Brands

- 6.4.13 Dark Dog Drink Co. (Asia) Pte Ltd

- 6.4.14 Nocco (Sweden)

- 6.4.15 Olvi (Finland)

- 6.4.16 Vita Cola GmbH (Germany)

- 6.4.17 Mutalo Group (Poland) - producer of Kabisa Energy

- 6.4.18 QPower Energy Drink

- 6.4.19 Energy Drink Max

- 6.4.20 Hell Energy Magyarorszag Kft.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK