PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073529

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073529

United States Coffee Pods and Capsules - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

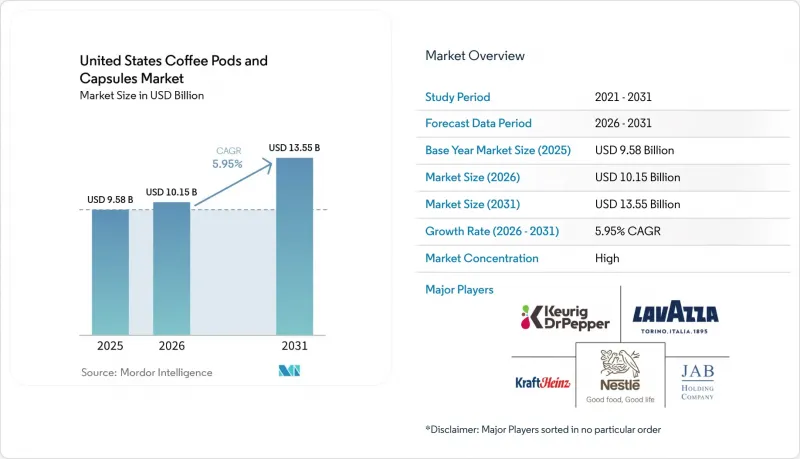

According to Mordor Intelligence, the united states coffee pods and capsules market size was valued at USD 9.58 billion in 2025 and estimated to grow from USD 10.15 billion in 2026 to reach USD 13.55 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031).

This report is Segmented by Product Type (Pods, Capsules), Flavor (Plain, Flavored), Packaging Material (Aluminum, Plastic, Compostable/Biodegradable), Coffee Roast (Light, Medium, Dark), Distribution Channel (Off-Trade, On-Trade), Source (Conventional, Single Origin/Organic/Specialty), and Geography (Northeast, Midwest, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Coffee Pods and Capsules Market Trends and Insights

Rising preference for convenient single-serve coffee in households

The coffee market shows a significant shift toward single-serve options, with 66% of Americans consuming coffee daily and single-cup brewing systems representing 42% of brewing preferences, according to the Spring 2025 National Coffee Data Trends report . The convenience of single-serve pods has effectively bridged the gap between home brewing and coffee shop quality, as evidenced by consistent weekly out-of-home coffee purchases among consumers. Besides, Americans consume 516 million cups of coffee daily, with pod-based systems steadily replacing traditional drip brewing methods. Also, the FDA's recent classification permitting coffee with less than 5 calories to be labeled as "healthy" is expected to increase demand for low-calorie coffee pod varieties. Major companies, including Keurig Dr Pepper, Nestle's Nespresso, and Starbucks, have responded to this trend by developing pods that offer diverse flavors and sustainable options. The expanded availability of coffee pods through online and retail channels has improved consumer access to various options for quality home brewing. This accessibility, combined with consumer preferences for health-conscious and sustainable products, continues to drive the growth of the coffee pods and capsules market.

Expanding availability of specialty and premium pods/capsules

Premium and specialty coffee pods and capsules have become essential offerings in the market, evolving beyond niche segments. The Specialty Coffee Association's 2024 National Coffee Data Trends report indicates that 45% of Americans consumed specialty coffee in the past week, demonstrating substantial market demand . Premium offerings now encompass single-origin certifications, organic compliance, and functional ingredients, enabling higher profit margins. The implementation of the USDA's Strengthening Organic Enforcement Rule in March 2024 has enhanced premium coffee positioning through improved organic certification guidelines and supply chain verification. Millennials significantly influence this market transformation, with more than two-thirds of consumers aged 18-34 preferring single-serve ready-to-drink coffee and demonstrating willingness to pay more for sustainable options. Market innovation is evident in strategic partnerships, such as Nespresso's collaboration with Oatly to produce Barista Edition coffee pods in 2025. Companies like Illy, Lavazza, and Peet's Coffee have expanded their specialty capsule offerings to meet consumer demand for ethically sourced, distinctive coffees in convenient formats. Hence, the U.S. specialty coffee market continues to grow, prompting retailers and producers to increase their premium pods and capsules offerings. This focus on quality and sustainability drives market expansion and product innovation in the coffee pod segment.

Environmental concerns over single-use waste

Environmental concerns regarding single-use coffee pod waste have transformed into regulatory and corporate accountability challenges in the coffee pods and capsules market. In 2024, the U.S. Securities and Exchange Commission (SEC) imposed a USD 1.5 million fine on Keurig Dr Pepper for misleading statements about K-Cup pod recyclability. The SEC determined that Keurig's annual reports for fiscal years 2019 and 2020 claimed effective pod recyclability while omitting that major recycling companies had questioned the feasibility of curbside recycling for these pods and would not accept them. Moreover, Extended Producer Responsibility (EPR) laws in Oregon, Colorado, California, Minnesota, and Maine now require manufacturers to fund packaging disposal, affecting the economic model of single-use pods. These regulations create compliance costs that impact smaller manufacturers and require industry-wide investment in sustainable alternatives, despite their higher production costs. The combination of strict regulations and increased environmental awareness compels coffee pod manufacturers to develop sustainable solutions that remain commercially viable. This shift highlights the importance of accurate environmental reporting and the need to improve packaging design and disposal methods to reduce the environmental impact of single-use coffee systems.

Other drivers and restraints analyzed in the detailed report include:

- Introduction of new flavors, fortified options, and enhanced functionalities

- Advancements in eco-friendly product solutions

- Compatibility issues impacting consumer choice

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Capsules hold 82.63% market share in 2025, as consumers value their consistent brewing performance and flavor preservation capabilities through sealed aluminum and plastic designs. Pods are growing at an 7.85% CAGR through 2031, driven by developments like Keurig's K-Round compostable pods and reusable pod systems that combine environmental responsibility with convenience. This growth pattern indicates environmental concerns' influence on product development, with capsule manufacturers focusing on compostable materials and pod makers advancing material science solutions. Recent innovations like Nespresso's paper pulp capsules and FLO Group's KEYGEA compostable pods show both segments moving toward sustainable options.

Competition between capsules and pods now focuses on brewing system compatibility and environmental performance rather than convenience alone. Capsules maintain advantages through established distribution networks and consumer familiarity. Pods offer market entry opportunities for third-party manufacturers without requiring proprietary system development. Products like Xpod, which allow users to create reusable pods with any coffee beans, indicate pods may gain market share through customization options that capsule systems cannot match. ISO 18606:2013 organic recycling standards influence material selection in both segments, creating regulatory alignment that may reduce capsules' traditional technical advantages.

In 2025, plain coffee holds a dominant 72.05% market share, reflecting a strong consumer preference for traditional coffee values that emphasize bean quality and expert roasting over artificial flavors. Meanwhile, flavored coffees are on a growth trajectory, expanding at a 7.43% CAGR through 2031. This growth is driven by brand collaborations and the integration of functional ingredients, creating differentiated offerings that go beyond conventional coffee profiles. Notable innovations, such as Eggo Coffee's five waffle-inspired flavors and Nespresso's partnership with Oatly Barista, demonstrate how manufacturers are leveraging familiar taste profiles to extend coffee consumption occasions beyond traditional moments.

Flavor innovations are increasingly combining taste with functional benefits. For example, OGI Coffee's chaga mushroom-infused Kona Cherry Blend targets health-conscious consumers by offering cognitive enhancement alongside traditional caffeine benefits. The FDA's GRAS approval for coffee fruit extract (up to 300mg per serving) enables manufacturers to introduce antioxidant-rich formulations that align with wellness trends and command premium pricing. Besides, seasonal offerings, such as Dunkin's limited-edition S'mores, create urgency and collectibility, driving repeat purchases while allowing manufacturers to test market acceptance for potential permanent flavors. Data from the National Coffee Association identifies vanilla and mocha as the most popular flavored options, providing manufacturers with insights to balance innovation with proven consumer preferences.

Complete Report Scope:

- By Product Type

- Pods

- Capsules

- By Flavor

- Plain

- Flavored

- By Packaging Material

- Aluminum

- Plastic

- Compostable/Biodegradable

- By Coffee Roast

- Light Roast

- Medium Roast

- Dark Roast

- By Distribution Channel

- Off-Trade

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

- On-Trade

- Off-Trade

- By Source

- Conventional

- Single Origin/Organic/Speciality Coffee

- By Region

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Keurig Dr Pepper Inc.

- Nestle S.A. (Nespresso & Starbucks-at-Home)

- JAB Holding Company (Peet's, Caribou, Keurig licensees)

- Starbucks Corporation

- Luigi Lavazza S.p.A.

- The Kraft Heinz Company

- The J.M. Smucker Company

- Inspire Brands LLC (Dunkin')

- Restaurant Brands International

- Baronet Coffee

- Illycaffe S.p.A.

- Intelligent Blends

- Coffee Capsules Inc. (Gourmesso)

- Death Wish Coffee

- Black Rifle Coffee Company

- Two Rivers Coffee LLC

- VitaCup, Inc

- Massimo Zanetti Beverage Group

- Newman's Own, Inc.

- San Francisco Bay Coffee

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising preference for convenient single-serve coffee in households

- 4.2.2 Expanding availability of specialty and premium pods/capsules

- 4.2.3 Introduction of new flavors, fortified options, and enhanced functionalities

- 4.2.4 Advancements in Eco-Friendly product solutions

- 4.2.5 Marketing strategies and promotional efforts for coffee pods and capsules

- 4.2.6 Emergence of IoT-connected brewers enabling data-driven replenishment

- 4.3 Market Restraints

- 4.3.1 Environmental concerns over single-use waste

- 4.3.2 Compatibility issues impacting consumer choice

- 4.3.3 Volatility with raw material sourcing or distribution

- 4.3.4 High cost compared to bulk/brewed options

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Pods

- 5.1.2 Capsules

- 5.2 By Flavor

- 5.2.1 Plain

- 5.2.2 Flavored

- 5.3 By Packaging Material

- 5.3.1 Aluminum

- 5.3.2 Plastic

- 5.3.3 Compostable/Biodegradable

- 5.4 By Coffee Roast

- 5.4.1 Light Roast

- 5.4.2 Medium Roast

- 5.4.3 Dark Roast

- 5.5 By Distribution Channel

- 5.5.1 Off-Trade

- 5.5.1.1 Supermarkets/Hypermarkets

- 5.5.1.2 Specialty Stores

- 5.5.1.3 Online Retail Stores

- 5.5.1.4 Other Distribution Channels

- 5.5.2 On-Trade

- 5.5.1 Off-Trade

- 5.6 By Source

- 5.6.1 Conventional

- 5.6.2 Single Origin/Organic/Speciality Coffee

- 5.7 By Region

- 5.7.1 Northeast

- 5.7.2 Midwest

- 5.7.3 South

- 5.7.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Keurig Dr Pepper Inc.

- 6.4.2 Nestle S.A. (Nespresso & Starbucks-at-Home)

- 6.4.3 JAB Holding Company (Peet's, Caribou, Keurig licensees)

- 6.4.4 Starbucks Corporation

- 6.4.5 Luigi Lavazza S.p.A.

- 6.4.6 The Kraft Heinz Company

- 6.4.7 The J.M. Smucker Company

- 6.4.8 Inspire Brands LLC (Dunkin')

- 6.4.9 Restaurant Brands International

- 6.4.10 Baronet Coffee

- 6.4.11 Illycaffe S.p.A.

- 6.4.12 Intelligent Blends

- 6.4.13 Coffee Capsules Inc. (Gourmesso)

- 6.4.14 Death Wish Coffee

- 6.4.15 Black Rifle Coffee Company

- 6.4.16 Two Rivers Coffee LLC

- 6.4.17 VitaCup, Inc

- 6.4.18 Massimo Zanetti Beverage Group

- 6.4.19 Newman's Own, Inc.

- 6.4.20 San Francisco Bay Coffee

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK