PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073548

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073548

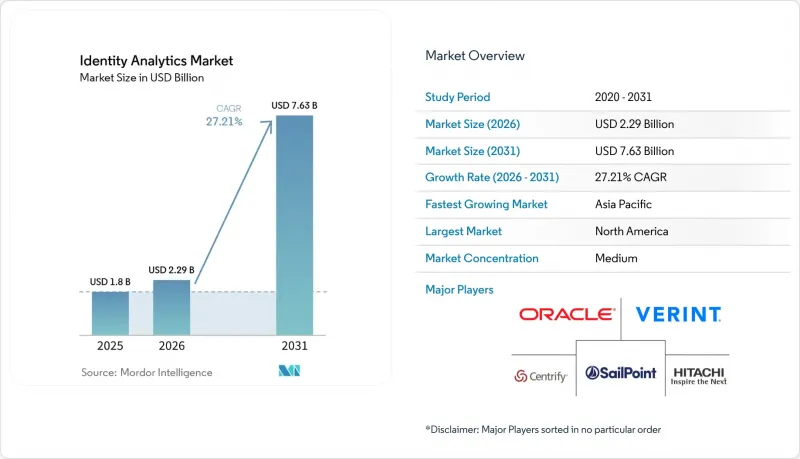

Identity Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the identity analytics market size is expected to grow from USD 1.8 billion in 2025 to USD 2.29 billion in 2026 and is forecast to reach USD 7.63 billion by 2031 at 27.21% CAGR over 2026-2031.

This report is Segmented by Component Type (Solutions, Services), Deployment Model (On-Premises, Cloud), Enterprise Size (Small & Medium Enterprises, Large Enterprises), End-User Industry (Information Technology & Telecommunication, BFSI and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Identity Analytics Market Trends and Insights

Surge in Deep-fake-driven Identity Attacks

Deepfake-enabled impersonation skyrocketed 3,000% in 2024, now representing 6.5% of global fraud attempts. Synthetic identities account for 85% of total identity fraud cases, according to the U.S. Department of Homeland Security. The democratization of generative-AI tooling means threat actors can bypass static biometric checks, compelling enterprises to deploy multilayered analytics that fuse behavioural, device and cryptographic signals. Vendors able to detect AI-generated content in real time are winning proof-of-concept trials, and deepfake mitigation is rapidly becoming a core evaluation criterion in competitive tenders. The urgency of this threat elevates identity analytics investments from discretionary spending to board-level risk mitigation.

Zero-Trust and Machine-Identity Governance Mandates

Executive Order 14144 requires U.S. federal agencies to implement phishing-resistant authentication by December 2025, catalysing broader enterprise zero-trust adoption. Machine-to-machine identities already outnumber human accounts, and unmanaged service credentials expose cloud workloads to lateral-movement attacks. IBM's integration of HashiCorp technology illustrates a shift toward unified identity fabrics that discover, classify and govern millions of API keys and certificates. Compliance deadlines translate into time-boxed procurement cycles, pushing organizations to favour analytics platforms that ship with embedded governance policies. The resulting demand uplift spans public and private sectors, embedding identity analytics market growth into multi-year budget roadmaps.

High TCO of Real-time Analytics at Petabyte Scale

Processing petabyte-level identity data can push annual infrastructure outlays above USD 10 million for large enterprises, and unexpected query spikes during security incidents aggravate cost volatility. Cloud billing models often lack price predictability when customers ingest streaming logs at sustained throughput. Mid-size organizations therefore delay advanced analytics deployments or limit telemetry retention windows, trading visibility for budget certainty. Managed SaaS models that amortize compute across tenants are gaining traction, but margins remain sensitive to cloud egress and GPU leasing rates. Until cost-management tooling matures, procurement cycles may lengthen for budget-constrained buyers.

Other drivers and restraints analyzed in the detailed report include:

- Migration to Cloud-native Identity Fabric

- Gen-AI-based Fraud-detection Performance Gains

- Shortage of Identity-centric Data-science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained a 62.40% revenue share in 2025, anchoring the identity analytics market with integrated platforms that deliver governance, risk scoring and orchestration. Yet services revenue is advancing at a 33.17% CAGR, reflecting enterprises' dependence on vendor expertise for migration roadmaps, regulatory alignment and model optimization. The services contribution to the identity analytics market size is forecast to surpass USD 3.54 billion by 2031, underscoring professional consultancies' role in translating platform capabilities into operational outcomes. Ongoing shortages of identity-centric data scientists further fuel services demand, compelling organizations to engage success-acceleration packages from vendors like SailPoint.

Professional services also address post-implementation challenges such as continuous model tuning and attack-surface reassessment. As executive leadership demands evidence of risk reduction, service teams benchmark fraud metrics, refine detection thresholds and structure remediation workflows. This lifecycle support converts one-time projects into recurring revenue. Conversely, the solutions segment is evolving toward modular micro-services, allowing enterprises to activate analytics functions on demand and pay only for utilized capacity. The interplay between packaged software and high-touch services positions full-stack providers to capture larger wallet share across the identity analytics market.

Cloud deployments represented 70.30% of 2025 revenue and are projected to grow at 30.62% over the forecast horizon, driven in part by enterprise legacy modernization initiatives. Demand is fuelled by elastic compute, API-first integration and built-in high availability. Many organizations, however, operate hybrid estates during multiyear transitions, with parallel on-premises and SaaS directories. This coexistence phase elevates analytics workloads because data must be collected across both environments and correlated in real time. Cloud platforms therefore emphasize connector breadth and policy reconciliation engines that interpret legacy attribute structures.

Identity analytics market share is shifting decisively toward consumption-based pricing, and insurers such as AIG now link premium discounts to customers that evidence continuous monitoring via cloud platforms. Migration roadmaps are informed by Microsoft's published Entra ID playbooks and reference architectures, setting de-facto industry implementation patterns. While total cost of ownership can rise during dual-running periods, long-term economics favour cloud models once on-premises hardware refresh cycles are avoided. Vendors offering granular usage billing and cross-tenant data isolation are positioned to win procurement rounds, especially within multinational enterprises subject to data-residency regulations.

Complete Report Scope:

- By Component Type

- Solutions

- Services

- By Deployment Model

- On-Premise

- Cloud

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-user Industry

- Information Technology and Telecommunication

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Retail and Consumer

- Healthcare and Life Sciences

- Manufacturing, Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America retained a 41.60% revenue share in 2025, buoyed by the Executive Order 14144 mandate and a dense concentration of analytics vendors. Federal deadlines drive near-term spending spikes, while U.S. enterprises leverage favourable cyber-insurance economics tied to advanced identity postures. Canada's digital credential framework and Mexico's burgeoning fintech ecosystem contribute incremental growth, reinforcing regional leadership. Compliance alignment with NIST SP-800-63 guidelines further stimulates platform upgrades and positions North America as the reference market for zero-trust maturity.

Europe follows closely, propelled by the European Digital Identity Regulation that requires interoperable wallet solutions by 2027. The United Kingdom already hosts 270 digital-identity companies, generating USD 2.05 billion in annual revenue. Germany and France emphasize privacy-by-design, obliging vendors to embed consent orchestration and policy versioning into analytics workflows. Data-sovereignty clauses and cross-border transfer rules drive demand for regional data centers and encryption-in-use capabilities. As a result, cloud providers expand European availability zones to accommodate localized processing and maintain competitive parity.

Asia-Pacific represents the fastest-growing region with a 32.86% CAGR forecast through 2031. Government-backed eID schemes, such as Indonesia's USD 1.2 billion digital-transformation partnership and Australia's Digital ID Act 2024, establish mandatory verification layers that require analytics at scale. India's Aadhaar success and China's vast volume of digital transactions provide proof points for neighbouring economies, catalysing uptake across ASEAN. The region's investment in 5G infrastructure and mobile-money adoption creates high-velocity identity telemetry that demands cloud-based analytic performance. Vendors offering language-agnostic interfaces and regionally hosted data options are well placed to gain share as cross-border digital-commerce expands.

- Okta Inc.

- Microsoft Corporation

- Oracle Corporation

- International Business Machines Corporation

- SailPoint Technologies Holdings Inc.

- Ping Identity Holding Corp.

- CyberArk Software Ltd.

- Saviynt Inc.

- Thales Group (Thales Digital Identity and Security)

- HID Global Corporation

- Idemia Group SAS

- Verint Systems Inc.

- LogRhythm Inc.

- Securonix Inc.

- Gurucul Solutions LLC

- MicroStrategy Incorporated

- One Identity LLC

- ForgeRock Inc.

- Centrify Corporation

- Transmit Security Ltd.

- Eviden (an Atos business)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in deep-fake-driven identity attacks

- 4.2.2 Zero-Trust and machine-identity governance mandates

- 4.2.3 Migration to cloud-native identity fabric

- 4.2.4 Gen-AI-based fraud-detection performance gains

- 4.2.5 Cyber-insurance premium discounts tied to analytics

- 4.2.6 Government-backed eID program roll-outs

- 4.3 Market Restraints

- 4.3.1 High TCO of real-time analytics at petabyte scale

- 4.3.2 Shortage of identity-centric data-science talent

- 4.3.3 Inter-operability gaps across legacy IAM stacks

- 4.3.4 Privacy-by-design regulatory hurdles for UEBA

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component Type

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Information Technology and Telecommunication

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Government and Public Sector

- 5.4.4 Retail and Consumer

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Manufacturing, Energy and Utilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Okta Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 SailPoint Technologies Holdings Inc.

- 6.4.6 Ping Identity Holding Corp.

- 6.4.7 CyberArk Software Ltd.

- 6.4.8 Saviynt Inc.

- 6.4.9 Thales Group (Thales Digital Identity and Security)

- 6.4.10 HID Global Corporation

- 6.4.11 Idemia Group SAS

- 6.4.12 Verint Systems Inc.

- 6.4.13 LogRhythm Inc.

- 6.4.14 Securonix Inc.

- 6.4.15 Gurucul Solutions LLC

- 6.4.16 MicroStrategy Incorporated

- 6.4.17 One Identity LLC

- 6.4.18 ForgeRock Inc.

- 6.4.19 Centrify Corporation

- 6.4.20 Transmit Security Ltd.

- 6.4.21 Eviden (an Atos business)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment