PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073558

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073558

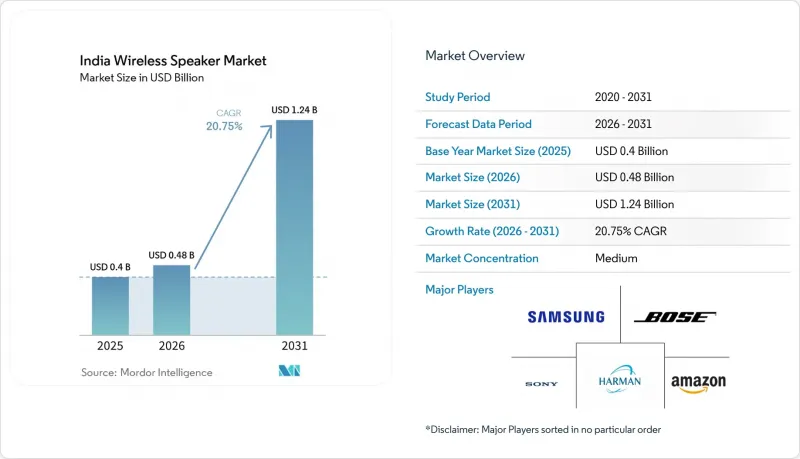

India Wireless Speaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india wireless speaker market size in 2026 is estimated at USD 0.48 billion, growing from 2025 value of USD 0.4 billion with 2031 projections showing USD 1.24 billion, growing at 20.75% CAGR over 2026-2031.

This report is Segmented by Device Type (Bluetooth-Only, Wi-Fi-Only, Smart Speakers, Combo), Distribution Channel (Offline-Organised Retail, Offline-Specialist Audio Stores, and More), Price Range (Entry-Level Less Than USD 150, and More), End-User (Residential, Commercial), and Geography (North, West, South, East, Central, North-East India). The Market Forecasts are Provided in Terms of Value (USD).

India Wireless Speaker Market Trends and Insights

Rising Smartphone and Affordable Data Penetration

Expanded 4G/5G coverage and aggressive handset financing have drawn millions of first-time buyers into the digital ecosystem. Tier-2 and tier-3 cities now post double-digit smartphone growth versus single-digit gains in metros, and their users stream 35-40 GB of data each month, 15-20% higher than urban counterparts. The leap in handset ownership directly fuels hardware attach rates for entry-level Bluetooth speakers and opens a gateway for premium audio upgrades once disposable incomes rise.

OTT Streaming Services Proliferation Reshapes Audio Consumption Patterns

Streaming accounts for 88% of recorded-music revenue, with Indian users listening 26.7 hours weekly, well above global averages. Paid subscriptions rose 58.5%; 69.4% tuned into music livestreams in the previous month. YouTube's 95.2% penetration confirms a mobile-first habit that aligns with portable speaker ownership, while the demand for higher fidelity is steering urban buyers toward Wi-Fi-enabled smart speakers.

Premium Segment Price Sensitivity Constrains Market Expansion

Although the premium tier is registering the quickest growth, the >USD 500 bracket faces a ceiling in smaller towns where disposable incomes are still normalizing. Surveys show 60% of Gen Z shoppers rely on installment options for experiential buys, making flexible financing essential for premium speaker uptake. Brands counter by offering luxurious designs at mid-range prices, as seen in boAt's Stone Opus that mirrors the Marshall Acton aesthetic at one-third the cost.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Home Aspirations Fuel Premium Segment Growth

- PLI Scheme Manufacturing Incentives Strengthen Domestic Supply Chains

- RF-Radiation Health Concerns Create Consumer Hesitancy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth-only units held 52.40% revenue in 2025, underscoring the India wireless speaker market preference for simple pairing with smartphones. Smart speakers, propelled by multilingual voice assistants, are advancing at a 22.60% CAGR and are likely to close the gap by 2031. The India wireless speaker market size for smart speakers is projected to climb from USD 0.06 billion in 2025 to USD 0.2 billion in 2031. Display-equipped models such as Amazon Echo Spot broaden use cases from audio playback to recipe help and security feeds. Wi-Fi-only and combo devices address high-fidelity and multi-room needs in premium homes, while BIS-mandated RF caps keep all form factors within safety norms.

Early adoption began in metros, but Hindi, Tamil, and Punjabi language support is unlocking demand among first-time voice-assistant users in tier-2 cities. JBL's Auracast-enabled PartyBox range demonstrates how legacy audio brands are embedding future-proof wireless protocols to maintain relevance. Longer replacement cycles for fixed smart speakers versus portable Bluetooth units imply higher average selling prices and greater revenue-per-user upside, which the India wireless speaker industry leaders view as a strategic growth lever.

Online vendors controlled 65.90% of the India wireless speaker market in 2025, benefiting from deep discounting, fast delivery pledges, and reach across 90% of PIN codes. Organized audio boutiques, however, are growing 22.30% annually as shoppers in the USD 150-plus bracket look to audition devices before paying. The India wireless speaker market size attributed to specialist stores is forecast at USD 0.12 billion by 2031. In metros, brand-owned showrooms double as experience centers, while in tier-2 cities, chains are franchising smaller footprints that combine product demos with immediate service options.

E-commerce remains crucial for entry-level and refresh sales because price comparisons are easiest online. Yet premium buyers often seek advice on codec support, room acoustics, and warranty add-ons that store staff are trained to supply. Successful brands now execute synchronized releases: product goes live on websites and shelves the same day, and invoice data feeds directly into central CRMs to streamline after-sales. Over time, hybrid strategies that let customers buy online and pick up in store are poised to dominate.

Complete Report Scope:

- By Device Type

- Bluetooth-only

- Wi-Fi-only

- Smart Speakers

- Combo (Bluetooth + Wi-Fi)

- By Distribution Channel

- Online (E-tailers, Brand.com)

- Offline - Organised Retail

- Offline - Specialist Audio Stores

- Offline - Hyper/Super-markets

- By Price Range

- Entry-Level (Less than USD 150)

- Mid-Range (USD 150 - 500)

- Premium (Greater than USD 500)

- By End-User

- Residential

- Commercial

- By Region (India)

- North India

- West India

- South India

- East India

- Central India

- North-East India

List of Companies Covered in this Report:

- Amazon Retail India Private Limited

- Imagine Marketing Limited (boAt)

- HARMAN International (India) Pvt. Ltd. (JBL)

- Sony India Private Limited

- Xiaomi Technology India Private Limited

- Samsung India Electronics Private Limited

- Google India Private Limited

- Bose Corporation India Private Limited

- GN Audio A/S (Jabra)

- Koninklijke Philips N.V.

- Portronics Digital Pvt. Ltd.

- Zebronics India Pvt. Ltd.

- Sennheiser Electronics India Pvt. Ltd.

- Marshall Group India

- Logitech Electronics India Private Limited

- Panasonic India Pvt. Ltd.

- OPPO Mobile India Pvt. Ltd. (realme and Dizo speakers)

- Anker Innovations Technology (India) Pvt. Ltd. (Soundcore)

- Fire-Boltt (Savex Technologies Pvt. Ltd.)

- Lenovo (India) Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising smartphone and affordable data penetration

- 4.2.2 Proliferation of OTT music/video streaming services

- 4.2.3 Rising disposable income and aspiration for smart-home gadgets

- 4.2.4 PLI incentives for domestic audio-electronics manufacturing

- 4.2.5 Regional-language voice-assistant roll-outs

- 4.2.6 Telco-bundled speaker + content offers

- 4.3 Market Restraints

- 4.3.1 High price sensitivity in premium tier

- 4.3.2 RF-radiation and child-health concerns

- 4.3.3 Patchy after-sales network beyond metros

- 4.3.4 BIS RF-compliance certification delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Bluetooth-only

- 5.1.2 Wi-Fi-only

- 5.1.3 Smart Speakers

- 5.1.4 Combo (Bluetooth + Wi-Fi)

- 5.2 By Distribution Channel

- 5.2.1 Online (E-tailers, Brand.com)

- 5.2.2 Offline - Organised Retail

- 5.2.3 Offline - Specialist Audio Stores

- 5.2.4 Offline - Hyper/Super-markets

- 5.3 By Price Range

- 5.3.1 Entry-Level (Less than USD 150)

- 5.3.2 Mid-Range (USD 150 - 500)

- 5.3.3 Premium (Greater than USD 500)

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Region (India)

- 5.5.1 North India

- 5.5.2 West India

- 5.5.3 South India

- 5.5.4 East India

- 5.5.5 Central India

- 5.5.6 North-East India

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Retail India Private Limited

- 6.4.2 Imagine Marketing Limited (boAt)

- 6.4.3 HARMAN International (India) Pvt. Ltd. (JBL)

- 6.4.4 Sony India Private Limited

- 6.4.5 Xiaomi Technology India Private Limited

- 6.4.6 Samsung India Electronics Private Limited

- 6.4.7 Google India Private Limited

- 6.4.8 Bose Corporation India Private Limited

- 6.4.9 GN Audio A/S (Jabra)

- 6.4.10 Koninklijke Philips N.V.

- 6.4.11 Portronics Digital Pvt. Ltd.

- 6.4.12 Zebronics India Pvt. Ltd.

- 6.4.13 Sennheiser Electronics India Pvt. Ltd.

- 6.4.14 Marshall Group India

- 6.4.15 Logitech Electronics India Private Limited

- 6.4.16 Panasonic India Pvt. Ltd.

- 6.4.17 OPPO Mobile India Pvt. Ltd. (realme and Dizo speakers)

- 6.4.18 Anker Innovations Technology (India) Pvt. Ltd. (Soundcore)

- 6.4.19 Fire-Boltt (Savex Technologies Pvt. Ltd.)

- 6.4.20 Lenovo (India) Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment