PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073576

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073576

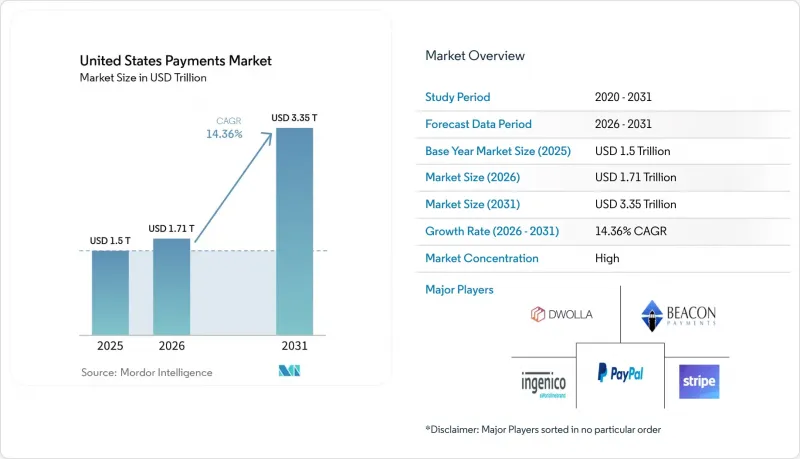

United States Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states payments market size is projected to expand from USD 1.5 trillion in 2025 and USD 1.71 trillion in 2026 to USD 3.35 trillion by 2031, registering a CAGR of 14.36% between 2026 to 2031.

This report is Segmented by Mode of Payment (Point of Sale [Debit Card, Credit Card, Account-To-Account, Digital Wallet, Cash, and More], Online Sale [Debit Card, Credit Card, Account-To-Account, Digital Wallet, Cash-On-Delivery, and More]), and End-User Industry (Retail, Entertainment, Hospitality, Healthcare, Other). Market Forecasts are Provided in Terms of Value (USD).

United States Payments Market Trends and Insights

Surge in Contactless Card Issuance

Contactless credentials already ride in 69% of U.S. debit cards and are expected to reach full penetration by 2027 as issuers replace expiring plastics with NFC-enabled versions. Merchant readiness has kept pace, with 87% of point-of-sale terminals accepting tap-to-pay by 2024, up from 43% in 2020. Faster checkouts raise throughput by roughly 12-18 customers an hour at quick-service restaurants, adding USD 40,000-USD 60,000 in incremental annual revenue for large chains. Crucially, proximity-based authentication habituates users to device-initiated payments, helping smartphones claim 31% of in-store card-present transactions in 2025. The compounding network effect between card hardware, wallet software, and merchant acceptance places the United States payments market on a path toward near-ubiquitous contactless outcomes.

E-Commerce Volume Expansion

U.S. digital commerce registered significant growth, exceeding physical retail growth by more than 7 percentage points. Subscription-heavy consumer behavior, spanning grocery delivery to streaming media, generates data-rich, predictable revenue streams that acquirers can underwrite at lower fraud risk. Retail media networks amplify conversion by embedding one-click checkout next to sponsored placements, lifting purchase rates to 42% compared with 28% for multi-step flows. Solutions such as PayPal Fastlane auto-populate shipping and payment fields across 30 million merchants, cutting cart abandonment by 18 percentage points and producing material fee revenue. These vectors collectively reinforce the momentum propelling the United States payments market.

Interchange Fee Litigation Uncertainty

The rejection of a USD 30 billion settlement in 2024 exposed ongoing volatility in swipe-fee economics. Merchants now hesitate to invest in omnichannel acceptance until legal clarity emerges, while issuers temper spending on rewards programs traditionally funded by interchange spreads. The historical precedent of the Durbin Amendment, which triggered the removal of free checking for 68% of customers and slashed fraud-monitoring budgets, accentuates fears that further regulation could induce unintended consumer impacts. This overhang threatens to marginally dent the otherwise robust trajectory of the United States payments market.

Other drivers and restraints analyzed in the detailed report include:

- Smartphone Wallet Adoption

- FedNow Instant-Rail Enablement of B2B A/R Automation

- Fraud and Chargeback Cost Escalation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Credit cards captured a 40.62% United States payments market share at point of sale in 2025, underpinned by rewards programs that rebate 1.5-5% of spend and secure 78% consumer loyalty to a primary card exceeding five years. Account-to-account payments booked USD 806 billion on Zelle in 2023 and are tracking a 15.63% CAGR through 2031, aided by integration into 2,100 mobile-banking apps serving 120 million users. Debit cards remain the workhorse at 86.7 billion transactions but see relative share erosion as wallets and instant transfer products displace traditional plastic. Digital wallets, already at 31% of card-present volume, subdivide into niche verticals such as premium retail, peer-to-peer, and cryptocurrency trading. Cash usage slipped to 16% of U.S. transaction value in 2023, reflecting both convenience gaps and the limited growth of physical currency in circulation. Buy-now-pay-later solutions, exemplified by Affirm's USD 21.6 billion in fiscal 2024 GMV, cement installment credit as a mainstream checkout option. The interplay of these modes fosters channel diversity that buffers the United States payments market from single-rail disruption.

The United States payments market size for account-to-account transfers is projected to expand at double-digit pace as FedNow and RTP improve real-time liquidity and as merchants adopt lower-cost, low-fraud alternatives to cards. Tokenized credit rails will coexist, particularly for card-on-file subscriptions and high-ticket travel bookings where embedded protections remain valued. Anticipated acceleration in open-banking APIs and wallet-based credentials further tilts growth toward credential-less and biometric-based flows, positioning A2A as the share-gainer through 2031. In parallel, credit networks will emphasize premium rewards, token security, and global acceptance as defensive differentiators. Collectively these vectors ensure that no single modality dominates, underpinning a resilient architecture for the United States payments market.

Complete Report Scope:

- By Mode of Payment

- Point of Sale

- Debit Card Payments

- Credit Card Payments

- Account-to-Account (A2A) Payments

- Digital Wallet

- Cash

- Other Point-of-Sale Payment Mode

- Online Sale

- Debit Card Payments

- Credit Card Payments

- Account-to-Account (A2A) Payments

- Digital Wallet

- Cash-on-Delivery

- Other Online Sales Payment Mode

- Point of Sale

- By End-User Industry

- Retail

- Entertainment

- Hospitality

- Healthcare

- Other End-User Industries

List of Companies Covered in this Report:

- Payment Processors and Gateways

- Card Networks

- Mobile Wallet Providers

- Buy-Now-Pay-Later and Alternative Finance

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Contactless Card Issuance

- 4.2.2 E-Commerce Volume Expansion

- 4.2.3 Smartphone Wallet Adoption

- 4.2.4 FedNow Instant-Rail Enablement of B2B A/R Automation

- 4.2.5 Retail Media Networks Driving In-App One-Click Checkout

- 4.2.6 CBDC Sandbox Pilots Accelerating Bank/Fin-Tech Integration

- 4.3 Market Restraints

- 4.3.1 Interchange Fee Litigation Uncertainty

- 4.3.2 Fraud and Chargeback Cost Escalation

- 4.3.3 2027 PCI-DSS 4.0 Retrofit CAPEX Burden for SMBs

- 4.3.4 Real-Time Payments Liquidity-Management Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment

- 5.1.1 Point of Sale

- 5.1.1.1 Debit Card Payments

- 5.1.1.2 Credit Card Payments

- 5.1.1.3 Account-to-Account (A2A) Payments

- 5.1.1.4 Digital Wallet

- 5.1.1.5 Cash

- 5.1.1.6 Other Point-of-Sale Payment Mode

- 5.1.2 Online Sale

- 5.1.2.1 Debit Card Payments

- 5.1.2.2 Credit Card Payments

- 5.1.2.3 Account-to-Account (A2A) Payments

- 5.1.2.4 Digital Wallet

- 5.1.2.5 Cash-on-Delivery

- 5.1.2.6 Other Online Sales Payment Mode

- 5.1.1 Point of Sale

- 5.2 By End-User Industry

- 5.2.1 Retail

- 5.2.2 Entertainment

- 5.2.3 Hospitality

- 5.2.4 Healthcare

- 5.2.5 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Payment Processors and Gateways

- 6.4.1.1 PayPal Holdings, Inc.

- 6.4.1.2 Stripe, Inc.

- 6.4.1.3 Block, Inc.

- 6.4.1.4 Fiserv, Inc.

- 6.4.1.5 Global Payments Inc.

- 6.4.1.6 Adyen N.V.

- 6.4.1.7 Beacon Payments LLC

- 6.4.1.8 Authorize.Net, LLC

- 6.4.1.9 Toast, Inc.

- 6.4.1.10 Dwolla, Inc.

- 6.4.2 Card Networks

- 6.4.2.1 Visa Inc.

- 6.4.2.2 Mastercard Incorporated

- 6.4.2.3 American Express Company

- 6.4.2.4 Discover Financial Services

- 6.4.3 Mobile Wallet Providers

- 6.4.3.1 Apple Inc.

- 6.4.3.2 Google LLC

- 6.4.3.3 Amazon.com, Inc.

- 6.4.3.4 Samsung Electronics Co., Ltd.

- 6.4.3.5 Meta Platforms, Inc.

- 6.4.4 Buy-Now-Pay-Later and Alternative Finance

- 6.4.4.1 Affirm Holdings, Inc.

- 6.4.4.2 Klarna Bank AB (publ)

- 6.4.4.3 Beacon Payments LLC

- 6.4.4.4 Ingenico Group SA

- 6.4.1 Payment Processors and Gateways

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment