PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073627

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073627

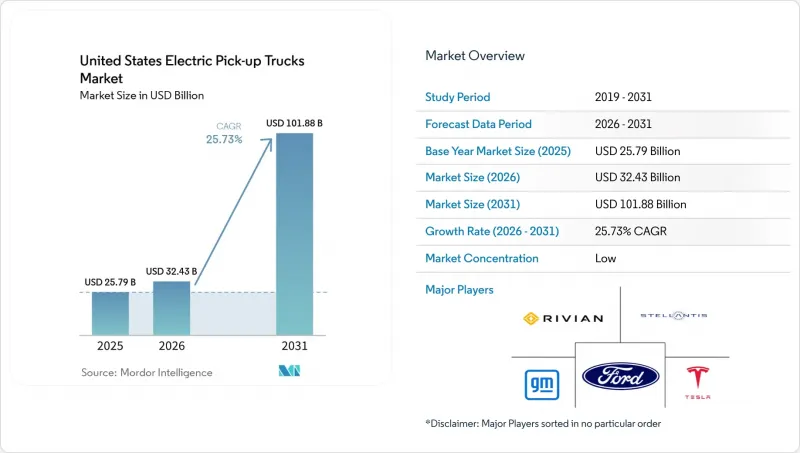

United States Electric Pick-up Trucks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states electric pick-up trucks market size was valued at USD 25.79 billion in 2025 and estimated to grow from USD 32.43 billion in 2026 to reach USD 101.88 billion by 2031, at a CAGR of 25.73% during the forecast period (2026-2031).

This report is Segmented by Fuel Category (Battery-Electric Vehicles and More), Vehicle Class (Class 1 and 2a and Class 2b and 3), Battery Capacity (Below 100 KWh and More), End-User (Retail Consumers and More), Sales Channel (Franchise Dealerships and Direct-To-Consumer / Online), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United States Electric Pick-up Trucks Market Trends and Insights

Falling Battery-Pack Costs

Pack prices continued to slide as domestic gigafactories scaled and material substitution reduced cathode expense. The U.S. Department of Energy projects that cost reductions will narrow the purchase-price gap between battery-electric and gasoline trucks well before mid-decade. Automakers are realigning model portfolios around chemistries that balance range and affordability. Lower pack costs translate into shorter total-cost-of-ownership payback periods, a metric closely tracked by commercial fleets. Reduced capital risk is prompting finance providers to introduce longer-tenor leases, further smoothing the transition. As a result, price sensitivity, once the dominant barrier, is easing for both retail and fleet buyers.

Federal & State Purchase Incentives

Although the federal clean-vehicle credit expired in September 2025, a patchwork of state rebates and point-of-sale tax relief continues to cushion upfront pricing. The ZEV mandate links these incentives to compliance targets, aligning consumer benefits with manufacturers' obligations. Transitional policies concentrate demand into high-population corridors, giving OEMs a predictable launchpad for early volumes. At the same time, procurement programs for public-sector fleets help backstop residual values, lowering lender exposure. Incentive stacks, therefore, act as both demand accelerant and risk-mitigation tool, reinforcing the business case for expanded production.

High Up-front Vehicle Price Differential

The sticker premium over comparable gasoline trucks still weighs on mass-market adoption. With the federal incentive expired, affordability hinges on state programs, OEM leasing strategies, and secondary-market confidence. Financing innovations such as battery-subscription models are emerging, yet their penetration remains limited. Buyers without home charging access also face additional installation costs, creating a compounded hurdle. Until scale economies shave more capital out of the battery, higher entry prices will temper the speed of uptake in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Fleet Decarbonization Mandates

- Domestic Battery-Cell Manufacturing Expansion

- Sparse Rural DC Fast-Charging Coverage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-electric trucks captured 93.12% of the United States electric pick-up trucks market in 2025 and are expected to register a CAGR of 31.33% to 2031, reflecting a decisive lead over hybrid alternatives. Product plans from leading OEMs emphasize larger packs and faster charging, signaling confidence in continued share gains. Greater drivetrain simplicity is lowering service costs, which, in turn, strengthens residual values and lease attractiveness. Software-enabled torque management gives battery-electric models a performance edge that resonates with both recreational and commercial users.

Plug-in and range-extended hybrids remain relevant in regions where charging access is thin, yet their advantage narrows as infrastructure spreads. Brands experimenting with on-board generators pitch extreme-range capability, but market reception hinges on pricing relative to pure battery-electric configurations. Should battery production outpace projections, hybrids may cede even more ground. In parallel, policy frameworks continue to favor zero-tailpipe-emission solutions, creating systemic pressure that aligns with buyer trends.

The 6,001-14,000 lbs segment held 61.74% of the United States electric pick-up trucks market share in 2025, underscoring strong demand from trade, utility, and delivery fleets. Payload capacity and exportable power features meet work-site requirements, making this class the default choice for institutional buyers. Fleet duty cycles also match high-battery utilization profiles, maximizing return on the electrified drivetrain investment.

Conversely, lighter classes are on a faster growth curve, posting a 26.04% CAGR outlook as lifestyle buyers embrace electric trucks for commuting and recreation. Automakers are tailoring these models with sport-oriented trims and digital-first purchase journeys. As battery density improves, lighter trucks will inherit range previously reserved for heavier models, further broadening audience reach. Over time, cross-shopping with mid-size SUVs is likely to raise competitive stakes in the segment.

Complete Report Scope:

- By Fuel Category

- Battery-Electric Vehicles (BEV)

- Hybrid Electric Vehicles (HEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- By Vehicle Class

- Class 1 and 2a (Below 6,000 lbs GVWR)

- Class 2b and 3 (6,001 to 14,000 lbs GVWR)

- By Battery Capacity (kWh)

- Below 100 kWh

- 100 to 150 kWh

- Over 150 kWh

- By End-User

- Retail Consumers

- Commercial and Leasing Fleets

- Government and Utilities

- By Sales Channel

- Franchise Dealerships

- Direct-to-Consumer (DTC) / Online

- By State

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

List of Companies Covered in this Report:

- Ford Motor Company

- General Motors Company

- Mullen Automotive Inc. (Bollinger Motors)

- Stellantis N.V. (Ram)

- Rivian Automotive, Inc.

- Toyota Motor Corporation

- Tesla, Inc.

- Hercules Electric Vehicles

- Via Motors

- Workhorse Group Inc.

- Hyundai Motor Company

- Kia Corporation

- Isuzu Commercial Truck of America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Urbanization, Population and Vehicle/Transit Demand

- 4.2 EV Penetration in Truck Market

- 4.3 Fuel vs Electricity Price Spread (per km, ICE vs EV)

- 4.4 EV vs ICE Total Cost of Ownership (TCO) Gap

- 4.5 Financing and Ownership Models (Loans, Leasing, Subscription)

- 4.6 Battery Chemistry Mix and Pack Energy Density (LFP vs NMC)

- 4.7 Home, Workplace and Public Charger Access / Density

- 4.8 Fast-Charging Network Coverage and Power Bands

- 4.9 Alternative Fuels Infrastructure (Hydrogen for FCEVs)

- 4.10 Subsidy and Consumer Incentive Value

- 4.11 OEM EV Line-up and Model Pipeline

- 4.12 Value-Chain & Distribution-Channel Analysis

- 4.13 Regulatory, Fiscal and Industrial Policy Framework

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Falling Battery-Pack Costs

- 5.2.2 Federal and State Purchase Incentives

- 5.2.3 Corporate Fleet Decarbonization Mandates

- 5.2.4 Domestic Battery-Cell Manufacturing Expansion

- 5.2.5 Bi-directional Charging Revenue Streams

- 5.2.6 High Residual-Value Expectation for Electric Trucks

- 5.3 Market Restraints

- 5.3.1 High Up-front Vehicle Price Differential

- 5.3.2 Sparse Rural DC Fast-Charging Coverage

- 5.3.3 Towing-Related Range Degradation

- 5.3.4 Dealer Service-Network Readiness Gaps

- 5.4 Value/Supply-Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Competitive Rivalry

6 Market Size and Growth Forecasts (Value (USD) & Volume (Units))

- 6.1 By Fuel Category

- 6.1.1 Battery-Electric Vehicles (BEV)

- 6.1.2 Hybrid Electric Vehicles (HEV)

- 6.1.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 6.2 By Vehicle Class

- 6.2.1 Class 1 and 2a (Below 6,000 lbs GVWR)

- 6.2.2 Class 2b and 3 (6,001 to 14,000 lbs GVWR)

- 6.3 By Battery Capacity (kWh)

- 6.3.1 Below 100 kWh

- 6.3.2 100 to 150 kWh

- 6.3.3 Over 150 kWh

- 6.4 By End-User

- 6.4.1 Retail Consumers

- 6.4.2 Commercial and Leasing Fleets

- 6.4.3 Government and Utilities

- 6.5 By Sales Channel

- 6.5.1 Franchise Dealerships

- 6.5.2 Direct-to-Consumer (DTC) / Online

- 6.6 By State

- 6.6.1 Alabama

- 6.6.2 Alaska

- 6.6.3 Arizona

- 6.6.4 Arkansas

- 6.6.5 California

- 6.6.6 Colorado

- 6.6.7 Connecticut

- 6.6.8 Delaware

- 6.6.9 Florida

- 6.6.10 Georgia

- 6.6.11 Hawaii

- 6.6.12 Idaho

- 6.6.13 Illinois

- 6.6.14 Indiana

- 6.6.15 Iowa

- 6.6.16 Kansas

- 6.6.17 Kentucky

- 6.6.18 Louisiana

- 6.6.19 Maine

- 6.6.20 Maryland

- 6.6.21 Massachusetts

- 6.6.22 Michigan

- 6.6.23 Minnesota

- 6.6.24 Mississippi

- 6.6.25 Missouri

- 6.6.26 Montana

- 6.6.27 Nebraska

- 6.6.28 Nevada

- 6.6.29 New Hampshire

- 6.6.30 New Jersey

- 6.6.31 New Mexico

- 6.6.32 New York

- 6.6.33 North Carolina

- 6.6.34 North Dakota

- 6.6.35 Ohio

- 6.6.36 Oklahoma

- 6.6.37 Oregon

- 6.6.38 Pennsylvania

- 6.6.39 Rhode Island

- 6.6.40 South Carolina

- 6.6.41 South Dakota

- 6.6.42 Tennessee

- 6.6.43 Texas

- 6.6.44 Utah

- 6.6.45 Vermont

- 6.6.46 Virginia

- 6.6.47 Washington

- 6.6.48 West Virginia

- 6.6.49 Wisconsin

- 6.6.50 Wyoming

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 Ford Motor Company

- 7.4.2 General Motors Company

- 7.4.3 Mullen Automotive Inc. (Bollinger Motors)

- 7.4.4 Stellantis N.V. (Ram)

- 7.4.5 Rivian Automotive, Inc.

- 7.4.6 Toyota Motor Corporation

- 7.4.7 Tesla, Inc.

- 7.4.8 Hercules Electric Vehicles

- 7.4.9 Via Motors

- 7.4.10 Workhorse Group Inc.

- 7.4.11 Hyundai Motor Company

- 7.4.12 Kia Corporation

- 7.4.13 Isuzu Commercial Truck of America

8 Market Opportunities and Future Outlook

- 8.1 White-Space and Unmet-Need Assessment

9 Key Strategic Questions for CEOs