PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073657

North America Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

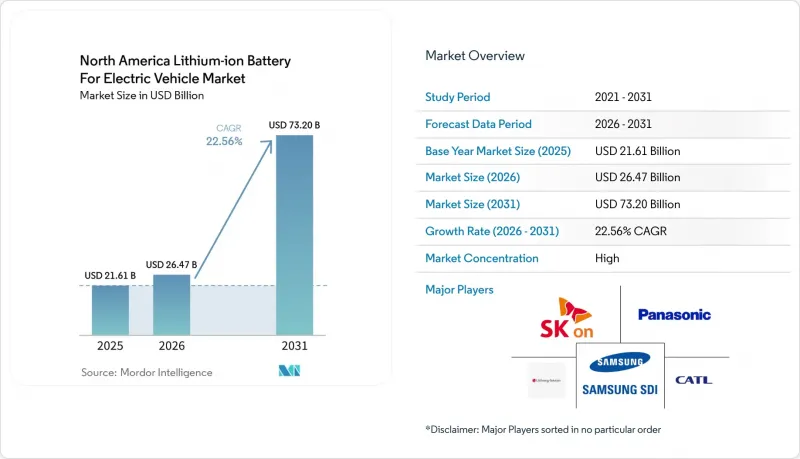

According to Mordor Intelligence, the north america lithium-ion battery for electric vehicle market size is projected to be USD 21.61 billion in 2025, USD 26.47 billion in 2026, and reach USD 73.20 billion by 2031, growing at a CAGR of 22.56% from 2026 to 2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging Chemistries, Lead-Acid, Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, Pouch), Propulsion (BEV, PHEV, HEV), Vehicle Type (Passenger Cars, Lcvs, Medium and Heavy Trucks, Buses, Two and Three-Wheelers), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Declining Lithium-Ion Battery Prices Compressing Cost Barriers

The North America EV lithium-ion battery market is seeing its strongest cost support from the continued fall in battery pack prices. Pack-level costs fell from near USD 300 per kWh in 2018 to USD 95 to USD 115 per kWh in 2026, which improves vehicle affordability and eases pressure on automaker margins. The benefit is still uneven because US-made LFP cells remain more expensive than the Chinese supply, even after production credits narrow part of the gap for local manufacturing economics. That cost spread is pushing the North America EV lithium-ion battery market toward wider LFP adoption in mid-range vehicles and work fleets, where price sensitivity is stronger than in premium passenger programs. GM has stated that shifting from NMC to LFP in part of its portfolio could lower battery cost by at least USD 6,000 per vehicle, which shows how chemistry choice now affects retail pricing as much as vehicle engineering. Lower new-cell prices are also making second-life reuse less attractive in some cost-sensitive fleet applications, which increases the appeal of direct recycling instead of long reuse chains for retired packs.

Growing EV Model Availability and Purchase Incentives Broadening Addressable Demand

The North America EV lithium-ion battery market is benefiting from a wider range of EV models across passenger and commercial categories. Electric medium and heavy-duty vehicle model availability rose from 24 models in 2019 to 161 models by 2025, which materially broadened purchasing options for fleet operators and public buyers. This wider product base is reinforcing battery demand because more duty cycles can now be matched with dedicated electric platforms rather than limited pilot models. California's Advanced Clean Cars II rule and its adoption by additional states are keeping regulatory demand visible into the next decade, which reduces the risk of a short-lived demand spike in the North America EV lithium-ion battery market. The end of the Section 30D consumer credit in September 2025 changed the demand mix, yet commercial operators still retain access to leasing-related support, which has helped fleet electrification hold up better than expected. That shift matters because fleet demand usually involves larger batteries, repeat ordering behavior, and clearer replacement cycles than private retail demand, which gives the North America EV lithium-ion battery market a steadier volume base.

Raw-Material Supply Bottlenecks for Class-1 Nickel Constraining NMC Economics

The North America EV lithium-ion battery market remains exposed to imported Class-1 nickel, which keeps a key input risk in place for high-nickel cathode chemistries. The United States holds less than 3% of global nickel processing capacity, and its only operating nickel mine in Michigan was expected to cease production by the end of 2025, which raises dependence on external supply. Indonesia already dominates global nickel production, and much of that material is tied to Chinese-affiliated processing, which creates IRA eligibility problems under FEOC-related restrictions. As a result, the North America EV lithium-ion battery market is seeing a stronger cost case for LFP in mid-range applications, even when NMC still offers better energy density for premium models. Canada and the United States are trying to improve local supply links, but project timing and scaling remain uncertain enough that nickel will stay a constraint over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Scale-Up of North American Cell Manufacturing Capacity Creating Supply-Side Density

- OEM-Battery Maker Long-Term Offtake Agreements Locking in Supply Visibility

- Thermal-Runaway Reputation Risk Elevating Safety Engineering Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion chemistries held 90.9% of revenue in 2025, which placed this segment at the center of the North America EV lithium-ion battery market size in the base year. The North America EV lithium-ion battery market still relies on NMC for premium passenger EVs because long-range platforms continue to prioritize high energy density. NCA also remains relevant in selected high-performance applications, especially where cylindrical formats and proven production lines already exist. LFP is expanding quickly in mid-range passenger vehicles and commercial platforms because its lower cost and stronger perceived safety profile match the needs of higher-volume programs. GM and LG Energy Solution are moving US capacity toward LFP production, which shows that announced plant plans are now being revised around practical cost targets rather than only technical range goals.

Lead-acid and nickel-metal-hydride chemistries still have small roles in mild-hybrid and auxiliary systems, but their position is weakening as low-voltage architectures increasingly shift toward lithium-ion support. Emerging chemistries held only a minimal revenue share in 2025, yet they are projected to expand at 34.1% through 2031, which makes them the fastest-growing chemistry group in the North America EV lithium-ion battery market. Nissan stated in April 2026 that its 23-layer solid-state prototype pack met charge and discharge benchmarks and remains aimed at a 2028 launch at a USD 75 per kWh pack cost, which keeps solid-state progress visible even before mass commercialization. At the same time, lithium-manganese-rich development at GM and Ford could broaden the future chemistry set before solid-state reaches large-scale production, which means the market is likely to remain mixed rather than settle around a simple two-chemistry structure

Cylindrical cells claimed 51.9% of the North America EV lithium-ion battery market share in 2025, which kept them in the lead across cell formats. The North America EV lithium-ion battery market has favored cylindrical formats because Panasonic built large-scale 2170 production in Nevada and then extended that base through De Soto, Kansas. Tesla's 4680 cell strategy also supports this position because the format is tied to its heavy vehicle and pickup programs, which require high output and a proven domestic manufacturing path. Pouch cells still retain a role where custom packaging and platform-specific layouts matter, and several joint-venture programs continue to use them in passenger EV architectures. That said, the present lead for cylindrical cells does not remove the growing structural appeal of prismatic designs in the North America EV lithium-ion battery market.

Prismatic cells are forecast to expand at 25.3% through 2031, which makes them the fastest-growing format segment. This growth reflects three linked shifts, namely broader LFP adoption, increasing use of cell-to-pack designs, and rising commercial vehicle demand, where modular pack logic is easier to implement with prismatic cells. Volkswagen's PowerCo plant in St. Thomas is being built around the Unified Cell in prismatic format with a targeted 90 GWh annual capacity, which gives the region a major future source of local prismatic output VW.CA. The upcoming USMCA review could further favor producers that already manufacture prismatic cells inside the trade bloc, because rules-of-origin compliance is becoming as important as pure manufacturing scale in the North America EV lithium-ion battery market.

Complete Report Scope:

- By Battery Chemistry

- Lithium-ion (NMC, LFP, NCA)

- Emerging (Solid-state, Li-S, Na-ion)

- Lead-acid

- Nickel-metal-hydride

- By Cell Format

- Cylindrical

- Prismatic

- Pouch

- By Propulsion

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Trucks

- Buses and Coaches

- Two and Three-wheelers

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- LG Energy Solution Ltd

- Panasonic Holdings Corporation

- SK On Co. Ltd

- Contemporary Amperex Technology Co. Ltd (CATL)

- Samsung SDI Co. Ltd

- BYD Company Ltd

- A123 Systems LLC

- EnerSys

- E-One Moli Energy Corp.

- VARTA AG

- Microvast Holdings Inc.

- Farasis Energy Inc.

- Romeo Power Inc.

- Northvolt AB

- Gotion High-Tech Co. Ltd

- Clarios LLC

- Envision AESC Group Ltd

- Tesla Inc. (Cell Manufacturing)

- FREYR Battery

- Solid Power Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery prices

- 4.2.2 Growing EV model availability & purchase incentives

- 4.2.3 Scale-up of North-American cell manufacturing capacity

- 4.2.4 OEM-battery maker long-term offtake agreements

- 4.2.5 Break-throughs in high-silicon anodes (>=2028)

- 4.2.6 Second-life battery leasing models for fleets

- 4.3 Market Restraints

- 4.3.1 Raw-material supply bottlenecks for Class-1 nickel

- 4.3.2 Slow permitting of new North-American lithium projects

- 4.3.3 Recycling regulatory uncertainty beyond California

- 4.3.4 Thermal-runaway reputation risk after high-profile fires

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LG Energy Solution Ltd

- 6.4.2 Panasonic Holdings Corporation

- 6.4.3 SK On Co. Ltd

- 6.4.4 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.4.5 Samsung SDI Co. Ltd

- 6.4.6 BYD Company Ltd

- 6.4.7 A123 Systems LLC

- 6.4.8 EnerSys

- 6.4.9 E-One Moli Energy Corp.

- 6.4.10 VARTA AG

- 6.4.11 Microvast Holdings Inc.

- 6.4.12 Farasis Energy Inc.

- 6.4.13 Romeo Power Inc.

- 6.4.14 Northvolt AB

- 6.4.15 Gotion High-Tech Co. Ltd

- 6.4.16 Clarios LLC

- 6.4.17 Envision AESC Group Ltd

- 6.4.18 Tesla Inc. (Cell Manufacturing)

- 6.4.19 FREYR Battery

- 6.4.20 Solid Power Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment