PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432437

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432437

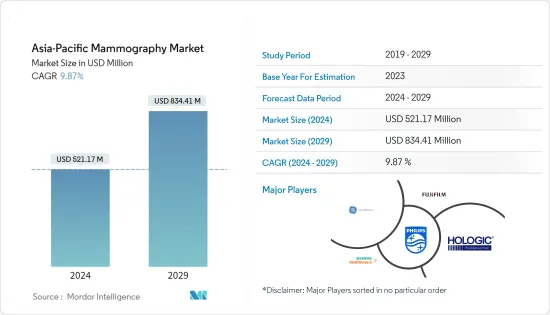

Asia-Pacific Mammography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Asia-Pacific Mammography Market size is estimated at USD 521.17 million in 2024, and is expected to reach USD 834.41 million by 2029, growing at a CAGR of 9.87% during the forecast period (2024-2029).

The major factors contributing to the growth of the Asia-Pacific mammography market are the rising incidence of breast cancer, large R&D investment in breast cancer therapies, and advances in breast imaging modalities. In most Asian countries, breast cancer is the most common cancer. Incidence rates increase at a faster rate than in Western countries due to lifestyle and dietary changes. The Center for Disease Control (CDC) reports breast cancer to be one of the most common cancers among women, irrespective of race or ethnicity. The rising prevalence of breast cancer and the growing healthcare infrastructure in the region is expected to drive the overall growth. As per the GLOBOCAN 2018, the estimated age-standardized incidence rate of breast cancer in Asia is 34.4 per 100,00. The other factors helping the growth of the mammography market are the rapid increase in population.

Asia-Pacific Mammography Market Trends

Digital Mammography Segment is Expected to Hold the Largest Market Share in the Asia-Pacifc Mammography Market

Digital mammography is a specialized and advanced form of mammography that uses digital receptors and computers instead of X-ray films to examine breast tissue for tumor presence. So far, conventional screen-film mammography (SFM) with high-spatial-resolution has been the preferred choice for screening programs in most countries. However, with the advent of digital mammography, an increasing number of countries are experiencing shifts toward these newer systems, due to their superior depiction of low-contrast objects, wider dynamic change, and improved diagnostic quality of images, especially when examining denser breasts. They also come with an added advantage of soft-copy image displays and soft-copy reading, which can be easily transferred. Mammography screening offers greater precision, better quality, and higher efficiency results. Thus, digital mammography is becoming the preferred choice of selection, even though the new technology cost is six times higher than the conventional systems. These factors are expected to contribute to the growth of the market during the forecast period.

Asia-Pacific Mammography Industry Overview

The Asia-Pacific mammography market is competitive and consists of several players. In terms of market share, few of the major players are currently dominating the market. And some prominent players are vigorously making acquisitions and joint ventures with the other companies to consolidate their market positions across the region. Some of the companies which are currently dominating the market are Bayer AG, Pfizer Inc., Merck & Co., Inc., CooperSurgical, Inc., and Allergan PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidences of Breast Cancer

- 4.2.2 Advancements in the Technologies of Breast Imaging Modalities

- 4.3 Market Restraints

- 4.3.1 High Cost of Imaging Devices

- 4.3.2 Risk of Adverse Effects of Radiation Exposure

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Digital Systems

- 5.1.2 Analog Systems

- 5.1.3 Breast Tomosynthesis

- 5.1.4 Film Screen Systems

- 5.1.5 Other Product Types

- 5.2 By End Users

- 5.2.1 Hospitals

- 5.2.2 Diagnostic Centers

- 5.2.3 Others

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 Australia

- 5.3.1.5 South korea

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fujifilm Holdings Corporation

- 6.1.2 Hologic, Inc.

- 6.1.3 Koninklijke Philips N.V.

- 6.1.4 Siemens Healthineers AG

- 6.1.5 GE Healthcare

- 6.1.6 Metaltronica S.p.A.

- 6.1.7 Planmed Oy

- 6.1.8 Konica Minolta, Inc.

- 6.1.9 Carestream Health

- 6.1.10 Canon Medical Systems Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS