PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939599

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939599

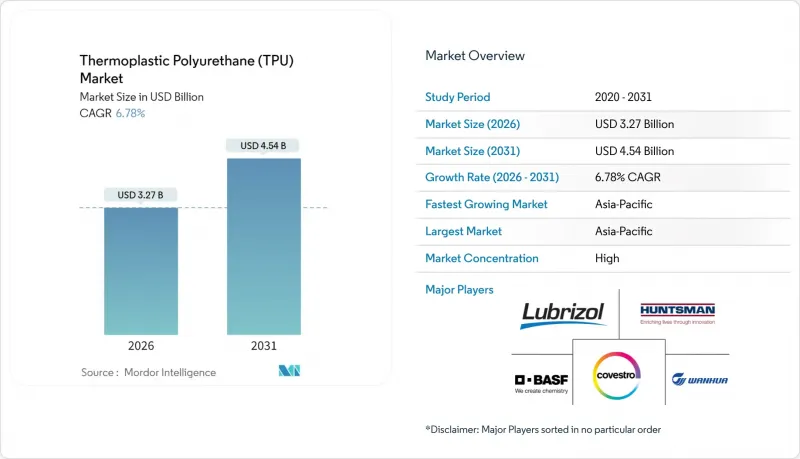

Thermoplastic Polyurethane (TPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Thermoplastic Polyurethane market is expected to grow from USD 3.06 billion in 2025 to USD 3.27 billion in 2026 and is forecast to reach USD 4.54 billion by 2031 at 6.78% CAGR over 2026-2031.

Expanding demand across footwear, automotive, medical devices, and additive manufacturing anchors this growth as converters seek materials that combine elasticity, abrasion resistance, and ease of processing. Polyester grades hold sway because they balance mechanical performance with cost, while bio-based content and closed-loop designs help brands meet sustainability mandates. Rising lightweighting in electric vehicles, strong adoption in wearable health monitors, and increased use of TPU membranes in flexible solar modules further widen the addressable base of the thermoplastic polyurethane market. Regional competitive intensity is highest in Asia-Pacific due to integrated supply chains and sizable downstream capacity, yet North American producers set the pace on regulatory compliance and specialty innovation.

Global Thermoplastic Polyurethane (TPU) Market Trends and Insights

Wearable medical devices

Surging adoption of continuous glucose monitors, smart cardiac patches and next-generation catheters is intensifying the pull for medical-grade TPU. These devices require soft touch, long-term skin compatibility and kink resistance. Avient tripled capacity for its NEUSoft TPU in Suzhou under ISO 13485 certification to localize supply for Asian health-tech manufacturers . Lubrizol and Polyhose followed with a Tamil Nadu tubing plant that scales neurovascular products five-fold . Such vertical investments shorten lead times and lock in material grades that can pass stringent biocompatibility testing, adding momentum to the thermoplastic polyurethane market.

3D-printing filaments & powders

Additive manufacturing reshapes prototype cycles by enabling functional parts that mimic end-use performance. BASF's Ultrasint TPU01 runs on powder-bed fusion platforms with 80% powder recyclability and 88-90 Shore A hardness, delivering energy return suited to lattice midsoles and impact-absorbing automotive ducts. Process stability lowers scrap while recycled powder cuts cost per part, encouraging tier-1 suppliers to integrate TPU into serial production. The resulting design freedom accelerates iteration and supports broader adoption across the thermoplastic polyurethane market.

1,4-BDO feedstock volatility

Polyester and polyether TPU rely on 1,4-butanediol for soft-segment chemistry. Supply disruptions and dual-use regulatory scrutiny raise transaction prices and complicate inventory planning. Chemical distributors report that controlled-substance documentation slows customs clearance, extending lead times during demand spikes. Producers hedge with multi-sourcing strategies and forward contracts but still face margin compression that restrains capacity expansion plans in the thermoplastic polyurethane market.

Other drivers and restraints analyzed in the detailed report include:

- Bio-based mono-material footwear

- PVC-to-TPU shift in membranes

- Tightening isocyanate regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester TPU generated 39.35% of 2025 revenue and is projected to grow at 7.73% CAGR, establishing it as both the largest and fastest segment within the thermoplastic polyurethane market. Robust oil and grease resistance underpins its dominance in hydraulic hoses, wire coatings and dynamic automotive belts. BASF's Elastollan B CF series trims cycle times by 25% and widens hardness coverage from 25 Shore A to 70 Shore D, enabling parts that combine clarity with low-temperature impact strength. The resulting productivity gains improve economic viability for secondary converters.

Polyether TPU sustains demand where hydrolysis resistance is paramount, such as pneumatic tubes and outdoor cables. Polycaprolactone TPU, though smaller, advances in bio-resorbable scaffolds. Electrospun nanofibers mimic extracellular matrices and support controlled drug release, expanding clinical research pipelines. Diversified chemistry assures that the thermoplastic polyurethane market can address divergent performance specifications across industries.

The Thermoplastic Polyurethane Market Report Segments the Industry by Product Type (Polyester TPU, Polyether TPU, Polycaprolactone TPU), Application (Extruded Products, Injection Molded Products, and More), End-User Industry (Footwear, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 57.40% of global revenue in 2025 and is set to compound at 7.55% annually to 2031. China's vertically integrated supply chain secures raw materials, compounding and conversion under one roof, thereby compressing cost to serve. Avient's Suzhou investment localises catheter-grade TPU production, cutting lead times for regional device makers. Concurrently, Lubrizol's Indian tubing project lifts regional capacity five-fold and enhances supply resilience for cardiovascular OEMs.

North America ranks second owing to high adoption in performance sports, medical disposables and specialty films. Regulatory tightening on diisocyanates elevates barriers to entry yet spurs innovation in low-free-isocyanate prepolymers and bio-based carbon routes. Investments in additive manufacturing also advance regional material differentiation, supporting niche growth inside the thermoplastic polyurethane market.

Europe leverages its leadership in circular economy frameworks. Brands favour renewable carbon feedstocks and transparent end-of-life schemes, accelerating demand for biomass-balanced TPU grades. Automotive suppliers in Germany and France integrate TPU seal profiles to meet EU fleet emission targets, while Italian fashion houses adopt solvent-free TPU synthetic leather for luxury accessories.

South America and the Middle East & Africa remain nascent but strategic. Brazilian footwear clusters consume increasing volumes of recyclable TPU pellets, while United Arab Emirates contractors specify TPU roofing membranes to withstand desert UV exposure. Local production remains limited, encouraging multinational producers to establish distribution hubs and technical service centers to penetrate these emerging nodes of the thermoplastic polyurethane market.

- BASF

- Avient Corporation

- Coim Group

- Covestro AG

- Dongsung

- Epaflex Polyurethanes SpA

- Hexpol AB

- Huntsman International LLC

- Miracll Chemicals Co. Ltd

- Mitsui Chemicals Inc.

- Novotex Italiana SpA

- Sumei Chemical Co. Ltd

- Suzhou Austen New Mstar Technology Ltd

- Taiwan PU Corporation

- The Lubrizol Corporation

- Tosoh Corporation

- Trinseo

- Wanhua Chemical Group Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Wearable Medical Devices Driving Medical-Grade TPU Demand

- 4.2.2 3D-Printing Filaments & Powders Accelerating Prototyping Adoption

- 4.2.3 Bio-Based Mono-Material Footwear Programs Boosting Consumption

- 4.2.4 PVC-to-TPU Shift in Flexible Solar & Architectural Membranes

- 4.2.5 Rising Usage in Industrial Applications

- 4.3 Market Restraints

- 4.3.1 1,4-BDO Feedstock Volatility Inflating Polyester/Ether TPU Prices

- 4.3.2 Tightening Isocyanate-Exposure Regulations

- 4.3.3 Displacement Risk from High-Heat TPEE & TPV in Automotive Application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Polyester TPU

- 5.1.2 Polyether TPU

- 5.1.3 Polycaprolactone TPU

- 5.2 By Application

- 5.2.1 Extruded Products

- 5.2.2 Injection Molded Products

- 5.2.3 Adhesives

- 5.2.4 Other Applications

- 5.3 By End-Use Industry

- 5.3.1 Footwear

- 5.3.2 Automotive

- 5.3.3 Medical

- 5.3.4 Electrical & Electronics

- 5.3.5 Construction

- 5.3.6 Heavy Engineering

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global & Market Overview, Core Segments, Financials, Strategy, Rank/Share, Products, Recent Developments)

- 6.3.1 BASF

- 6.3.2 Avient Corporation

- 6.3.3 Coim Group

- 6.3.4 Covestro AG

- 6.3.5 Dongsung

- 6.3.6 Epaflex Polyurethanes SpA

- 6.3.7 Hexpol AB

- 6.3.8 Huntsman International LLC

- 6.3.9 Miracll Chemicals Co. Ltd

- 6.3.10 Mitsui Chemicals Inc.

- 6.3.11 Novotex Italiana SpA

- 6.3.12 Sumei Chemical Co. Ltd

- 6.3.13 Suzhou Austen New Mstar Technology Ltd

- 6.3.14 Taiwan PU Corporation

- 6.3.15 The Lubrizol Corporation

- 6.3.16 Tosoh Corporation

- 6.3.17 Trinseo

- 6.3.18 Wanhua Chemical Group Co. Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

- 7.2 Shifting Focus Toward the Development of Bio-based Products