PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850071

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850071

Packaging Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

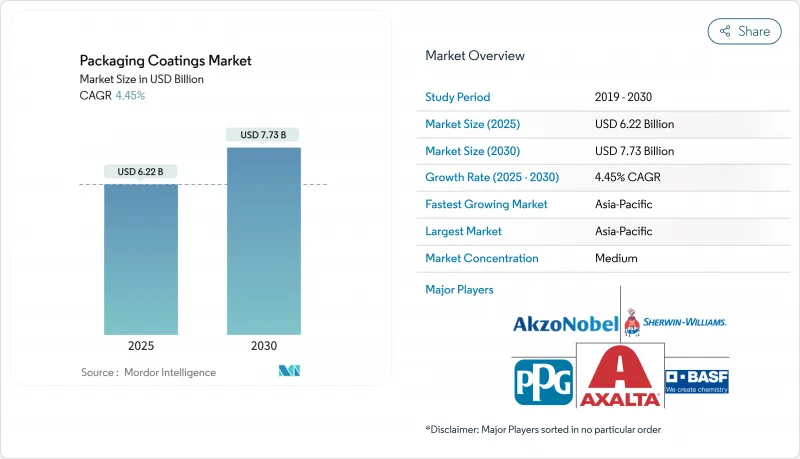

The Packaging Coatings Market size is estimated at USD 6.22 billion in 2025, and is expected to reach USD 7.73 billion by 2030, at a CAGR of 4.45% during the forecast period (2025-2030).Growth is being propelled by tighter global food-contact rules, rapid shifts toward PFAS-free and BPA-free chemistries, and rising consumer demand for premium, visually distinctive packages.

Asia-Pacific remains both the largest and fastest-expanding region, while water-based, UV-curable, and non-BPA epoxy technologies capture share as converters race to meet evolving customer and legislative standards. Rigid formats continue to dominate volumes, yet flexible innovations tied to e-commerce and lightweighting are eroding the historical gap. Cost volatility for epoxy feedstocks and infrastructure gaps in circular-economy logistics temper the otherwise steady advance of the packaging coatings market.

Global Packaging Coatings Market Trends and Insights

BPA-free Can-Lining Mandates Fueling Epoxy-Alternative Demand

The EU Regulation 2024/3190 banning bisphenol A in food-contact materials, effective January 2025, coupled with parallel North-American measures, has created an acute need for compliant internal and external can coatings. Manufacturers are responding by scaling non-BPA chemistries that retain epoxy performance, such as Sherwin-Williams' valPure V70 and Akzo Nobel's Accelshield 700. Fillers and brand owners are qualifying these systems well ahead of the 18-month transition window granted for internal linings, driving brisk adoption across metal packaging lines in both continents.

Craft Beverage Boom in Asia Accelerating UV-Curable Varnish Uptake

Independent breweries across India, China, and Southeast Asia seek vibrant graphics and scratch-free finishes that differentiate cans on crowded shelves. UV-curable overprint varnishes deliver instant cure, high gloss, and line-speed productivity benefits, pushing their technology CAGR around 5.01%. ACTEGA's new WESSCO UV facility in Maharashtra illustrates how local capacity expansion supports brand schedules while reducing lead times.

Epoxy Resin Price Volatility Pressuring Margins

Supply-chain disruptions, energy price swings, and feedstock tightness have pushed epoxy costs to multi-year highs. Because epoxies underpin half of the packaging coatings market, even minor price spikes widen cost-pass-through gaps for can-makers and fillers. PPG, for example, has accelerated raw-material hedging and productivity programs to soften earnings exposure.

Other drivers and restraints analyzed in the detailed report include:

- GCC E-Grocery Growth Boosting Scuff-Resistant Cap & Closure Coatings

- Europe PFAS Phase-Out Driving Water-Based Barrier Coatings for Paperboard

- Weak Recycling Streams Slowing Bio-Barrier Adoption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy systems accounted for 51% of packaging coatings market share in 2024, underlining their unrivaled adhesion, heat resistance and chemical barrier attributes. The packaging coatings market size tied to epoxies is set to grow on a 4.7% CAGR as suppliers commercialize non-BPA variants that satisfy both regulatory scrutiny and filler performance thresholds. Sherwin-Williams' valPure V70 and PPG's HobaPro 2848 exemplify this middle-path approach, preserving line efficiency while eliminating endocrine-disruptor concerns.

Acrylic and polyurethane chemistries now capture applications requiring lower VOC profiles or higher flexibility, respectively. Polyolefins serve heat-seal foil lids, whereas polyester networks bring solvent resistance to D&I beverage cans. Bio-derived resins, although still niche, post double-digit gains as brand owners test cellulose, terpene and polysaccharide matrices for snack flexibles and single-use cup stock.

Epoxy price swings described in the restraints scenario keep purchasing managers alert to substitution opportunities; nonetheless, end-users rarely abandon the class outright because retrofitting lines entails downtime and retesting. Consequently, hybrid strategies emerge: thin epoxy primers topped with acrylic or polyester overcoats reduce overall bisphenol exposure while retaining core advantages. Over the forecast window, incremental reformulation rather than wholesale replacement is expected to preserve epoxy primacy without breaching tightening migration limits.

Water-based products held 43% revenue in 2024 as converters chased lower VOCs and simpler permitting. The packaging coatings market size for water-based lines is forecast to rise steadily, helped by European PFAS policies that incentivize aqueous barrier science. Film stability advances such as PUD #65215A shorten drying curves and allow thicker films, narrowing historical productivity gaps versus solvent routes.

UV-curable technology registers the highest 5.01% CAGR thanks to instant-cure economics and minimal oven infrastructure. Asia-Pacific mobile canning lines now adopt UV spot-varnish units to enable short-run labels for craft brewers, highlighting the versatility of the platform. Solvent-borne nitrocellulose or epoxy systems still dominate retort foods needing extreme chemical resistance, but ongoing air-quality caps in California and the EU limit incremental growth. Powder coatings, although a smaller base, earn share in welded aerosol cans by offering zero VOCs and superb edge coverage, reinforcing the green-chemistry narrative that underscores competition within the packaging coatings market.

Technology selection is increasingly multivariate-balancing cure speed, energy, migration limits, odor, recyclability and total applied cost. Formulators now integrate AI-guided design of experiments to optimize ingredient matrices, accelerating time-to-market while cutting lab emissions. The resulting pipeline of hybrid chemistries-water-based UV, energy-curable powders and high-solid polyesters-suggests that technology lines will blur, yet the overall packaging coatings market will pivot toward platforms with verifiable life-cycle advantages.

The Packaging Coatings Market Report Segments the Industry by Resin (Epoxies, Acrylics, and More), Coating Technology (Water-Based, Solvent-Based, and More), Packaging Type (Rigid and Flexible), Application (Food Cans, Beverage Cans, and More), End-User Industry (Food and Beverage, Industrial Goods, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific led the packaging coatings market with a 43% revenue share in 2024 and the highest 4.73% CAGR outlook. China's beverage can production, India's craft-beer rise and Southeast Asia's snack export boom combine to deliver unrivaled volume growth. Regional authorities also fast-track low-VOC mandates, pushing domestic firms to license Western water-borne know-how while investing in local UV resin synthesis capacity. Multinationals such as Amcor are expanding medical-pack plants to tap the fastest-growing healthcare sub-segment, reinforcing Asia-Pacific's centrality.

North America ranks second, buoyed by high per-capita beverage consumption and widespread adoption of premium finishes such as matte-varnish soft-touch. The FDA's alignment with EU PFAS restrictions accelerates label-change cycles, driving incremental demand for compliant alternatives. Beyond canning, North American e-commerce penetration lifts the need for impact-resistant pouches and scuff-proof lids, extending the regional scope of the packaging coatings market.

Europe experiences regulatory-induced transformation rather than volume surge. The BPA ban effective January 2025 and looming PFAS prohibition are compelling rapid technology swaps, evident in Akzo Nobel's EUR 32 million Spanish plant scheduled for mid-2025 start-up. Although economic sluggishness tempers unit volume growth, technology value-add per ton rises, partially offsetting slower can counts. Meanwhile, the Middle East and Africa benefit from rising disposable incomes and GCC warehousing infrastructure, while South America sees beverage-sector resilience amid economic swings, continuing to offer selective upside for coating exporters.

- Akzo Nobel N.V.

- ALTANA

- artience Co., Ltd.

- Axalta Coating Systems LLC

- BASF SE

- DIC Corporation

- Dow

- H.B. Fuller Company

- Hempel A/S

- Henkel AG & Co. KGaA

- Jamestown Coating Technologies

- Jotun

- KANGNAM JEVISCO CO., LTD.

- Kansai Paint Co., Ltd.

- Michelman, Inc.

- PPG Industries Inc.

- RPM International Inc.

- Silgan Holdings Inc.

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 BPA-free Can Lining Mandates Fueling Epoxy-Alternative Demand in North America and Europe

- 4.2.2 Craft Beverage Boom in Asia Accelerating UV-Curable Varnish Uptake

- 4.2.3 GCC E-grocery Growth Boosting Scuff-Resistant Cap and Closure Coatings

- 4.2.4 Europe PFAS Phase-out Driving Water-based Barrier Coatings for Paperboard

- 4.2.5 Growing Utilization of Packaging Coatings in Aerosol Cans for Personal Care Industry

- 4.3 Market Restraints

- 4.3.1 Epoxy Resin Price Volatility Pressuring Margins Across Regions

- 4.3.2 Weak Recycling Streams Slowing Bio-barrier Adoption

- 4.3.3 Stringent Regulation and Environmental Concern Regarding VOC Emission

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Epoxies

- 5.1.2 Acrylics

- 5.1.3 Polyurethane

- 5.1.4 Polyolefins

- 5.1.5 Polyester

- 5.1.6 Other Resins

- 5.2 By Coating Technology

- 5.2.1 Water-based

- 5.2.2 Solvent-based

- 5.2.3 Powder

- 5.2.4 UVcurable

- 5.3 By Packaging Type

- 5.3.1 Rigid (Cans, Caps and Closures)

- 5.3.2 Flexible (Pouches, Films, Sachets)

- 5.4 By Application

- 5.4.1 Food Cans

- 5.4.2 Beverage Cans

- 5.4.3 Aerosol and Tubes

- 5.4.4 Caps and Closures

- 5.4.5 Industrial and Specialty Packaging

- 5.5 By End-User Industry

- 5.5.1 Food and Beverage

- 5.5.2 Personal Care and Cosmetics

- 5.5.3 Healthcare and Pharmaceutical

- 5.5.4 Industrial Goods

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Indonesia

- 5.6.1.6 Malaysia

- 5.6.1.7 Thailand

- 5.6.1.8 Vietnam

- 5.6.1.9 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Turkey

- 5.6.3.8 Russia

- 5.6.3.9 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Qatar

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Nigeria

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 ALTANA

- 6.4.3 artience Co., Ltd.

- 6.4.4 Axalta Coating Systems LLC

- 6.4.5 BASF SE

- 6.4.6 DIC Corporation

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Hempel A/S

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Jamestown Coating Technologies

- 6.4.12 Jotun

- 6.4.13 KANGNAM JEVISCO CO., LTD.

- 6.4.14 Kansai Paint Co., Ltd.

- 6.4.15 Michelman, Inc.

- 6.4.16 PPG Industries Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Silgan Holdings Inc.

- 6.4.19 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growing Inclination for Eco-Friendly Packaging Coatings