PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444623

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444623

Telemedicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

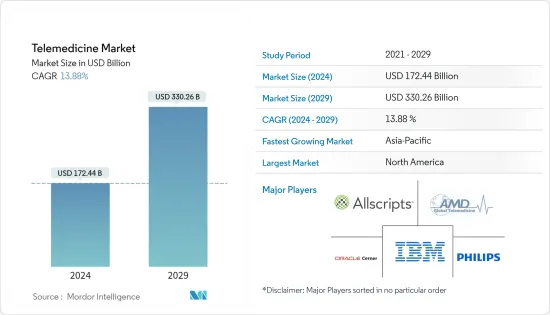

The Telemedicine Market size is estimated at USD 172.44 billion in 2024, and is expected to reach USD 330.26 billion by 2029, growing at a CAGR of 13.88% during the forecast period (2024-2029).

Telehealth has emerged as an essential component of healthcare during the COVID-19 pandemic. Though telemedicine services were integrated into most healthcare systems even before the onset of the pandemic, services began to be extensively used only during the COVID-19 crisis. An article published in October 2021, by Foundation for Research and Technology Greece, explained that during the pandemic, COVID-19 served as a catalyst and accelerator for digital healthcare innovation. Regulators worked to eliminate data silos in artificial intelligence and digital health to better promote innovation. Furthermore, the United States has approved legislation to allow for more seamless data flow, while the European Union integrated the data across member states to permit the interchange of electronic health records (EHRs) across borders during the pandemic. Additionally, according to a study published in Health Affairs, in September 2022, during the COVID-19 pandemic, a small percentage of primary care doctors were responsible for the more than 4-fold rise in the usage of remote patient monitoring (RPM). Telemedicine solutions have demonstrated the ability to enhance health outcomes during a high-stress period like the COVID-19 pandemic and being integrated with conventional healthcare services which are expected to further increase the demand for telemedicine services.

The major factors for the growth of the telemedicine market include rising healthcare expenditure, technological innovations and rising demand for remote patient monitoring, and the growing burden of chronic diseases. For instance, according to the UK Health Accounts provisional estimates, the 2021 report, published in May 2022, the total current healthcare expenditure in 2021 was estimated at GBP 277 billion (USD 317 billion), which is an increase in nominal terms of 7.4% on spending in 2020. Furthermore, as per the 2022 update from the Canadian Institute for Health Information, hospitals (24.34%), physicians (13.60%), and drugs (13.58%) categories continued to account for the largest shares, which is over half of the total health spending in 2022. As the cost of in-person consultation is much more tedious and costly as compared to an online consultation and hence telemedicine gained traction. This is likely to boost the growth of the market studied over the forecast period.

Furthermore, according to CDC, in 2021, around 18.2 million adults aged 20 and older had coronary artery disease (CAD) in the United States. Heart disease is the leading cause of death in the United States. Also, as per the 2022 update from the International Diabetic Federation (IDF), approximately 537 million adults (20-79 years) are living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The high incidence of chronic diseases increases the demand for huge telemedicine, which, in turn, drives the market.

Thus, the abovementioned factors are impacting the market growth of the telemedicine market. However, legal and reimbursement issues and high initial capital requirements, and lack of physician support are expected to hinder market growth over the forecast period.

Telemedicine Market Trends

Tele homes Segment is Expected to Witness a Significant Growth Over the Forecast Period

Tele homes involve delivering healthcare services to clients in their own homes. The rise of chronic diseases is a global concern that strains healthcare resources. Tele-homecare is an innovative way to provide care, monitor a patient, and provide information using the latest technology. Monitoring allows early identification of diseases and provides aid in emergencies. Hence, the use of tele home services is increasing. For instance, according to an article published by JMIR Publications, in January 2022, children and their families chose pediatric tele home care since it is 9% less expensive than traditional hospital care, freeing up hospital beds for more complicated situations in Spain.

Further, people prefer tele home at home rather than visiting a hospital for treatment owing to greater convenience and reduction in overall cost. For instance, according to an article published by the Partnership for Quality Home Healthcare, in 2021, some 86% of adults preferred to receive "post-hospital, short-term healthcare" at home, while only 5% preferred nursing homes in the United States. Tele home services provide an opportunity for significant savings for patients and hospitals. Thus, the increasing adoption rate of tele homes services is directly affecting the growth of the telemedicine market. Therefore, factors such increase adoption rate and low cost of tele home are expected to drive segmental growth in the market during the forecast period.

North America is Expected to Dominate the Telemedicine Market Over the Forecast Period

Telemedicine is a rapidly growing component of healthcare in the United States due to the growing burden of chronic diseases and the high adoption of advanced healthcare technologies. The adoption of telemedicine has improved care management, patients' quality of life, and reduced healthcare spending. Furthermore, the rising demand for mobile technologies, rising home care adoption by patients, increased healthcare expenditure, and reduction in hospital visits are expected to propel the market's growth over the forecast period. For instance, according to the 2021 report from the Canadian Institute of Health Information, Canadian health expenditure increased to USD 308.1 billion in 2021 compared to USD 301.5 billion in 2020. Similarly, as per the 2022 report of the Centers for Medicare and Medicaid Services (CMS), the health expenditure of the United States was about USD 4.3 trillion, an increase of about USD 173 billion from the previous year. Thus, the increasing healthcare spending is anticipated to create opportunities for telemedicine, thereby propelling the market growth.

Additionally, companies are engaged in partnerships, collaborations, acquisitions, mergers, and product launches to innovate in the telemedicine market driving growth in the forecast period. For instance, in April 2021, Inova Health System in the Northern Virginia and Washington DC area, United States, offered an FDA-approved telemedicine option for remote neuromodulation of deep brain stimulation (DBS) patients being treated for Parkinson's disease and essential tremor. Also, in August 2022, Hicuity Health launched tele-ICU services at MUSC Health Columbia Medical Center Downtown in Columbia, South Carolina. Therefore, such development is expected to drive the market. Thus, given the factors above, the telemedicine market is expected to grow significantly in North America over the forecast period.

Telemedicine Industry Overview

The Telemedicine Market is fragmented in nature due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies which hold market shares and are well known including Allscripts Healthcare Solutions Inc., BioTelemetry, Medtronic, Koninklijke Philips NV, Aerotel Medical Systems (1998) Ltd, AMD Global Telemedicine Inc., and SOC Telemed, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Healthcare Expenditure

- 4.2.2 Technological Innovations and Rising Demand for Remote Patient Monitoring

- 4.2.3 Growing Burden of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 Legal and Reimbursement Issues

- 4.3.2 High Initial Capital Requirements and Lack of Physician Support

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 By Type

- 5.1.1 Tele hospitals

- 5.1.2 Tele homes

- 5.1.3 mHealth (Mobile Health)

- 5.2 By Component

- 5.2.1 Products

- 5.2.1.1 Hardware

- 5.2.1.2 Software

- 5.2.1.3 Other Products

- 5.2.2 Services

- 5.2.2.1 Telepathology

- 5.2.2.2 Telecardiology

- 5.2.2.3 Teleradiology

- 5.2.2.4 Teledermatology

- 5.2.2.5 Telepsychiatry

- 5.2.2.6 Other Services

- 5.2.1 Products

- 5.3 By Mode of Delivery

- 5.3.1 On-premise Delivery

- 5.3.2 Cloud-based Delivery

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 US

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 UK

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems (1998) Ltd

- 6.1.2 IBM

- 6.1.3 Allscripts Healthcare Solutions Inc.

- 6.1.4 AMD Global Telemedicine Inc.

- 6.1.5 SOC Telemed

- 6.1.6 Resideo Technologies Inc.

- 6.1.7 Koninklijke Philips NV

- 6.1.8 Medtronic PLC

- 6.1.9 SHL Telemedicine

- 6.1.10 Teladoc Health Inc. (InTouch Technologies Inc.)

- 6.1.11 Cerner Corporation

- 6.1.12 Cisco System

7 MARKET OPPORTUNITIES AND FUTURE TRENDS