PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444783

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444783

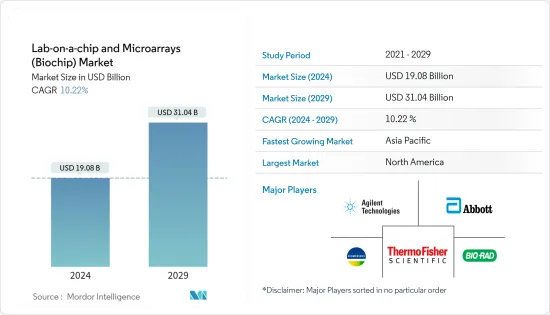

Lab-on-a-chip and Microarrays (Biochip) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Lab-on-a-chip and Microarrays Market size is estimated at USD 19.08 billion in 2024, and is expected to reach USD 31.04 billion by 2029, growing at a CAGR of 10.22% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the lab-on-a-chip and microarrays (biochips) market. For instance, an article published by the journal Nature Communication in January 2021 reported that this microarray could be used as a diagnostic tool, as an epidemiologic tool to estimate the disease burden of COVID-19 more accurately, and as a research tool to correlate antibody responses with clinical outcomes. Thus, the COVID-19 pandemic increased the demand for lab-on-a-chip diagnostic tools. However, in the current scenario, it is anticipated that with the presence of other chronic and infectious diseases, the demand for the studied market is expected to increase over the forecast period.

The factors driving the growth of the studied market are increasing demand for point-of-care testing, increasing incidences of chronic diseases, and increasing application of proteomics and genomics in cancer research. Most market players are focusing on the development of new and technologically advanced diagnostic tests. Chronic diseases are the leading cause of death and disability across the world. For instance, an article published by the journal Plos One in March 2022 reported that 21% of the elderly in India had at least one chronic disease. Chronic diseases are the leading causes of disability and mortality among the elderly population in India.

Similarly, another article published by European Public Health Conference in January 2022 reported that more than 3 million people will be affected by cancer by 2030 in Europe. Globally, chronic diseases (CDs) are found to be the leading causes of disability and morbidity. Since those diseases are chronic, accurate and timely clinical decision-making is required. In this direction, research toward developing new lab-on-a-chip-based POC systems for the diagnosis of chronic diseases is an emerging area. Thus, a high incidence of chronic diseases is expected to drive the growth of the studied market.

Biochips are increasingly being used in the field of biomedical and biotechnological research. With the advancement of technologies, there has been a rise in the adoption of biochips in proteomics. The advantages of protein biochips are the low sample consumption due to their inclination toward miniaturization. These characteristics of microarrays are important for proteome-wide analysis. Proteomics is being widely adopted for biomarker and drug discoveries. For instance, in April 2021, PathogenDx Inc. reported that the USFDA had issued an Emergency Use Authorization (EUA) for its patented COVID-19 multiplexed viral diagnostic assay, DetectX-Rv. DetectX-Rv is an RT-PCR and DNA microarray hybridization test intended for the qualitative detection of nucleic acids from SARS-CoV-2 swabs. Thus, such approvals for new products are also contributing to the growth of the studied market.

Thus, due to the increasing demand for point-of-care testing, increasing incidences of chronic diseases, and increasing application of proteomics and genomics in cancer research, the studied market is expected to witness significant growth over the forecast period. However, the design constraints of lab-on-chip technology and the availability of alternative technologies may slow down the growth of the studied market.

Lab-on-a-chip and Microarrays Market Trends

Lab-on-a-chip Segment Expected to Witness Significant Growth over the Forecast Period

The lab-on-a-chip (LOC) segment is expected to have positive market growth due to the increasing number of chronic diseases and rising technological advancements. There is also a rise in the adoption of personalized medicine and easy accessibility of lab-on-chip technology, which will boost the demand for the same across the world. Also, there are various applications of LOC that are growing rapidly. Lab-on-a-chip devices equipped with electrodes for particle or cell detection, particle packing, sorting, electrophoresis, PCR, etc., are commercially available.

With the increasing number of COVID-19 cases, there is a growing number of research studies to treat and prevent this disease. This has boosted the demand for labs-on-a-chip. For instance, in January 2021, researchers at the University of Alberta joined forces to develop a handheld LOC device for the rapid detection of COVID-19 antibodies. Also, a low-cost imaging platform utilizing the lab-on-a-chip technology created by the University of California by Irvine scientists may be available for rapid coronavirus diagnostic and antibody testing.

Furthermore, the market has witnessed frequent developments in lab-on-a-chip (LOC) platform-based immunoassays. Such advanced LOC platforms include microfluidic chips, paper, lateral flow, electrochemistry, and new biosensor concepts. The rapid increase in demand for point-of-care diagnosis is the most prominent driver expected to propel the segment during the forecast period. For instance, in February 2022, Onera Health launched the Onera Biomedical-Lab-on-Chip, an ultra-low-power biosignal sensor subsystem for wearable devices. This biomedical compact chip is designed to process multiple biosignals, which creates a massive opportunity for health devices. Thus, such developments are propelling the growth of this segment.

Thus, due to the increasing number of chronic diseases, rising technological advancements, rise in the adoption of personalized medicine, and easy accessibility of lab-on-chip technology, the segment is expected to witness significant growth over the forecast period.

North America Expected to Witness a Significant Growth Over the Forecast Period

North America is expected to witness significant growth over the forecast period owing to the presence of key market players in the region and the development of healthcare infrastructure. In addition, the region has witnessed major collaborative activities with healthcare giants that are extensively investing in R&D in microarray technology. For instance, in September 2022, Illumina Inc. launched the NovaSeq X Series, new production-scale sequencers, enabling faster, more powerful, and more sustainable sequencing. This revolutionary new technology, NovaSeq X Plus can generate more than 20,000 whole genomes per year, 2.5 times the throughput of prior sequencers, greatly accelerating genomic discovery and clinical insights to understand the disease and ultimately transform patient lives. Thus, such developments in the region are driving the growth of the studied market.

The field of point-of-care (POC) diagnostics also widely uses microfluidic technology for various applications, like molecular diagnostics, infectious diseases, and chronic diseases, in resource-limited settings. For instance, an article published by the journal Frontiers of Bioengineering and Biotechnology in January 2021 reported that Lateral Flow Assays (LFAs) were widely being used in POC testing and can be used for diagnosis and prognosis of diseases like cancer by identifying specific biomarkers. LFAs have widely been used to detect an array of pathogens and proteins via antibody and nucleic acid amplification. Thus, the latest advances in the research in microfluidics aim to produce integrated devices that are self-contained, automated, easy to use, and rapid.

Moreover, the high incidence of chronic diseases reported in the region is also contributing to the growth of this segment. For instance, as per the Canadian Cancer Statistics released in November 2021 reported that an estimated 229,200 Canadians were diagnosed with cancer in 2021. Similarly, according to the International Diabetes Federation (IDF) published, in 2021, an estimated 14 million adults in Mexico were living with diabetes. Thus, such a high number of people living with chronic diseases in the region is also contributing to the growth of the studied market in the region.

Over the last few years, the interest in high throughput screening (HTS) technologies within academic research has increased drastically in the United States. For instance, in October 2022, Ginkgo Bioworks entered into a collaboration with Merck to engineer up to four enzymes for use as biocatalysts in Merck's active pharmaceutical ingredient (API) manufacturing efforts. Through this collaboration, Ginkgo is to leverage its extensive experience in cell engineering and enzyme design, as well as its capabilities in automated high throughput screening, manufacturing process development/optimization, bioinformatics, and analytics to deliver optimal strains for expression of targeted biocatalysts.

Thus, due to the presence of key market players in the region, the increase in chronic diseases, and the development of healthcare infrastructure, the region is expected to witness significant growth over the forecast period.

Lab-on-a-chip and Microarrays Industry Overview

The lab-on-a-chip and microarrays (biochip) market is moderately competitive, with the presence of a few companies operating globally and regionally. Some of the largest market players include Abbott Laboratories, Agilent Technologies Inc., Bio-Rad Laboratories Inc., Danaher Corporation (Cepheid), Fluidigm Corporation, Thermo Fisher Scientific Inc., PerkinElmer Inc., Micronit BV, Illumina Inc., Phalanx Biotech Group Inc., BioMerieux SA, Qiagen NV, and Merck Kommanditgesellschaft auf Aktien.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Point-of-care Testing

- 4.2.2 Increasing Incidences of Chronic Diseases

- 4.2.3 Increasing Application of Proteomics and Genomics in Cancer Research

- 4.3 Market Restraints

- 4.3.1 Design Constraints of Lab-on-chip Technology

- 4.3.2 Availability of Alternative Technologies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Lab-on-a-chip

- 5.1.2 Microarray

- 5.2 By Products

- 5.2.1 Instruments

- 5.2.2 Reagents and Consumables

- 5.2.3 Software and Services

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Drug Discovery

- 5.3.3 Genomics and Proteomics

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Biotechnology and Pharmaceutical Companies

- 5.4.2 Hospitals and Diagnostic Centers

- 5.4.3 Academic and Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle-East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Agilent Technologies Inc.

- 6.1.3 Bio-Rad Laboratories Inc.

- 6.1.4 Danaher Corporation (Cepheid)

- 6.1.5 Fluidigm Corporation

- 6.1.6 Thermo Fisher Scientific Inc.

- 6.1.7 PerkinElmer Inc.

- 6.1.8 Micronit BV

- 6.1.9 Illumina Inc.

- 6.1.10 Phalanx Biotech Group Inc.

- 6.1.11 BioMerieux SA

- 6.1.12 Qiagen NV

- 6.1.13 Merck Kommanditgesellschaft auf Aktien

7 MARKET OPPORTUNITIES AND FUTURE TRENDS