PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852027

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852027

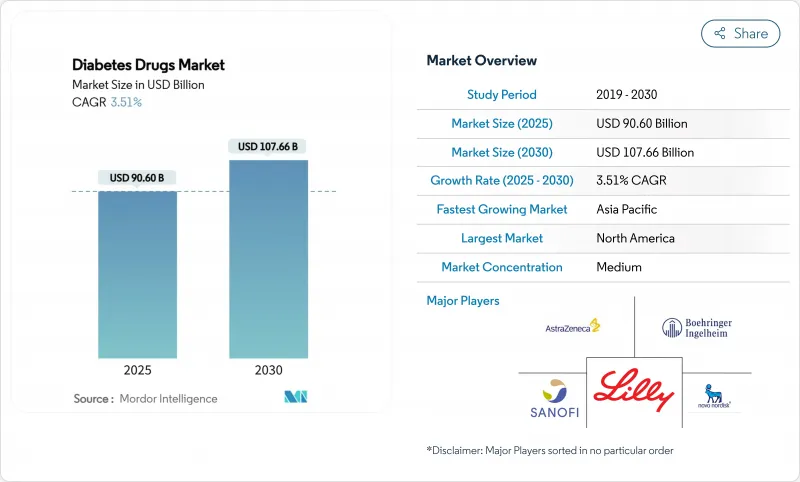

Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Diabetes Drugs Market size is estimated at USD 90.60 billion in 2025, and is expected to reach USD 107.66 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

Sustained growth is rooted in the accelerating global diabetes burden, earlier diagnosis, and rapid uptake of innovative therapies that combine glycemic control with weight-management benefits. Insulin remains indispensable, yet demand is tilting toward GLP-1 receptor agonists and other non-insulin injectables that improve cardiometabolic outcomes . Oral peptide technologies, biosimilar basal insulins, and digitally enabled care models are widening patient access while tempering costs. Competitive intensity is high as incumbents scale manufacturing and digital ecosystems to defend share in an increasingly value-driven environment.

Global Diabetes Drugs Market Trends and Insights

Escalating Global Diabetes Prevalence and Early Diagnosis

More than 828 million adults were living with diabetes in 2024, quadruple the 1990 level. Earlier screening programs in lower-income regions are enlarging the treated population and lengthening therapy duration . New WHO guidance endorsing earlier use of GLP-1 agonists signals tighter integration of advanced injectables into first-line care. The overlap between obesity and diabetes further amplifies demand because many GLP-1 drugs now carry dual indications. These shifts collectively underpin long-run volume growth for the diabetes drugs market.

Rising Healthcare Expenditures

Pharmaceutical spending on diabetes climbed 19% in 2023, outpacing overall health inflation . As per diabetes market research, payers are funding costlier therapies because lower complication rates offset near-term outlays. Employer health plans face mounting pressure, driving tighter utilization management yet preserving access to high-value medicines. This spending momentum sustains price realization even as unit costs come under scrutiny, benefiting innovative products that demonstrate clear clinical and economic returns.

Safety Concerns on GLP-1-Linked Pancreatitis

Isolated pancreatitis reports have prompted enhanced pharmacovigilance and conservative patient selection. Although incidence rates remain low, prescriber caution may slow uptake in high-risk cohorts, moderating the meteoric rise of GLP-1 sales. Manufacturers are supporting education and post-marketing surveillance to safeguard benefit-risk profiles.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Biosimilar Basal Insulins

- Rise of Combination Fixed-Dose Pens Enhancing Adherence

- Public-Sector Price Caps on Insulin Analogues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insulin maintained a 55% share of the diabetes drugs market in 2024, underscoring its central role in both Type 1 and advanced Type 2 management. However, GLP-1 receptor agonists are expanding at a 4.5% CAGR, propelled by weight-loss efficacy that broadens prescribing beyond traditional glycemic control. The diabetes drugs market size for GLP-1 products is projected to reach USD 150 billion by 2030, reflecting their dual-indication appeal. Oral SGLT-2 inhibitors continue to gain favor, supported by organ-protective data that positions them as valuable adjuncts or alternatives to injectables in the diabetes treatment market.

Competitive dynamics within this segment are intense. Novo Nordisk and Eli Lilly currently hold an estimated near-total share, yet a pipeline of dual and triple agonists promises fresh competition. Fixed-dose combinations, such as insulin degludec / liraglutide pens, illustrate how delivery innovation can lock in adherence benefits and extend product life cycles within the diabetes drugs industry.

The Diabetes Drug Market Report Segments the Industry Into by Drugs (Oral Anti-Diabetic Drugs, Insulin, and More), Route of Administration (Oral, Subcutaneous, and Intravenous), Distribution Channel (Online Pharmacies, and Offline), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained leadership with a 42% contribution to 2024 revenue. Broad insurance coverage, strong specialty-care infrastructure, and early adoption of GLP-1 agents underpin regional dominance. Insulin affordability legislation has also stimulated unit demand by lowering patient cost exposure, even as it constrains price expansion. Employers are refining prior-authorization protocols to manage GLP-1 growth, but sustained clinical value is preserving broad access.

Asia-Pacific is the fastest-growing territory, registering a projected 5.3% CAGR from 2025-2030. Rising urbanization, dietary shifts, and aging populations are driving a steep rise in Type 2 prevalence. Expanded insurance benefits in China and India are widening access to branded insulins and novel injectables. Digital health tools and mob ile platforms are bridging care-delivery gaps, supporting adherence and continuity for patients in remote areas. The diabetes drugs market size in Asia-Pacific is therefore expected to close part of the gap with entrenched Western markets by 2030.

Europe presents a mature but evolving landscape shaped by robust biosimilar frameworks and value-assessment bodies that scrutinize cost-effectiveness. High biosimilar penetration is pressuring originator pricing, yet uptake of combination devices and advanced GLP-1 agents is supporting revenue resilience. Emerging markets in the Middle East and Latin America add incremental opportunity as governments commit funds to address escalating diabetes prevalence and as multinational firms localize manufacturing and distribution.

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- AstraZeneca

- Merck

- Bristol-Myers Squibb

- Boehringer Ingelheim

- Pfizer

- Johnson & Johnson

- Novartis

- Biocon

- Teva Pharmaceutical Industries

- Mylan (Viatris)

- Hualan Biologicals

- Tonghua Dongbao

- Wockhardt

- Gan & Lee Pharmaceuticals

- Hanmi Pharmaceutical

- Mitsubishi Tanabe Pharma

- Sun Pharmaceuticals Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Diabetes Prevalence and Early Diagnosis

- 4.2.2 Rising Healthcare Expenditures

- 4.2.3 Rise of Combination Fixed-Dose Pens Enhancing Adherence

- 4.2.4 Strong outcome-based clinical evidence and guideline endorsements for innovative classes

- 4.2.5 Growing Adoption of Biosimilar Basal Insulins

- 4.2.6 Digital Therapeutic Bundling (App + Drug) Boosting Prescription Renewals

- 4.3 Market Restraints

- 4.3.1 Safety Concerns on GLP-1-Linked Pancreatitis

- 4.3.2 Public-Sector Price Caps on Insulin Analogues

- 4.3.3 Cold-Chain Infrastructure Gaps Limiting Uptake i

- 4.3.4 Affordability of Drugs in Emerging Economies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Drugs

- 5.1.1 Oral Anti-diabetic Drugs

- 5.1.1.1 Biguanides

- 5.1.1.1.1 Metformin

- 5.1.1.2 Alpha-glucosidase Inhibitors

- 5.1.1.3 Dopamine-D2 Receptor Agonist

- 5.1.1.3.1 Cycloset (Bromocriptine)

- 5.1.1.4 SGLT-2 Inhibitors

- 5.1.1.4.1 Invokana (Canagliflozin)

- 5.1.1.4.2 Jardiance (Empagliflozin)

- 5.1.1.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.1.1.4.4 Suglat (Ipragliflozin)

- 5.1.1.5 DPP-4 Inhibitors

- 5.1.1.5.1 Januvia (Sitagliptin)

- 5.1.1.5.2 Onglyza (Saxagliptin)

- 5.1.1.5.3 Tradjenta (Linagliptin)

- 5.1.1.5.4 Vipidia/Nesina (Alogliptin)

- 5.1.1.5.5 Galvus (Vildagliptin)

- 5.1.1.6 Sulfonylureas

- 5.1.1.7 Meglitinides

- 5.1.2 Insulin

- 5.1.2.1 Basal / Long-acting

- 5.1.2.1.1 Lantus (Insulin Glargine)

- 5.1.2.1.2 Levemir (Insulin Detemir)

- 5.1.2.1.3 Toujeo (Insulin Glargine)

- 5.1.2.1.4 Tresiba (Insulin Degludec)

- 5.1.2.1.5 Basaglar (Insulin Glargine)

- 5.1.2.2 Bolus / Fast-acting

- 5.1.2.2.1 NovoRapid/Novolog (Insulin Aspart)

- 5.1.2.2.2 Humalog (Insulin Lispro)

- 5.1.2.2.3 Apidra (Insulin Glulisine)

- 5.1.2.3 Traditional Human Insulin

- 5.1.2.3.1 Novolin/Actrapid/Insulatard

- 5.1.2.3.2 Humulin

- 5.1.2.3.3 Insuman

- 5.1.2.4 Biosimilar Insulin

- 5.1.2.4.1 Insulin Glargine Biosimilars

- 5.1.2.4.2 Human Insulin Biosimilars

- 5.1.3 Non-insulin Injectable Drugs

- 5.1.3.1 GLP-1 Receptor Agonists

- 5.1.3.1.1 Victoza (Liraglutide)

- 5.1.3.1.2 Byetta (Exenatide)

- 5.1.3.1.3 Bydureon (Exenatide)

- 5.1.3.1.4 Trulicity (Dulaglutide)

- 5.1.3.1.5 Lyxumia (Lixisenatide)

- 5.1.3.2 Amylin Analogue

- 5.1.3.2.1 Symlin (Pramlintide)

- 5.1.4 Combination Drug

- 5.1.4.1 Combination Insulin

- 5.1.4.1.1 NovoMix (Biphasic Insulin Aspart)

- 5.1.4.1.2 Ryzodeg (Insulin Degludec + Aspart)

- 5.1.4.1.3 Xultophy (Insulin Degludec + Liraglutide)

- 5.1.4.2 Oral Combination

- 5.1.4.2.1 Janumet (Sitagliptin + Metformin)

- 5.1.1 Oral Anti-diabetic Drugs

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Subcutaneous

- 5.2.3 Intravenous

- 5.3 By Distribution Channel

- 5.3.1 Online Pharmacies

- 5.3.2 Offline (Hospital & Retail Pharmacies)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Market Indicators

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company profiles ((includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 Novo Nordisk

- 7.4.2 Eli Lilly and Company

- 7.4.3 Sanofi

- 7.4.4 AstraZeneca

- 7.4.5 Merck & Co.

- 7.4.6 Bristol Myers Squibb

- 7.4.7 Boehringer Ingelheim

- 7.4.8 Pfizer

- 7.4.9 Johnson & Johnson (Janssen)

- 7.4.10 Novartis

- 7.4.11 Biocon

- 7.4.12 Teva Pharmaceuticals

- 7.4.13 Mylan (Viatris)

- 7.4.14 Hualan Biologicals

- 7.4.15 Tonghua Dongbao

- 7.4.16 Wockhardt

- 7.4.17 Gan & Lee Pharmaceuticals

- 7.4.18 Hanmi Pharmaceutical

- 7.4.19 Mitsubishi Tanabe Pharma

- 7.4.20 Sun Pharma

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment