PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1331274

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1331274

Europe Diabetes Care Devices Market Size & Share Analysis - Growth Trends & Forecasts (2023 - 2028)

The Europe Diabetes Care Devices Market size is expected to grow from USD 8 billion in 2023 to USD 10.21 billion by 2028, at a CAGR of 6.18% during the forecast period (2023-2028).

The COVID-19 pandemic has substantially impacted the Europe Diabetes Care Devices Market. People with diabetes have a weak immune system so, with COVID-19, the immune system gets weaker very fast. People with diabetes will have more chances to get into serious complications rather than normal people. The manufacturers of diabetes care devices have taken care during COVID-19 to deliver the diabetes care devices to diabetes patients with the help of local governments. Novo Nordisk stated on their website that "Since the start of COVID-19, our commitment to patients, our employees and the communities where we operate has remained unchanged, we continue to supply our medicines and devices to people living with diabetes and other serious chronic diseases, safeguard the health of our employees, and take actions to support doctors and nurses as they work to defeat COVID-19." Doctors around the world suggested diabetes patients should check their diabetes levels more often to be careful and the intake of medicine has increased, which lead to an increase in the usage of diabetes care devices.

According to the diabetes category, the estimated cost per hospital admission during the first wave of COVID-19 in Europe ranged from EUR 25,018 for type 2 diabetes patients in good glycemic control to EUR 57,244 for type 1 diabetes patients in poor glycemic control, reflecting a higher risk of intensive care, ventilator support, and a longer hospital stay. The estimated cost for patients without diabetes was EUR 16,993. The expected total direct expenditures for COVID-19 secondary care in Europe were 13.9 billion euros. Diabetes treatment thus accounted for 23.5% of total expenditures.

The European countries are suffering from the burden of high diabetes expenditure due to its rising prevalence. Technological advancements have increased over the period in Diabetes care devices for safer and more accurate administration of insulin. Medtronic launched its first integrated smart insulin pen. The Medtronic Integrated Insulin Pen provides real-time glucose readings of patients along with insulin dose information to manage their glucose levels.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

Europe Diabetes Care Devices Market Trends

The continuous glucose monitoring segment is expected to witness the highest growth rate over the forecast period

The continuous glucose monitoring segment is expected to register a CAGR of around 14.8% over the forecast period.

A CGM is used by inserting a small sensor into the abdomen or arm with a tiny plastic tube known as a cannula penetrating the top layer of skin. An adhesive patch holds the sensor in place, allowing it to take glucose readings in interstitial fluid throughout the day and night. Generally, the sensors must be replaced every 7 to 14 days. A small, reusable transmitter connected to the sensor allows the system to send real-time readings wirelessly to a monitor device that displays blood glucose data. Some systems come with a dedicated monitor, and some now display the information via a smartphone app.

Continuous glucose monitoring sensors use glucose oxidase to detect blood sugar levels. Glucose oxidase converts glucose to hydrogen peroxidase, which reacts with the platinum inside the sensor, producing an electrical signal to be communicated to the transmitter. Sensors are the most important part of continuous glucose monitoring devices. Technological advancements to improve the accuracy of the sensors are expected to drive segment growth during the forecast period.

The frequency of monitoring glucose levels depends on the type of diabetes, which varies from patient to patient. Type-1 diabetic patients must check their blood glucose levels regularly, monitor their blood glucose levels, and adjust the insulin dosing accordingly. The current CGM devices show a detailed representation of blood glucose patterns and tendencies compared to a routine check of glucose levels at set intervals. Furthermore, the current continuous glucose monitoring devices can either retrospectively display the trends in blood glucose levels by downloading the data or give a real-time picture of glucose levels through receiver displays. Such advantages helped the rise in the adoption of these products in the market.

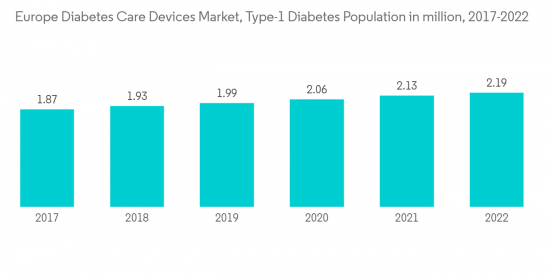

According to IDF, every year, 21,600 children are added to the type-1 diabetic population pool. These figures indicate that approximately 9% of the total healthcare expenditure is spent on diabetes in Europe. Various initiatives by the Government, such as the National Service Framework (NSF) program in the United Kingdom, are improving services by setting national standards to drive up service quality and tackle variations in care. The Association of British HealthTech Industries (ABHI) launched a diabetes section, enabling diabetes technology companies to work together in the first forum of its kind. The ABHI group is for any health technology company interested in diabetes care, from CGM and insulin pumps to apps.

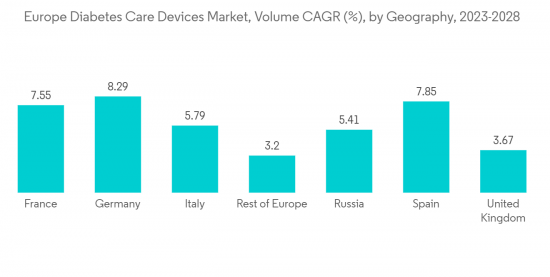

Germany held the highest market share in the European Diabetes Care Devices Market in the current year

Germany held the highest market share of about 28.3% in the European Diabetes Care Devices Market in the current year.

Diabetes is a significant health problem and one of the tremendous challenges for healthcare systems all over Germany. The prevalence of known type 1 & 2 diabetes in the German adult population is very high, along with many patients not yet diagnosed with the disease. Due to an aging population and unhealthy lifestyle, the prevalence of type 2 diabetes is expected to increase steadily over the next few years. High-quality care, including adequate monitoring, control of risk factors, and active self-management, are the key factors for preventing complications in German patients with type 2 diabetes. The disease's growing incidence, prevalence, and progressive nature encouraged the development of new drugs to provide additional treatment options for diabetic patients.

According to the German Diabetes Centre (DDZ), about 8.5 million people in Germany are affected by diabetes. The number of people with type 2 diabetes in Germany will continue to increase over the next twenty years. German law requires public plans to cap out-of-pocket health care costs and to cover all medically necessary treatment, including insulin. Germany is one of the developed countries with advanced healthcare facilities. Moreover, reimbursement and pricing policies are highly regulated, which drives the market. The roll-out of many new products, increasing international research collaborations in technology advancement, and increasing awareness about diabetes among people are some market opportunities for the players.

Europe Diabetes Care Devices Industry Overview

The Europe Diabetes Care Devices Market is moderately fragmented, with few significant and generic players. Manufacturers drove constant innovations to compete in the market. The major players, such as Abbott and Medtronic, underwent many mergers, acquisitions, and partnerships to establish market dominance while adhering to organic growth strategies. It is evident from the R&D spending of these companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Monitoring Devices

- 5.1.1 Self-monitoring Blood Glucose Devices

- 5.1.1.1 Glucometer Devices

- 5.1.1.2 Blood Glucose Test Strips

- 5.1.1.3 Lancets

- 5.1.2 Continuous Glucose Monitoring Devices

- 5.1.2.1 Sensors

- 5.1.2.2 Durables (Receivers and Transmitters)

- 5.1.1 Self-monitoring Blood Glucose Devices

- 5.2 Management Devices

- 5.2.1 Insulin Pump

- 5.2.1.1 Insulin Pump Device

- 5.2.1.2 Insulin Pump Reservoir

- 5.2.1.3 Infusion Set

- 5.2.2 Insulin Syringes

- 5.2.3 Cartridges in Reusable Pens

- 5.2.4 Insulin Disposable Pens

- 5.2.5 Jet Injectors

- 5.2.1 Insulin Pump

- 5.3 Geography

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Spain

- 5.3.5 United Kingdom

- 5.3.6 Russia

- 5.3.7 Rest of Europe

6 MARKET INDICATORS

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Dexcom Inc.

- 7.1.2 Insulet Corporation

- 7.1.3 Medtronic

- 7.1.4 Roche Diabetes Care

- 7.1.5 Novo Nordisk A/S

- 7.1.6 Ascensia Diabetes Care

- 7.1.7 Agamatrix Inc.

- 7.1.8 Bionime Corporation

- 7.1.9 LifeScan

- 7.1.10 Abbott Diabetes Care

- 7.1.11 Eli Lilly

- 7.1.12 Sanofi

- 7.1.13 Rossmax

- 7.2 COMPANY SHARE ANALYSIS

- 7.2.1 Self-monitoring Blood Glucose Devices

- 7.2.1.1 Abbott Diabetes Care

- 7.2.1.2 Roche Diabetes Care

- 7.2.1.3 LifeScan

- 7.2.1.4 Others

- 7.2.2 Continuous Glucose Monitoring Devices

- 7.2.2.1 Dexcom Inc.

- 7.2.2.2 Medtronic PLC

- 7.2.2.3 Abbott Diabetes Care

- 7.2.2.4 Others

- 7.2.3 Insulin Devices

- 7.2.3.1 Insulet Corporation

- 7.2.3.2 Novo Nordisk A/S

- 7.2.3.3 Others

- 7.2.1 Self-monitoring Blood Glucose Devices

8 MARKET OPPORTUNITIES AND FUTURE TRENDS