PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850149

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850149

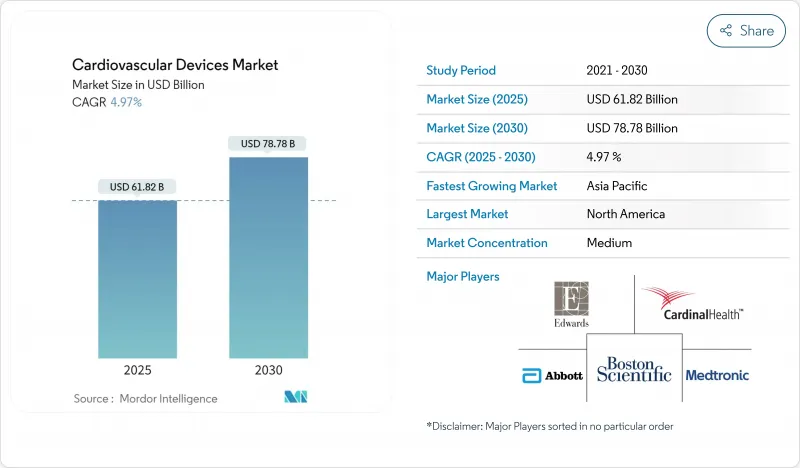

Cardiovascular Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Cardiovascular Devices Market size is estimated at USD 61.82 billion in 2025, and is expected to reach USD 78.78 billion by 2030, at a CAGR of 4.97% during the forecast period (2025-2030).

Demand accelerates as artificial intelligence enhances device functionality, making early detection more reliable and facilitating targeted therapies. The prevalence of minimally invasive procedures continues to grow, supported by expanded indications for transcatheter valve replacement and the increasing role of ambulatory surgical centers (ASCs). Strategic acquisitions among leading manufacturers are streamlining end-to-end treatment portfolios, while new FDA clearances for leadless pacemakers and renal denervation systems open fresh avenues for underserved patient groups. Heightened regulatory scrutiny and the high cost of advanced technology, however, remain barriers to adoption in price-sensitive regions.

Global Cardiovascular Devices Market Trends and Insights

Rapid Adoption of Minimally Invasive Procedures

Minimally invasive techniques are reshaping cardiovascular care by lowering complication rates and shortening hospital stays. Transcatheter tricuspid valve repair expanded market volume by more than 50% since Q2 2024. At the same time, pulsed-field ablation systems from Medtronic and Boston Scientific received FDA approvals during 2023-2024, bringing a safer approach to atrial fibrillation treatment. Investor interest mirrors these clinical shifts, as reflected in 342 cardiology clinic acquisitions from 2021 through September 2023. Johnson & Johnson's USD 13.1 billion purchase of Shockwave Medical underscores confidence in intravascular lithotripsy, already used in 400,000 procedures worldwide .

Increasing Burden of Cardiovascular Diseases

Heart and circulatory diseases cause 170,000 deaths a year in the United Kingdom and affect 7.6 million people, adding urgency to advanced diagnostics . Direct costs are steep in Asia-Pacific, reaching USD 21.7 billion in China alone. Eighty percent of disease burden links to modifiable risk factors, heightening interest in early-warning devices. Multimorbidity-diabetes coupled with cardiovascular conditions-accelerates mortality, making integrated solutions indispensable Journal of Clinical Medicine.

Integration of AI-Enabled Diagnostic Algorithms

Artificial intelligence now augments electrocardiogram interpretation, identifying subtle waveform patterns that precede detectable symptoms. AI-enhanced ECG can spot left-ventricular dysfunction at an AUC of 0.95, far surpassing traditional thresholds. Medtronic's AccuRhythm AI algorithms have cut false atrial fibrillation alerts by 88.2%, while preserving up to 100% of genuine alerts. FDA-cleared models like Implicity's SignalHF give clinicians a two-week heads-up on heart-failure deterioration, enabling timely intervention. Together, these advances spur further demand in the cardiovascular devices market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Advancements

- Restraint Impact Analysis

- Stringent Regulatory Policies and Product Recalls

- High Cost of Instruments and Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic and monitoring products led with 72.20% of the cardiovascular devices market share in 2024, underscoring the importance of early screening for risk management. Continuous ECG platforms, such as the BodyGuardian MINI, provide up to 15 days of Holter data, enriched by BeatLogic AI that refines rhythm classification. Vivalink's water-resistant wearable extends monitoring to 30 days, adding comfort for long-term observation. Artificial intelligence boosts diagnostic accuracy further, as CarDS-Plus can interpret single-lead smartwatch ECGs in roughly 35 seconds, creating actionable.

Therapeutic categories are advancing quickly. Leadless pacemakers limit infection risks linked to transvenous leads, and dual-chamber models like AVEIR DR now synchronize atrio-ventricular pacing. Breakthrough devices, including Abbott's dissolving stent for below-knee arteries, address chronic limb-threatening ischemia, expanding the cardiovascular devices market. AI-guided cardiac ablation posted 88% arrhythmia-free survival at 12 months versus 70% for pulmonary-vein-isolation alone, highlighting potential for superior outcomes. The cardiovascular devices market size attributed to advanced therapeutics is set to climb alongside these innovations.

The Global Cardiovascular Devices Market is Segmented by Device Type (Diagnostic and Monitoring Devices and Therapeutic and Surgical Devices), by Application (Coronary Artery Disease, Arrhythmia and More), by End User (Hospitals & Cardiac Centers, Ambulatory Surgical Centers and More) and Geography. The Report Offers the Value (in USD Billion) for all the Above Segments.

Geography Analysis

North America anchored 45.24% of the cardiovascular devices market in 2024, leveraging high per-capita healthcare spending and broad insurance coverage. Medicare reimbursement for ASCs reached USD 6.1 billion in 2022, illustrating public-payer traction for outpatient care medpac.gov. Robust regulatory frameworks allow rapid adoption of AI-enabled devices, as shown by multiple FDA clearances for leadless pacemakers and ablation systems during 2024. Supply-side strength stems from R&D hubs in Minnesota, California, and Massachusetts, where device firms co-locate with research universities.

Europe ranks second in revenue, supported by a tradition of clinical innovation. The European MDR's stricter scrutiny, however, may defer approvals and tighten post-market surveillance, temporarily constraining supply. Even so, CE Mark nods for the AVEIR DR pacemaker and M3 mitral valve system confirm continued innovation under the new rules abbott.mediaroom.com. Adoption of pulsed-field ablation and intravascular lithotripsy further underlines regional commitment to minimally invasive care.

Asia-Pacific is the fastest-growing region at an 8.96% CAGR through 2030. Aging populations and rising lifestyle-related risk factors create a large patient pool, with China alone counting 290 million cardiovascular disease patients biospectrumasia.com. Public-private partnerships improve infrastructure, and policy initiatives in India and China encourage domestic manufacturing. Despite heterogeneous regulatory pathways, local firms collaborate with global leaders for technology transfers, accelerating acceptance of novel implants. Collectively, these elements build momentum for the cardiovascular devices market across diverse economies.

- Abbott Laboratories

- Boston Scientific

- Edward Lifesciences

- Terumo

- Johnson & Johnson* (Biosense Webster, Cordis legacy)

- BIOTRONIK

- LivaNova plc

- MicroPort

- Lepu Medical

- B. Braun

- Getinge

- W. L. Gore & Associates

- Cook Group

- Cardinal Health

- Nihon Kohden

- Merit Medical Systems

- Zoll Medical

- Shockwave Medical, Inc.

- Penumbra

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Technological Advancements

- 4.2.2 Increasing Burden of Cardiovascular Diseases

- 4.2.3 Increased Preference for Minimally Invasive Procedures

- 4.2.4 Integration of AI-Enabled Diagnostic Algorithms

- 4.2.5 Proliferation of remote cardiac-monitoring reimbursement codes in United States CMS-2023

- 4.2.6 China's volume-based procurement for coronary stents reshaping price elasticity and accelerating unit uptake

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Policies and Product Recalls

- 4.3.2 High Cost of Instruments and Procedures

- 4.3.3 Shortage of heparin-coated raw materials due to swine fever in China impacting stent production pipeline

- 4.3.4 Reimbursement cap on TAVR implants by Indian NPPA

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD billion)

- 5.1 By Device Type

- 5.1.1 Diagnostic and Monitoring Devices

- 5.1.1.1 Electrocardiogram (ECG)

- 5.1.1.2 Remote Cardiac Monitoring

- 5.1.1.3 Other Diagnostic and Monitoring Devices

- 5.1.2 Therapeutic and Surgical Devices

- 5.1.2.1 Cardiac Assist Devices

- 5.1.2.2 Cardiac Rhythm Management Devices

- 5.1.2.3 Catheters

- 5.1.2.4 Grafts

- 5.1.2.5 Heart Valves

- 5.1.2.6 Stents

- 5.1.2.7 Other Therapeutic and Surgical Devices

- 5.1.1 Diagnostic and Monitoring Devices

- 5.2 By Application

- 5.2.1 Coronary Artery Disease

- 5.2.2 Arrhythmia

- 5.2.3 Heart Failure

- 5.2.4 Structural Heart Disease

- 5.2.5 Hypertension

- 5.2.6 Others

- 5.3 By End-User

- 5.3.1 Hospitals & Cardiac Centers

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home-Care Settings

- 5.3.4 Specialty Clinics

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Abbott Laboratories

- 6.4.2 Boston Scientific Corporation

- 6.4.3 Edwards Lifesciences Corporation

- 6.4.4 Terumo Corporation

- 6.4.5 Johnson & Johnson* (Biosense Webster, Cordis legacy)

- 6.4.6 BIOTRONIK SE & Co. KG

- 6.4.7 LivaNova plc

- 6.4.8 MicroPort Scientific Corporation

- 6.4.9 Lepu Medical Technology

- 6.4.10 B. Braun Melsungen AG

- 6.4.11 Getinge AB

- 6.4.12 W. L. Gore & Associates

- 6.4.13 Cook Medical

- 6.4.14 Cardinal Health, Inc.

- 6.4.15 Nihon Kohden Corporation

- 6.4.16 Merit Medical Systems

- 6.4.17 ZOLL Medical Corporation

- 6.4.18 Shockwave Medical, Inc.

- 6.4.19 Penumbra, Inc.

7 Market Opportunities & Future Outlook