PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685889

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1685889

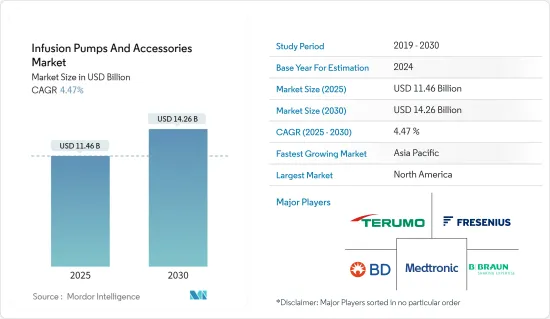

Infusion Pumps And Accessories - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Infusion Pumps And Accessories Market size is estimated at USD 11.46 billion in 2025, and is expected to reach USD 14.26 billion by 2030, at a CAGR of 4.47% during the forecast period (2025-2030).

The COVID-19 pandemic brought infusion pumps to the forefront since the demand for infusion pumps surged considerably during the COVID-19 lockdown, as the number of COVID-19 cases increased faster with growing hospital admissions. The demand for intravenous infusion therapies was higher during the first wave of the pandemic to provide essential nutrients to sepsis patients in the intensive care unit (ICU). For instance, an article published in May 2022 in PubMed stated that sepsis was present in 32.5% of total COVID-19 hospitalizations, of which 70.8% of sepsis were due to SARS-CoV-2 alone and 26.2% were due to both SARS-CoV-2 and non-SARS-CoV-2 infections. Infusion pumps were, therefore, frequently employed for IV fluid delivery for sepsis-affected patients, which further propelled the market expansion during the pandemic.

Thus, overall, the pandemic offered healthy growth for the market due to the increase in the patient pool in healthcare settings. However, the increase in the utilization of next-generation infusion systems, advancements in infusion bags, and the rise in chronic diseases, accidents, and blood transfusions are expected to bolster the market growth in the coming years.

The infusion pumps and accessories market is primarily driven by the rising incidence of chronic diseases, such as cancer and others, coupled with the rising adoption of infusion devices. Infusion pumps are widely used in chemotherapy, diabetes management, and many other applications. The rising prevalence of these diseases worldwide creates ample opportunities for the market to grow. Patients with cancer are more prone to hypovolemia, which is the absence of water in the extracellular space due to excessive fluid loss (such as vomiting and diarrhea) or insufficient fluid intake.

An increase in cancer cases is expected to raise the demand for pressure infusion bags, bolstering market growth. For instance, according to the American Cancer Society 2023 Cancer Statistics, the new cancer cases are estimated to be 1.93 million in the United States in 2023. This estimation includes 1.01 million males and 948,000 cases of females. The high burden of cancer is augmenting the demand for infusion pumps and accessories, thereby boosting market growth over the forecast period.

Moreover, increased clinical research activities involving infusion-related drug delivery are expected to bolster market growth over the forecast period. For instance, in November 2022, TriSalus Life Sciences, Inc., an oncology therapeutics company, publicized the additional information regarding its ongoing Pressure-Enabled Regional Immuno-Oncology ('PERIO 01') and ('PERIO 02') clinical studies for primary and metastatic liver tumors. The TriSalus platform comprises the TriNav Infusion System and SD-101, a class C toll-like receptor 9 (TLR9) agonist. TriNav is an FDA-cleared device designed to administer established and emerging therapeutics.

Additionally, technological advancements in device technology and innovative product launches by the key players are likely to fuel market growth. For instance, in February 2021, United Therapeutics launched the Remunity Pump for remodeling drug delivery, which helps to improve the lives of patients with pulmonary arterial hypertension (PAH). Similarly, in February 2021, Mindray Medical launched BeneFusion E series-ESP, EVP, and EDS, new infusion systems for expanding its product portfolio.

Hence, owing to the rise in chronic diseases and rapid advancements in infusion pumps coupled with product launches by the key players, the market is anticipated to grow significantly over the forecast period. However, the higher cost of infusion pumps and the associated safety issues are expected to restrain the market growth over the forecast period.

Infusion Pumps and Accessories Market Trends

Volumetric Infusion Pumps Segment Is Expected to Witness a Significant Growth Over the Forecast Period

Volumetric infusion pumps have many applications in disease management and parenteral nutrition. The safety, accuracy, and simplicity of volumetric infusion pumps in treating many therapeutic areas contribute to the high demand for these pumps. The volumetric infusion pump segment is expected to witness significant growth owing to the rise in blood and drug transfusion cases and the increase in strategic product launches by the key players.

The increasing number of injuries and trauma cases is expected to raise the demand for drug infusions, which is anticipated to drive the growth of the segment over the study period. For instance, the Road Safety Observatory report published in February 2022 stated that the number of injury accidents recorded by police forces in France was 3,728 in January 2022, which was higher than that of 2021 (3,508). The rising burden of road accidents leads to blood loss and creates the need for emergency transfusion, further projected to boost the segment growth over the forecast period.

Furthermore, the advancements and the emergence of innovative volumetric pumps, along with the increase in regulatory approvals, are expected to bolster segment growth. For instance, in March 2022, Fresenius Kabi received regulatory clearance from the FDA for its wireless Agilia connect infusion system, which includes the Agilia volumetric pump and the Agilia syringe pump with the vigilant software suite Vigilant Master Med technology. The Agilia Connect volumetric pump and syringe pump is one of the first to be cleared by following TIR101 standards developed by the Association for the Advancement of Medical Instrumentation (AAMI) in 2021.

Additionally, the major players are focusing on research and development activities, which is expected to boost the growth of the market segment. For instance, in November 2021, Zealand Pharma and DEKA Research & Development Corp. signed an agreement to advance the development of an infusion pump that can be used with glucagon for the treatment of congenital hyperinsulinism (CHI).

Thus, due to the aforementioned factors, such as the rising prevalence of chronic diseases and technological advancement, the studied segment is expected to witness healthy growth over the study period.

North America is Anticipated to Hold a Significant Market Share Over the Forecast Period

North America is expected to hold a significant market share in the infusion pumps and accessories market owing to the surge in chronic disorders, high healthcare expenditures, the increasing surgical treatments for chronic diseases, the increased R&D expenditure, and the presence of key players in the region. For instance, according to the data published by the CDC in July 2022, the cesarean delivery rate in the United States increased to 32.1% in 2021 from 31.8% in the previous year. Thus, the rising number of cesarean section surgeries is expected to boost the usage of infusion bags and accessories for blood and other drug delivery purposes, fueling market growth.

Moreover, blood transfusions are crucial in the treatment of cancer because they assist the body in getting healthy blood cells. Additionally, certain malignancies (particularly those of the digestive system) result in internal bleeding, which worsens anemia and the patient's condition. Thus, a high burden of cancer cases is expected to utilize infusion pumps and related accessories. For instance, according to the 2022 statistics published by the Canadian Cancer Society, about 233,900 cancer cases were diagnosed in Canada in 2022. Therefore, the high burden of cancer cases is expected to surge the demand for infusion pumps and accessories, leading to market growth over the study period.

Furthermore, the rising strategic activities by the key players, such as product launches, agreements, and collaboration in the North American region, are expected to bolster market growth over the forecast period. For instance, in November 2022, Medtronic plc launched an extended infusion set, one of the first infusion sets labeled for up to 7-day wear in the United States. The Medtronic Extended infusion set utilizes advanced materials that help reduce insulin preservative loss and maintain insulin flow and stability to double the wear time of an infusion set. Similarly, in May 2021, Smiths Medical partnered with Ivenix, Inc. to offer a comprehensive suite of infusion management solutions for healthcare needs in the United States.

Thus, due to the high prevalence of chronic diseases and strategic product launches by the key players, North America is expected to witness significant market growth over the study period.

Infusion Pumps and Accessories Industry Overview

The infusion pumps and accessories market is highly competitive and fragmented due to the presence of a large number of global and local players. Many key players are concentrating on various strategic activities like product launches, partnerships and collaborations to increase their presence across the globe. Some of the key global players in the infusion pumps and accessories market are Baxter International Inc., Becton, Dickinson and Company, Braun SE, Eli Lilly and Company, F. Hoffmann-la Roche Ltd, and Fresenius (Fresenius Kabi) among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption Rate of Infusion Pumps

- 4.2.2 Rising Incidences of Chronic Disease

- 4.3 Market Restraints

- 4.3.1 High Price of Infusion Pumps and Safety Issues Associated with Infusion Pumps

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Infusion Pump Types

- 5.1.1.1 Syringe Infusion Pumps

- 5.1.1.2 Volumetric Infusion Pumps

- 5.1.1.3 Elastomeric Infusion Pumps

- 5.1.1.4 Insulin Infusion Pumps

- 5.1.1.5 Enteral Infusion Pumps

- 5.1.1.6 Other Product Types

- 5.1.2 Accessories/Disposables

- 5.1.1 Infusion Pump Types

- 5.2 By Application

- 5.2.1 Gastroenterology

- 5.2.2 Diabetes Management

- 5.2.3 Hematology

- 5.2.4 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Center

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Baxter

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Braun SE

- 6.1.4 Eli Lilly and Company

- 6.1.5 Merit Medical

- 6.1.6 Fresenius (Fresenius Kabi)

- 6.1.7 ICU Medical Inc.

- 6.1.8 Eitan Medical Ltd.

- 6.1.9 Medtronic Inc.

- 6.1.10 Nipro Corporation

- 6.1.11 Option Care Health Inc.

- 6.1.12 Terumo Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS