PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044111

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044111

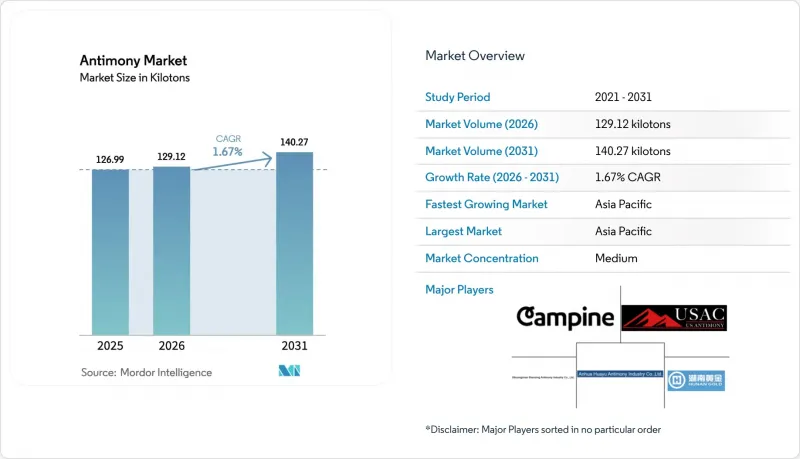

Antimony - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Antimony Market size was valued at 126.99 kilotons in 2025 and is estimated to grow from 129.12 kilotons in 2026 to reach 140.27 kilotons by 2031, at a CAGR of 1.67% during the forecast period (2026-2031).

A rapid price escalation exposed structural reliance on Chinese supply. Strategic demand continues to pivot toward energy storage, semiconductor doping, and defense electronics, where antimony's metallurgical and electronic properties have few substitutes. Western miners, refiners, and governments are scaling new capacity in Idaho, Montana, and Australia to counter China's December 2024 export ban, a move that doubled benchmark prices and spurred vertically integrated projects. Meanwhile, regulatory scrutiny over toxicology in Europe and North America is accelerating a gradual shift to halogen-free flame retardants, tempering volume growth but pushing value toward higher purity and specialty grades. Competitive differentiation is shifting away from cost and toward purity, provenance, and security of supply, especially for semiconductor-grade material.

Global Antimony Market Trends and Insights

Grid-Scale Lead-Acid and Liquid-Metal Battery Expansion in Asia-Pacific

Utility-scale storage is increasingly shaping the Antimony market. In February 2024, Ambri secured Series D financing and is set to deliver liquid-metal batteries, reliant on antimony-lead cathodes, to Xcel Energy and Vistra. While lead-acid batteries continue to dominate telecom backups throughout Southeast Asia, they incorporate antimony in their grid alloys to enhance deep-cycle durability. China's vast fleet of internal-combustion vehicles, even as electrification gains momentum, bolsters baseline demand, anchoring the Antimony market firmly in the automotive sector. Although the rise of calcium-tin alloys might reduce antimony usage in batteries, grid-scale liquid-metal systems counteract this by consuming significant amounts of high-purity antimony per module. This dynamic not only boosts aggregate volumes in the medium term but also enhances the value of supply adhering to stringent purity standards.

PET Resin Boom Boosting Sb-Catalyst Use

Antimony trioxide serves as the primary polymerization catalyst for over 90% of polyethylene terephthalate (PET) production. New PET facilities in Saudi Arabia and Vietnam are set to begin operations before 2027. Teijin's recent patent on ternary catalyst mixtures underscores the industry's push to reduce residual antimony while maintaining kinetic benefits. However, regulators are keeping a close watch. The European Chemicals Agency is currently reevaluating the permissible migration limits for food-contact packaging. This scrutiny introduces compliance costs, potentially steering the industry towards titanium-based systems for premium products. While low capital expenditure and established expertise currently uphold antimony's dominance as a catalyst, downstream producers are actively exploring alternatives to mitigate regulatory risks. This cautious approach tempers the growth outlook for the antimony market beyond the immediate two-year horizon.

Volatile Chinese Export Quotas and Price Spikes

Benchmark Rotterdam prices surged significantly from December 2023 to February 2025. This sharp rise has squeezed margins for compounders and battery makers, who find it challenging to pass on these costs. In Europe and North America, small and mid-sized processors are feeling the brunt of this cash-flow strain, with some even pausing production until prices stabilize. Korea Zinc's annual supply remains limited, accounting for a small fraction of the global mined output. This limited supply leaves Western buyers vulnerable to policy shifts in Beijing. As projects like Stibnite gear up, the ongoing volatility is projected to impact the forecasted CAGR.

Other drivers and restraints analyzed in the detailed report include:

- China Export Controls Driving Non-China Supply-Chain Investment

- Antimony Alloying in Next-Gen Calcium/Sodium Liquid-Metal Batteries

- Shift Toward Halogen-Free Flame Retardants in EU and NA

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antimony trioxide held 56.48% of the 2025 volume, reflecting its entrenched roles in PET catalysis and flame retardancy. However, its growth trajectory faces constraints due to Europe's shift towards halogen-free alternatives. Antimony pentoxide is expanding at a 2.5% CAGR as specialty glass and photovoltaic manufacturers seek its superior decolorizing and fining capabilities. Metal ingots, boasting a premium purity from Korea Zinc, cater to the high-purity demands of the military and semiconductor sectors. While lead-acid battery alloys are seeing reduced antimony loadings due to the rise of calcium-tin formulations, grid-scale batteries are helping to offset this decline. Additionally, niche products like antimony trisulfide, favored in pyrotechnics, command high margins but contribute negligible tonnage, highlighting the diverse dynamics within the antimony market.

While pentoxide's ascent bolsters specialty revenues, trioxide's dominance remains unchallenged outside Europe and North America. Teijin's advancements in ternary catalysts could extend trioxide's reign in the PET sector by curbing migration without compromising kinetics. Even a slight success in this endeavor could insulate a significant portion of global antimony demand from imminent substitutions. Thus, the antimony market is characterized by a volume-heavy, regulation-sensitive trioxide foundation, complemented by the rapid growth of pentoxide and a niche high-purity ingot segment that drives significant profits.

Flame retardants consumed 55.02% of the 2025 volume, but that dominance is losing momentum in the West. Ceramics and glass are growing at a 3.3% CAGR thanks to photovoltaic glass fining and antimony-doped monocrystalline silicon. Catalyst demand in PET polymerization remains substantial but is sensitive to regulatory pressure. Specialty electronic uses, measured in kilograms, carry high margins and strategic significance. This application mix indicates a transition toward fewer but higher value streams, creating a cushion for aggregate revenues even if flame-retardant tonnage erodes in mature economies.

Ceramic demand provides a hedge against regulatory headwinds, particularly as solar-glass producers secure antimony pentoxide to improve clarity and bubble removal. Batteries offer another hedge: although per-unit antimony intensity is falling in automotive starters, grid-scale projects require kilogram-level loadings per module. Therefore, the Antimony market maintains diversified demand drivers that temper downside risk from any single application class.

The Antimony Market Report is Segmented by Product Type (Metal Ingot, Antimony Trioxide, Antimony Pentoxide, Alloys, and Other Product Types), Ore Type (Stibnite and Others), Application (Flame Retardants, Batteries, and More), End-User Industry (Plastics and Polymers, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 86.67% of global volume in 2025 and is expanding at a 3.12% CAGR. In 2024, China refined antimony but operated at only one-third of its installed capacity, grappling with ore scarcity and compliance costs. Rising demand in India's plastics and two-wheeler sectors, coupled with Vietnam's PET surge, solidifies Asia-Pacific's central role in the Antimony market. Despite domestic refining, Japan remains a net importer, predominantly sourcing from China and Vietnam. Meanwhile, South Korea's Korea Zinc increased its output and plans a modest rise, with a portion of the production targeted for Western markets.

North America is gearing up for a supply expansion. Projects like Perpetua's Stibnite and operations by United States Antimony in Mexico and Montana are poised to meet a significant portion of domestic needs in the coming years. This demand is driven by sectors like defense electronics, grid-scale storage, and semiconductor fabs, especially with the reshoring push under the CHIPS and Science Act. While Europe relies heavily on imports, tightening regulations on flame retardants are prompting processors like Belgium's Campine to pivot towards recycling. In the Middle East-Africa/South America region, Bolivia and Morocco are key players in diversifying the supply, but their combined output offers only limited relief.

Despite Western diversification efforts, the Asia-Pacific market share is expected to decline slightly in the coming years, as Chinese smelters continue to benefit from economies of scale in refining. Yet, driven by political motivations for resilient supply chains, a larger portion of the Antimony market volumes is anticipated to flow through non-Chinese channels, even if the absolute tonnage doesn't keep pace with regional demand growth.

- Alkane Resources Ltd.

- AMG Advanced Metallurgical Group N.V.

- Belmont Metals Inc.

- Campine NV

- GUANGXI HUAYUAN METAL CHEMICAL CO., LTD.

- Hunan Gold Co., Ltd.

- Hunan Province Anhua Huayu Antimony Industry Co., Ltd.

- Koreazinc

- Lambert Metals International Limited

- Nihon Seiko Co., Ltd.

- Perpetua Resources

- SPMP (Strategic and Precious Metals Processing)

- SUZUHIRO CHEMICAL CO.,LTD.

- United States Antimony Corporation

- Xikuangshan Shanxing Antimony Industry Co., Ltd.

- Yiyang City Huachang Antimony Industry Co.,Ltd

- Youngsun (Guangdong Yuxing) Fire-Retardant New Material Co.

- Yunnan Muli Antimony Industry Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-scale lead-acid and liquid-metal battery expansion in Asia-Pacific

- 4.2.2 PET resin boom boosting Sb-catalyst use

- 4.2.3 China export controls driving non-China supply-chain investment

- 4.2.4 Antimony alloying in next-gen calcium/sodium liquid-metal batteries

- 4.2.5 Semiconductor-grade Sb for 5G and quantum devices

- 4.3 Market Restraints

- 4.3.1 Volatile Chinese export quotas and price spikes

- 4.3.2 Shift toward halogen-free flame retardants in EU and NA

- 4.3.3 REACH/TSCA toxicology compliance costs

- 4.4 Value Chain Analysis

- 4.5 Production Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Supply Analysis

- 4.8 Regulatory Policy Analysis

- 4.9 Trade Analysis

- 4.10 Price Trend Analysis

- 4.11 Production Cost Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Metal Ingot

- 5.1.2 Antimony Trioxide

- 5.1.3 Antimony Pentoxide

- 5.1.4 Alloys

- 5.1.5 Other Product Types (Granules, Single Crystals, etc.)

- 5.2 By Ore type

- 5.2.1 Stibnite

- 5.2.2 Others

- 5.3 By Application

- 5.3.1 Flame Retardants

- 5.3.2 Batteries

- 5.3.3 Ceramics and Glass

- 5.3.4 Catalyst

- 5.3.5 Other Applications (Semiconductor, Defense, etc.)

- 5.4 By End-user Industry

- 5.4.1 Plastics and Polymers

- 5.4.2 Automotive and Transportation

- 5.4.3 Chemicals and Catalysts

- 5.4.4 Electronics and Semiconductor

- 5.4.5 Energy Storage and Utilities

- 5.4.6 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacifc

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacifc

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles

- 6.4.1 Alkane Resources Ltd.

- 6.4.2 AMG Advanced Metallurgical Group N.V.

- 6.4.3 Belmont Metals Inc.

- 6.4.4 Campine NV

- 6.4.5 GUANGXI HUAYUAN METAL CHEMICAL CO., LTD.

- 6.4.6 Hunan Gold Co., Ltd.

- 6.4.7 Hunan Province Anhua Huayu Antimony Industry Co., Ltd.

- 6.4.8 Koreazinc

- 6.4.9 Lambert Metals International Limited

- 6.4.10 Nihon Seiko Co., Ltd.

- 6.4.11 Perpetua Resources

- 6.4.12 SPMP (Strategic and Precious Metals Processing)

- 6.4.13 SUZUHIRO CHEMICAL CO.,LTD.

- 6.4.14 United States Antimony Corporation

- 6.4.15 Xikuangshan Shanxing Antimony Industry Co., Ltd.

- 6.4.16 Yiyang City Huachang Antimony Industry Co.,Ltd

- 6.4.17 Youngsun (Guangdong Yuxing) Fire-Retardant New Material Co.

- 6.4.18 Yunnan Muli Antimony Industry Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 Recycling of end-of-life lead-acid batteries

- 7.2 Development of domestic refining outside China

- 7.3 White-space and unmet-need assessment