PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406088

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1406088

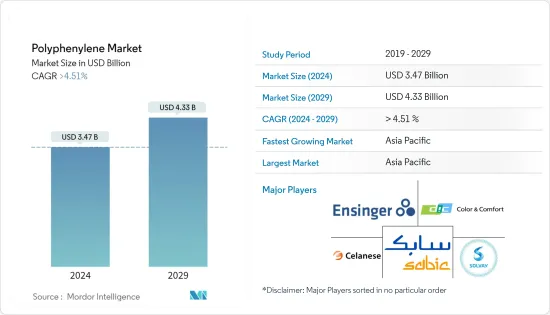

Polyphenylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029

The Polyphenylene Market size is estimated at USD 3.47 billion in 2024, and is expected to reach USD 4.33 billion by 2029, growing at a CAGR of greater than 4.51% during the forecast period (2024-2029).

The polyphenylene market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, wherein industries such as electrical and electronics, transportation, and others were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The growing usage of polyphenylene in the electrical and electronics industry and increasing demand for hybrid electric vehicles are the factors driving the growth of the studied market.

On the flip side, the availability of substitutes and the high cost associated with polyphenylene over other conventional materials are key factors limiting the growth of the market studied.

Moreover, the emerging applications of polyphenylene in 5G circuit board is a key factor expected to act as a lucrative opportunity for the studied market.

Asia-Pacific is expected to dominate the market, with the largest consumption from China, Japan, South Korea, and India.

Polyphenylene Market Trends

Increasing Demand from Automotive and Transportation Segment

- Polyphenylene is processed into its derivatives, like polyphenylene sulfide (PPS), polyphenylene oxide (PPO), and polyphenylene ether (PPE). Polyphenylene derivatives are preferred in electric auto parts that require higher temperature stability.

- In recent years, PPS successfully replaced metal, aromatic nylons, phenolic polymers, and bulk molding compounds in various engineered vehicle components.

- Polyphenylene derivatives become the ideal choice for automotive parts exposed to high temperatures. These can provide high strength while being light in weight. These are used in vehicle components, like electrical connectors, ignition systems, lighting systems, fuel systems, hybrid vehicle inverter components, and pistons.

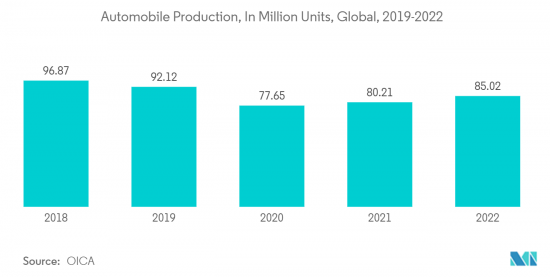

- According to the Organisation Internationale des Constructeurs d'Automobiles(OICA), 85.02 million vehicles were produced across the globe in 2022, witnessing a growth rate of 6% compared to 2021, thereby enhancing the demand for polyphenylene derivatives, which are employed for various automotive parts.

- China is the largest manufacturer of automobiles in the world. The country's automotive sector has been shaping up for product evolution, with the country focusing on manufacturing products to ensure fuel economy while minimizing emissions, owing to the growing environmental concerns.

- According to OICA, automobile production and sales in the country reached 27.021 million and 26.864 million, respectively, in 2022, up 3.4% and 2.1% from the previous year.

- Further, the global electric vehicle market is expanding significantly which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- All factors above are likely to significantly enhance the demand for polyphenylene in the automotive and transportation segment, and thus will propel the growth of the market studied.

Asia-Pacific to Dominate the Market

- Asia-Pacific represents the largest market for polyphenylene. In countries like China, Japan, South Korea, and India, the demand for polyphenylene has been increasing due to growing industries like automotive and transportation and electrical and electronics.

- In the Asia-Pacific region, the governments have adopted favorable policies toward the adoption of electric vehicles and the expansion of manufacturing infrastructure for electric vehicles. This, in turn, is anticipated to provide a huge impetus to the electric vehicle market in the region during the forecast period.

- The Chinese government policy developments include the restriction of investments in new ICE-vehicle manufacturing plants and a proposal to tighten the average fuel economy of its light-duty passenger vehicle fleet by 2025.

- Increasing standards of living in Asian countries have also led to increased awareness among the people of the use of electric and hybrid vehicles.

- The Asia-Pacific region is also the dominant producer of electrical and electronics across the world, with countries such as China, Japan, South Korea, and Malaysia contributing toward it. India is also emerging as a manufacturing hub for electronic products in Asia. This established industry is expected to attract demand for polyphenylene and its derivatives from the region.

- Thus, the increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth. In the electronics segment, Chinese manufacturers are setting up overseas production bases in order to expand in the international markets.

- For instance, In March 2023, TCL broadened its presence in international markets by establishing factories abroad, producing televisions, modules, and photovoltaic cells in Vietnam, Malaysia, Mexico, and India. In addition, it has formed partnerships with local companies in Brazil to collaboratively develop production facilities, supply chains, and an R&D infrastructure.

- Further, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

- Moreover, as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year.

- Thus, rising demand from the end-user mentioned above industries is expected to drive growth in the Asia-Pacific region.

Polyphenylene Industry Overview

The polyphenylene market is partially fragmented in nature. The major players in the studied market (not in any particular order) include SABIC, Ensinger, Celanese Corporation, DIC CORPORATION, and Solvay, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Electrical and Electronics Industry

- 4.1.2 Increasing Demand from Hybrid Electric Vehicles

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Availability of Substitute

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Polyphenylene Sulfide

- 5.1.2 Polyphenylene Oxide

- 5.1.3 Polyphenylene Ether

- 5.2 End-user Industry

- 5.2.1 Electrical and Electronics

- 5.2.2 Automotive and Transportation

- 5.2.3 Other End-user Industries (Coatings, Etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Mexico

- 5.3.2.3 Canada

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Biesterfeld AG

- 6.4.2 Celanese Corporation

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 DIC Corporation

- 6.4.5 Emco Industrial Plastics

- 6.4.6 Ensinger

- 6.4.7 KUREHA CORPORATION

- 6.4.8 LG Chem

- 6.4.9 Mitsubishi Chemical Group of companies

- 6.4.10 Nagase America LLC

- 6.4.11 RTP Company

- 6.4.12 SABIC

- 6.4.13 Solvay

- 6.4.14 Sumitomo Bakelite Co., Ltd.

- 6.4.15 TORAY INDUSTRIES, INC.

- 6.4.16 Tosoh Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Applications in 5G Circuit Board

- 7.2 Other Opportunities