PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1938978

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1938978

Cybersecurity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

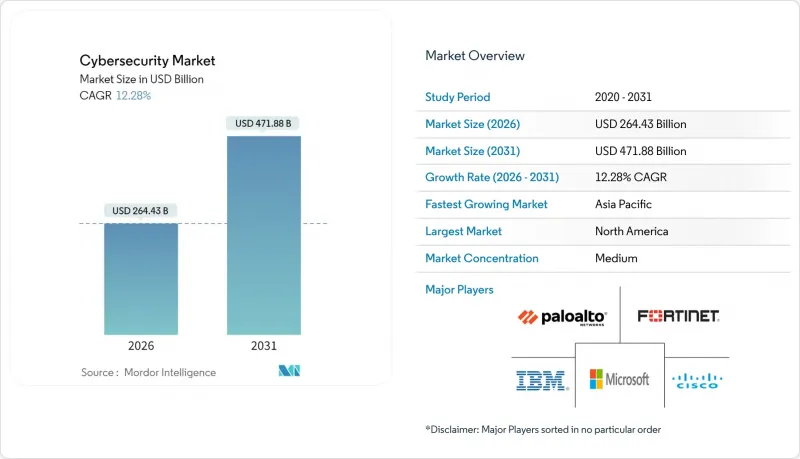

Cybersecurity Market size in 2026 is estimated at USD 264.43 billion, growing from 2025 value of USD 235.5 billion with 2031 projections showing USD 471.88 billion, growing at 12.28% CAGR over 2026-2031.

Increased spending on zero-trust architectures, the integration of IT and operational technology (OT) defenses, and preparations for quantum-ready encryption are the primary forces behind this expansion. North America retains spending leadership, while Asia-Pacific registers the most rapid gains as enterprises migrate workloads to cloud-first environments. Budget allocations are also rising as cyber-insurance underwriters demand verifiable controls, pushing organizations toward unified security platforms that simplify oversight. Simultaneously, platform consolidation through mergers and acquisitions is intensifying as vendors race to cover emerging threat vectors.

Global Cybersecurity Market Trends and Insights

Accelerated Cloud-First Digital Transformation

Cloud migration is reshaping security investment priorities as perimeter controls fail in distributed environments. Cloud deployment is growing, outpacing on-premise allocations and driving demand for cloud-native application protection platforms that integrate identity, workload, and data safeguards. Enterprises are seeking unified consoles to reduce tool sprawl, and vendors are responding with platforms that correlate telemetry across hybrid estates, improving visibility and response efficiency .

IT-OT Security Convergence Across Critical Infrastructure

Industry 4.0 forces formerly air-gapped systems online, exposing legacy control networks to the same adversaries that target IT assets, driving heightened demand in the cybersecurity market. Regulatory frameworks such as ISA/IEC 62443 now require integrated defenses that span production floors and data centers, encouraging investment in specialized OT threat detection and segmentation tools. Energy utilities are leading adoption as nation-state actors probe grid vulnerabilities, and returns on OT-focused security initiatives now exceed comparable IT projects in risk-reduction value.

Cyber-Security Talent Deficit and Wage Inflation

The shortfall of 3.4 million professionals strains budgets as salaries climb for scarce skills in cloud, OT, and AI-driven defense. This constraint is driving market consolidation toward platforms that require fewer specialized personnel to operate, while simultaneously creating opportunities for vendors offering managed security services and AI-powered automation tools. The situation is exacerbated by high turnover rates, with 64% of cybersecurity professionals considering job changes due to workload stress, creating a continuous cycle of recruitment and training costs that impact organizational security budgets .

Other drivers and restraints analyzed in the detailed report include:

- Zero-Trust Architecture Mandates for Hybrid Workforce

- Surge in Cyber-Insurance Underwriting Requirements

- Integration Complexity with Legacy Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America controlled 43.20% of 2025 revenue in the cybersecurity market, underpinned by mature regulations and the presence of major vendors. Regional spending is forecast to surpass USD 137.6 billion by 2027 as Executive Order 14028 obliges extensive zero-trust migration. The United States reported 9,036 cyber incidents in 2023, dwarfing Europe's 2,557 events and sustaining demand for advanced threat intelligence feeds and managed SOC services. Canada and Mexico contribute to growth through joint public-private programs that harmonise cross-border breach reporting and incident response.

Asia-Pacific is the fastest-growing area at 16.85% CAGR, with state-backed digital-nation plans elevating security to critical-infrastructure status. China, India, Japan, and South Korea allocate multi-year budgets to national cyber strategies, while Australia and New Zealand implement comprehensive resilience frameworks that require mandatory incident disclosure. Regional buyers often leapfrog legacy controls by adopting cloud-native security from the outset, accelerating uptake of identity-centric and AI-driven analytics.

Europe region growth is propelled by GDPR enforcement and the forthcoming NIS2 directive that expands coverage to more sectors. Germany, the United Kingdom, and France headline spending, whereas Central and Eastern European markets grow from a smaller base as they align with EU requirements. Sovereign-cloud initiatives in France and Spain stimulate demand for domestically hosted security stacks, while cross-border data-transfer restrictions accelerate adoption of privacy-enhancing encryption techniques.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems, Inc.

- Palo Alto Networks, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- CrowdStrike Holdings, Inc.

- Trend Micro Incorporated

- Zscaler, Inc.

- Okta, Inc.

- Gen Digital Inc. (formerly NortonLifeLock Inc.)

- Sophos Limited

- Proofpoint, Inc.

- McAfee LLC

- Darktrace plc

- Rapid7, Inc.

- SentinelOne, Inc.

- Imperva, Inc.

- Qualys, Inc.

- Trellix Holdings LLC

- Splunk Inc.

- Elastic N.V.

- Akamai Technologies, Inc.

- Broadcom Inc. (Symantec Enterprise Division)

- VMware, Inc.

- Cybereason

- Ivanti, Inc.

- Tenable Holdings, Inc.

- CyberArk Software Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated cloud-first digital transformation

- 4.2.2 IT-OT security convergence across critical infrastructure

- 4.2.3 Zero-trust architecture mandates for hybrid workforce

- 4.2.4 Surge in cyber-insurance underwriting requirements

- 4.2.5 Digital-sovereignty regulations driving localised security stacks

- 4.2.6 Timelines for quantum-ready cryptography migration

- 4.3 Market Restraints

- 4.3.1 Cyber-security talent deficit and wage inflation

- 4.3.2 Integration complexity with legacy infrastructure

- 4.3.3 API-sprawl expanding attack-surface complexity

- 4.3.4 SOC alert-fatigue and false-positive overload limiting ROI

- 4.4 Value Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Key Use Cased and Case Studies

- 4.10 Analysis of Pricing and Pricing Model

- 4.11 Cybersecurity Training Trends

- 4.12 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security

- 5.1.1.8 End-point Security

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Retail and E-commerce

- 5.3.6 Energy and Utilities

- 5.3.7 Manufacturing

- 5.3.8 Others

- 5.4 By End-user Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Palo Alto Networks, Inc.

- 6.4.5 Fortinet, Inc.

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 CrowdStrike Holdings, Inc.

- 6.4.8 Trend Micro Incorporated

- 6.4.9 Zscaler, Inc.

- 6.4.10 Okta, Inc.

- 6.4.11 Gen Digital Inc. (formerly NortonLifeLock Inc.)

- 6.4.12 Sophos Limited

- 6.4.13 Proofpoint, Inc.

- 6.4.14 McAfee LLC

- 6.4.15 Darktrace plc

- 6.4.16 Rapid7, Inc.

- 6.4.17 SentinelOne, Inc.

- 6.4.18 Imperva, Inc.

- 6.4.19 Qualys, Inc.

- 6.4.20 Trellix Holdings LLC

- 6.4.21 Splunk Inc.

- 6.4.22 Elastic N.V.

- 6.4.23 Akamai Technologies, Inc.

- 6.4.24 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.25 VMware, Inc.

- 6.4.26 Cybereason

- 6.4.27 Ivanti, Inc.

- 6.4.28 Tenable Holdings, Inc.

- 6.4.29 CyberArk Software Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment