PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907216

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907216

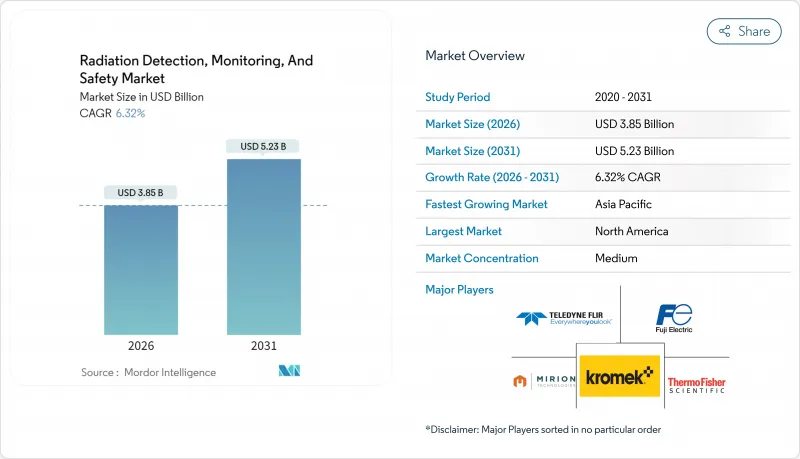

Radiation Detection, Monitoring, And Safety - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The radiation detection, monitoring, and safety market size in 2026 is estimated at USD 3.85 billion, growing from 2025 value of USD 3.62 billion with 2031 projections showing USD 5.23 billion, growing at 6.32% CAGR over 2026-2031.

The expansion of nuclear-medicine procedures, regulatory mandates for continuous environmental surveillance, and rapid advancements in semiconductor-based detector performance underpin this trajectory. Heightened security concerns reinforce demand across border control, first-responder, and critical infrastructure segments, while aging reactor fleets drive the need for decommissioning-linked monitoring deployments. The radiation detection, monitoring, and safety market benefits from a dual-use value proposition that aligns civilian healthcare investments with national-security spending, creating a resilient revenue base. North American utilities, European nuclear-phase-out programs, and Asia-Pacific build-outs collectively accelerate replacement cycles for legacy detection platforms. Digital connectivity, predictive analytics, and cloud-native architectures now distinguish premium offerings, supporting aftermarket software revenues and recurring service contracts.

Global Radiation Detection, Monitoring, And Safety Market Trends and Insights

Rising Incidence of Cancer and Chronic Diseases

Cancer prevalence is climbing toward 35 million global cases by 2050, enlarging the addressable base for precision dosimetry systems.Radiotherapy departments now specify sub-millisecond beam-monitoring accuracy, favoring semiconductor detectors that capture high-frequency fluctuations in dose rate. Adaptive treatment planning platforms amplify data-generation volumes, and clinicians increasingly rely on real-time feedback loops to tune fractionated doses. Health systems, therefore, budget for multi-channel dose-verification racks, redundant field calibrators, and cloud-hosted dose-registry software, an ecosystem that broadens the radiation detection, monitoring, and safety market. Vendor strategies focus on modular detector heads and AI-assisted QA dashboards that enhance linear-accelerator uptime.

Expanding Nuclear Medicine and Radiotherapy Procedures

Nuclear medicine examinations grew 12% year-over-year in 2024, propelled by theranostic isotopes such as actinium-225 and lutetium-177.Radiopharmaceutical hubs require air-borne alpha-particle monitors, hot-cell gamma spectrometers, and personal dosimeters that auto-synchronize with facility LIMS databases. Decentralized cyclotron networks, positioned closer to patient populations, multiply procurement nodes for shielding cabinets, de-contamination portals, and leak-testing kits. Standardization under U.S. FDA 21 CFR Part 361 obliges isotope-specific calibration protocols, ensuring recurring outsourcing opportunities for detector-recalibration service providers. These trends elevate ASPs (average selling prices) and extend aftermarket revenue visibility.

Stringent Multi-Jurisdictional Compliance Burden

Detector OEMs must clear FDA 510(k) dossiers, satisfy IEC 60601-2-45 performance metrics, and attain CE marking conformity, each requiring discrete biocompatibility, EMC, and radiation pattern tests. Documentation alone inflates research and development budgets, steering smaller innovators toward licensing deals or niche academic markets. Parallel certification tracks hinder agile firmware updates once fielded devices enter multi-country footprints, slowing feature rollouts. The result is elongated design-win cycles that can exceed four years, diluting NPV on new technology investments and tempering near-term revenue acceleration within the radiation detection, monitoring, and safety market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Real-Time Environmental Monitoring

- Miniaturization and IoT-Enabled Dosimeters

- Shortage of Certified Radiation Safety Officers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Detection and monitoring systems generated 50.74% of 2025 revenue, anchoring procurement budgets for hospitals, utilities, and defense agencies that must continuously validate dose conditions. Within the radiation detection, monitoring, and safety market size, detection platforms are projected to grow alongside predictive analytics modules that recommend proactive maintenance intervals. Safety equipment, encompassing lead-lined apparel, decontamination booths, and automated containment doors, is outpacing historical norms with a 7.55% CAGR, buoyed by harmonized ISO 2919 protective device standards. Integrated offerings that unite real-time g-ray probes with motorized shielding curtains shorten alarm-to-containment times and improve ALARA (as low as reasonably achievable) compliance. Vendors leverage cross-selling synergies: hospitals ordering scintillation probes often append badge-dosimetry subscriptions, while reactor operators bundle perimeter portals with shelter-in-place ventilation systems. Price elasticity remains modest, as regulatory obligations heighten procurement urgency, ensuring premium SKUs maintain a steady pull-through across the radiation detection, monitoring, and safety industry.

The expanded functionality of cloud dashboards, geo-tagged alarm visualization, role-based access, and automated compliance report generation pushes detection gear beyond commodity status. SaaS overlays carry significant gross margin, outstripping hardware rates and encouraging hardware-agnostic ecosystems. Consequently, channel partners favor stocking multi-protocol gateways that integrate NaI(Tl), CZT, and neutron modules under one supervisory HMI. Real-time analytics further reduces false-positive occurrences, trimming costly evacuation incidents. Such value-added solutions reinforce the leadership of detection solutions within the broader radiation detection, monitoring, and safety market.

The Radiation Detection, Monitoring and Safety Market Report is Segmented by Product Type (Detection and Monitoring and Safety), Detector Technology (Gas-Filled, Scintillation, and More), End-User Industry (Medical and Healthcare, Energy and Power, Homeland Security and Defence, Industrial, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 30.05% revenue lead in 2025, reflecting entrenched nuclear-power fleets, extensive homeland-security infrastructures, and early-adopter healthcare systems. U.S. national laboratories are funneling research and development grants into CZT detector miniaturization, while the Canadian NRCan framework is subsidizing environmental-monitoring upgrades at research reactors. Mexico's expanding radiopharmaceutical exports add incremental volume for isotope-production hot-cell monitors. Cross-border standardization under ANSI N42 enhances equipment interoperability, thereby reinforcing economies of scale within the regional radiation detection, monitoring, and safety market.

Asia-Pacific records the fastest trajectory at an 8.05% CAGR, underwritten by China's plan to commission 150 reactors before 2060. The localization mandate embedded in Beijing's Made-in-China 2025 policy promotes joint-venture fabrication plants for CZT wafers, reducing import tariffs and mitigating supply-chain fragility. Japan's post-Fukushima regulatory regime finances perimeter gamma-ray meshes extending 20 km around reactor sites, while India's Department of Atomic Energy funds low-cost survey meters for cancer-therapy wards in tier-two cities. South Korea's expanding 18-MeV cyclotron network further widens the addressable hospital count, reinforcing the Asia-Pacific region's status as the global growth engine for the radiation detection, monitoring, and safety market.

Europe exhibits balanced growth as decommissioning projects in Germany, Belgium, and Spain create specialized demand for alpha-in-air monitors and waste-drum assay systems. France, maintaining a strong nuclear-electricity share, focuses on life-extension upgrades that must meet ASN's stringent seismic-risk criteria. The Euratom treaty standardizes procurement specifications, enabling cross-border volume contracts that leverage multi-year budget cycles. Central and Eastern European nations, modernizing Soviet-era research reactors, seek turnkey detection suites bundled with training services.

The Middle East and Africa, although nascent, are deploying neutron-cargo scanners at strategic ports and commissioning cyclotron-based radiopharmacy labs, foreshadowing medium-term momentum for the radiation detection, monitoring, and safety market in emerging geographies.

- Mirion Technologies Inc.

- Thermo Fisher Scientific Inc.

- Teledyne FLIR LLC

- Fuji Electric Co., Ltd.

- Unfors RaySafe AB

- Arktis Radiation Detectors Ltd.

- Kromek Group plc

- Berthold Technologies GmbH & Co. KG

- Alpha-Spectra, Inc.

- Radiation Detection Company

- Centronic Ltd.

- Burlington Medical LLC

- Amray Group Ltd.

- Atomtex SPE

- Polimaster Ltd.

- Smiths Detection Group Ltd.

- Ludlum Measurements, Inc.

- Hitachi-Aloka Medical, Ltd.

- General Atomics Electronic Systems

- Else Nuclear s.r.l.

- Silena Group s.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of cancer and chronic diseases

- 4.2.2 Expanding nuclear medicine and radiotherapy procedures

- 4.2.3 Regulatory push for real-time environmental monitoring

- 4.2.4 Miniaturisation and IoT-enabled dosimeters

- 4.2.5 UAV-based wide-area radiation mapping

- 4.2.6 De-commissioning of ageing nuclear reactors worldwide

- 4.3 Market Restraints

- 4.3.1 Stringent multi-jurisdictional compliance burden

- 4.3.2 Shortage of certified radiation safety officers

- 4.3.3 High capex for spectroscopic-grade detectors

- 4.3.4 Supply-chain volatility for He-3 and scintillator crystals

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Detection and Monitoring

- 5.1.2 Safety

- 5.2 By Detector Technology

- 5.2.1 Gas-Filled (Geiger-Muller, Proportional, Ion-Chambers)

- 5.2.2 Scintillation (NaI(Tl), CsI, LaBr3, Plastic)

- 5.2.3 Semiconductor (HPGe, CZT, SiPM)

- 5.2.4 Personal Dosimeters (TLD, OSL, Electronic)

- 5.3 By End-user Industry

- 5.3.1 Medical and Healthcare

- 5.3.2 Energy and Power (Nuclear, Conventional)

- 5.3.3 Homeland Security and Defence

- 5.3.4 Industrial (Oil and Gas, Mining, Manufacturing)

- 5.3.5 Research and Academic Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Spain

- 5.4.3.4 Russia

- 5.4.3.5 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Egypt

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global overview, Market overview, Core Segments, Financials, Strategic Info, Market Share, Products and Services, Recent Developments)

- 6.4.1 Mirion Technologies Inc.

- 6.4.2 Thermo Fisher Scientific Inc.

- 6.4.3 Teledyne FLIR LLC

- 6.4.4 Fuji Electric Co., Ltd.

- 6.4.5 Unfors RaySafe AB

- 6.4.6 Arktis Radiation Detectors Ltd.

- 6.4.7 Kromek Group plc

- 6.4.8 Berthold Technologies GmbH & Co. KG

- 6.4.9 Alpha-Spectra, Inc.

- 6.4.10 Radiation Detection Company

- 6.4.11 Centronic Ltd.

- 6.4.12 Burlington Medical LLC

- 6.4.13 Amray Group Ltd.

- 6.4.14 Atomtex SPE

- 6.4.15 Polimaster Ltd.

- 6.4.16 Smiths Detection Group Ltd.

- 6.4.17 Ludlum Measurements, Inc.

- 6.4.18 Hitachi-Aloka Medical, Ltd.

- 6.4.19 General Atomics Electronic Systems

- 6.4.20 Else Nuclear s.r.l.

- 6.4.21 Silena Group s.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment