PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432578

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1432578

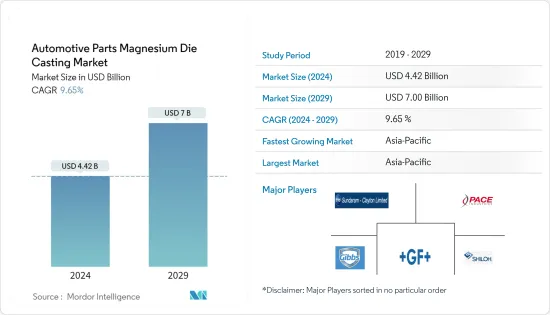

Automotive Parts Magnesium Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Automotive Parts Magnesium Die Casting Market size is estimated at USD 4.42 billion in 2024, and is expected to reach USD 7 billion by 2029, growing at a CAGR of 9.65% during the forecast period (2024-2029).

The COVID-19 pandemic hampered the market in focus for the year 2020, primarily attributed to decline in vehicle sales and production. The global vehicle sale declined by 16% in 2020 as compared to the 2019 vehicle sales. All main vehicle-producing countries had major declines, ranging from 11% to almost 40%. Europe represented an almost 22% share of global production. However, post-pandemic the automotive industry witnessed significant growth for the year 2020. The overall increase in vehicle sales and expected increase in electric vehicle sales is anticipated to primarily drive the market during the forecast period.

Lightweight vehicles are gaining popularity among vehicle manufacturers owing to an enhanced fuel economy of automobiles with adoption of lightweight automotive materials manufacturing crucial parts. Additionally, the light-weighting of vehicles must be done without compromising on safety before quality and performance.

An enactment of stringent emission norms across the globe is liekly to witness significant growth for the market. Rising consumer trend towards light weight vehicle is likely to increase the penetration of light weight parts such as magnesium and carbon fiber reinforced plastic, to manufacture vehicle components, which in turn is anticipated to boost the market.

Major manufacturing industries are investing in research and development activities regarding new magnesium alloys and efficient manufacturing techniques. For instance, the Indian Institute of Technology, Madras, the US Army Research Laboratory, and the University of North Texas developed a new magnesium alloy that can replace aluminum and steel alloys in the automotive industry and increase the fuel efficiency of vehicles.

Growing investment in automation of manufacturing process is likely to witness major growth for the market. High cost of magnessium die casting manufacturing process is liekly to hamper the automotive parts magnesium die casting market.

Automotive Parts Magnesium Die Casting Market Trends

Pressure Die Casting dominating the market

Rise in demand for electric vehicles and a shift in consumer preferences have pushed vehicle manufacturer to replace heavier components with lightweight which are manufactured from alloys like Magnesium.

Major vehicle manufcturer use magnesium alloy for applications like mirror housings, steering columns, driver's airbag casings, seat frames, and dash encasings. Growing trend towards greater battery and fuel efficiency, along with demand for improved performance, has driven an increased interest in high-pressure die cast magnesium alloys. These alloys have an excellent combination of mechanical properties and the highest strength to weight ratio of any structural metal.

In addition, the companies manufacturing EV are also actively procuring pressure diecasting machines and are adopting this technology to make themselves ready for growing consumer demand.

Some of the key players offering automotive pressure die casting components in the region include OEFORM Limited, CNM Tech, Dalian Yaming Automotive Parts Co. Ltd, LC Rapid, and others. While some players focusing on upgrading their portfolio others focus on the manufacturing plants expansion, collaborations, etc. to pitch themselves as top players in the market. For instance,

- In February 2021, Nantong Jiangzhong Photoelectricity Co., Ltd. Installed its Italpresse gauss TF5700 high pressure die casting (HPDC) machine at the company's base in Jiangsu province, China. With its huge 3500 x 3500mm plates, the TF5700's closing force of 5700 tons making it the ideal solution for large part production. Jiangzhong has also purchased a Westomat 3100 from StrikoWestofen to integrate seamlessly with the machine.

Asia-Pacific Projected to Dominate the Market During the Forecast Period

Asia Pacific has major presence of manufacturing industries which is likely to create an opprtunity for automotive parts magnesium die casting market. Rapid expansion of small and medium manufacturing industries across the region is likely to witness major growth for the market. Rise in vehicle production across the region is likely to increase the demand for magnesium die casting parts which in turn is likely to witness major growth for the market.

Rise in demand for electric vehicle across the region owing to an enactment of stringent emission norms is prmpting vehicle manufacturer to integrate lightweight parts in vehicle. China is one of the major producers of die casting parts and accounts for more than 60% of the regional (Asia-Pacific) die casting market share. The metal casting industry in China has more than 26,000 facilities, out of which 8,000 facilities produce non-ferrous castings. The country produces over 49.3 million metric tons of castings. The advanced and efficient automatic die casting machines supported the demand for metal die castings in the country. The Chinese magnesium die casting market experiences high demand from the automotive industry, which is rapidly growing at the international level. This is expected to drive the Chinese market's growth over the forecast period.

The Government of India focus on Make in India, developing the automotive industry, and the stringent emission norms are driving the market for automotive parts magnesium die casting in the country. The castings consumed by the automotive sector accounted for 35% of the country's production. India witnessed a declining trend in passenger vehicle sales, owing to numerous reasons, such as economic slowdown, rise in fuel, and insurance costs. However, despite numerous pressures, such as revised axel norms and NBFC crisis, the overall commercial vehicle sales increased and showcased a robust 27.28% growth.

The latest regulatory framework, the China 6, which was introduced in 2016 and the first stage China 6a came into effect from July 2020 and the second stage is planned for July 2023. The change in the regulatory standards that have been crucial in determining the dynamics of the automotive market in the region. The Ministry of Environmental Protection (MEP), has been maintaining the record of emission performance standard for each new vehicle registered in. This is likely to witness major growth for the automotive part magnesium die casting market across the Asia-Pacific during the forecast period.

Automotive Parts Magnesium Die Casting Industry Overview

The global automotive parts magnesium die casting market isdomnaitng by regional small- and medium-scale players across both developing and developed countries around the world. Major recognized players, such as Georg Fischer Automotive, Ryobi Die Casting, Shiloh Industries, and Pace Industries, accounted for over 30% of the overall global market share.

Growing merger and acquisition between vehicle manufacturer and automotive parts manufacturing companies across the globe is witnessing major growth for the market. Major industries investing on research and development facilities on the light weight parts to enhance vehicle fuel efficiency. For instance,

- In May 2022, GF Casting Solutions, a division of GF, Schaffhausen and the Bocar Group have signed an agreement to offer a specialized range of products and services worldwide. The collabration helped to develop and invest in new technologies and services to support customers in North America, Europe and Asia.

- In January 2022, Koch Enterprises, Inc. has announced the acquisition of Amprod Holdings, LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porters Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Production Process

- 5.1.1 Pressure Die Casting

- 5.1.2 Vacuum Die Casting

- 5.1.3 Gravity Die Casting

- 5.1.4 Squeeze Die Casting

- 5.2 Application

- 5.2.1 Body Parts

- 5.2.2 Engine Parts

- 5.2.3 Transmission Parts

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of the Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Chicago White Metal Casting Inc.

- 6.2.2 Sandhar Group

- 6.2.3 Georg Fischer AG

- 6.2.4 Gibbs Die Casting Group

- 6.2.5 Magic Precision Ltd.

- 6.2.6 Meridian Lightweight Technologies Inc.

- 6.2.7 Morimura Bros Ltd.

- 6.2.8 Tadir-Gan Group (Ortal Ltd)

- 6.2.9 Pace Industries

- 6.2.10 Shiloh Industries Inc.

- 6.2.11 Sundaram-Clayton Ltd.

- 6.2.12 Twin City Die Castings Co.

- 6.2.13 Dynacast (Form Technologies Inc.)

- 6.2.14 Ryobi Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS